Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

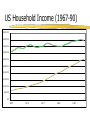

Discounting, Real, Nominal Values H. Scott Matthews 12-706 / 19-702 Admin Issues Pipeline case study writeup - due Monday Format expectations: Framing of problem (see p. 7!), Answer/justify with preliminary calculations Don’t just estimate the answer! Do not need to submit an excel printout, but feel free to paste a table into a document Length: Less than 2 pages. Announcements HW 1 Returned Solutions / “best answers” posted this afternoon Pipeline Case (for next Monday) posted Project Financing Goal - common monetary units Recall - will only be skimming this material in lecture - it is straightforward and mechanical Especially with excel, calculators, etc. Should know theory regardless Should look at problems in Chapter and ensure you can do them all on your own by hand General Terms and Definitions Three methods: PV, FV, NPV Future Value: F = $P (1+i)n P: present value, i:interest rate and n is number of periods (e.g., years) of interest i is discount rate, MARR, opportunity cost, etc. n F P (1i)n F(1 i) Present Value: NPV=NPV(B) - NPV(C) (over time) Assume flows at end of period unless stated Notes on Notation P F (1i)n n F(1 i) P F 1 (1i )n (1 i) n But [(1+i)-n ] is only function of i,n $1, i=5%, n=5, [1/(1.05)5 ]= 0.784 = (P|F,i,n) As shorthand: Future value of Present: (P|F,i,n) So PV of $500, 5%,5 yrs = $500*0.784 = $392 Present value of Future: (F|P,i,n) And similar notations for other types Timing of Future Values Normally assume ‘end of period’ values What is relative difference? Consider comparative case: $1000/yr Benefit for 5 years @ 5% Assume case 1: received beginning Assume case 2: received end Timing of Benefits Draw 2 cash flow diagrams 1000 1000 1000 NPV1 $1000 1000 1.05 1.052 1.053 1.054 NPV1 =1000 + 952 + 907 + 864 + 823 = $4,545 1000 1000 1000 1000 NPV2 1000 1.05 1.052 1.053 1.054 1.055 NPV2 = 952 + 907 + 864 + 823 + 784 = $4,329 NPV1 - NPV2 ~ $216 Note on Notation: use U for Uniform $1000 value (a.k.a. “A” for annual) so (P|U,i,n) = (P|A,i,n) Finding: Relative NPV Analysis If comparing, can just find ‘relative’ NPV compared to a single option E.g. beginning/end timing problem Net difference was $216 Alternatively consider ‘net amounts’ NPV1 =1000 + 952 + 907 + 864 + 823 = $4,545 NPV2 = 952 + 907 + 864 + 823 + 784 = $4,329 ‘Cancel out’ intermediates, just find ends NPV1 is $216 greater than NPV2 Internal Rate of Return Defined as discount rate where NPV=0 Literally, solving for “breakeven” discount rate Graphically it is between 8-9% But we could solve otherwise E.g. $100k 1i $150k 0 $100k 1i (1i)2 $150k (1i) 2 $100k $150k 1i 1+i = 1.5, i=50% $100k $150k 2 10.5 (10.5) Plug back into original equation<=> -66.67+66.67 Decision Making Choose project if discount rate < IRR Reject if discount rate > IRR Only works if unique IRR (which only happens if cash flow changes signs ONCE) Can get quadratic, other NPV eqns Another Analysis Tool Assume 2 projects (power plants) Equal capacities, but different lifetimes 70 years vs. 35 years Capital costs(1) = $100M, Cap(2) = $50M Net Ann. Benefits(1)=$6.5M, NB(2)=$4.2M How to compare? Can we just find NPV of each? Two methods Rolling Over (back to back) Assume after first 35 yrs could rebuild 6.5M 6.5M NPV1 $100M 6.5M ... $25.73M 1.05 1.052 1.0570 4.2 M 4.2M NPV2 $50M 4.2M ... $18.77M 1.05 1.052 1.0535 NPV2R $18.77M 18.77M $22.17M 1.0535 Makes them comparable - Option 1 is best There is another way - consider “annualized” net benefits Note effect of “last 35 yrs” is very small ($3.5 M)! Recall: Annuities Consider the PV (aka P) of getting the same amount ($1) for many years Lottery pays $A / yr for n yrs at i=5% A A A A P 1i (1i) .. 2 (1i)3 (1i)n A A A P * (1 i) A (1i) (1i) .. 2 (1i)n1 ----- Subtract above 2 equations.. ------A P * (1 i) P A (1i) n P * (i) A(1 (1i1 )n ) A(1 (1 i) n ) A(1(1i) n ) (1(1i) n ) P ;P / A i i a.k.a “annuity factor”; usually listed as (P|A,i,n) Equivalent Annual Benefit “Annualizing” cash flows EANB NPV annuity_ factor recall : annuity _ factor Annuity factor (i=5%,n=70) = 19.343 Ann. Factor (i=5%,n=35) = 16.374 $25.73M EANB1 19.343 $1.33M $18.77M EANB2 16.374 $1.15M Of course, still higher for option 1 Note we assumed end of period pays (1(1i) n ) i Annualizing Example You have various options for reducing cost of energy in your house. Upgrade equipment Install local power generation equipment Efficiency / conservation Residential solar panels: Phoenix versus Pittsburgh Phoenix: NPV is -$72,000 Pittsburgh: -$48,000 But these do not mean much. Annuity factor @5%, 20 years (~12.5) EANC = $5800 (PHX), $3800 (PIT) This is a more “useful” metric for decision making because it is easier to compare this project with other yearly costs (e.g. electricity) Benefit-Cost Ratio BCR = NPVB/NPVC Look out - gives odd results. Only very useful if constraints on B, C exist. Example from Boardman 3 projects being considered R, F, W Recreational, forest preserve, wilderness Which should be selected? Alternative R R w/ Road F F w/ Road W W w/ Road Road only Benefits ($) 10 18 13 18 5 4 2 Costs ($) 8 12 10 14 1 5 4 B/C Ratio 1.25 1.5 1.3 1.29 5 0.8 0.5 Net Benefits ($) 2 6 3 4 4 -1 -2 Question 2.4 Base Case Net Benefits ($) Road only Project “R with Road” has highest NB W w / Road W F w / Road F R w / Road R -4 -2 0 2 4 6 8 Beyond Annual Discounting We generally use annual compounding of interest and rates (i.e., i is “5% per year”) i kn Generally, F P(1 ) k Where i is periodic rate, k is frequency of compounding, n is number of years k=1/year, i=annual rate: F=P*(1+i)n For See similar effects for quarterly, monthly Various Results $1000 compounded annually at 8%, FV=$1000*(1+0.08) = $1080 $1000 quarterly at 8%: FV=$1000(1+(0.08/4))4 = $1082.43 $1000 daily at 8%: FV = $1000(1 + (0.08/365))365 = $1083.27 (1 + i/k)kn term is the effective rate, or APR APRs above are 8%, 8.243%, 8.327% What about as k keeps increasing? k -> infinity? Continuous Discounting (Waving big calculus wand) As k->infinity, P*(1 + i/k)kn --> P*ein $1,083.29 continuing our previous example What types of problems might find this equation useful? Where benefits/costs do not accrue just at end/beginning of period IRA example While thinking about careers .. Government allows you to invest $5k per year in a retirement account and deduct from your income tax Investment values will rise past $5k soon Start doing this ASAP after you get a job. See ‘IRA worksheet’ in RealNominal US Household Income (1967-90) $50,000 $45,000 $40,000 $35,000 $30,000 $25,000 $20,000 $15,000 $10,000 $5,000 $0 1967 1972 1977 1982 1987 Real and Nominal Nominal: ‘current’ or historical data Real: ‘constant’ or adjusted data Use inflation deflator or price index for real US Household Income (1967-90) $50,000 $45,000 $40,000 $35,000 $30,000 Nominal $25,000 Real (2005) $20,000 $15,000 $10,000 $5,000 $0 1967 1972 1977 1982 1987 Income in current and 2005 CPI-U-RS adjusted dollars Adjusting to Real Values Price Index (CPI, PPI) - need base year Market baskets of goods, tracks price changes E.g., http://www.minneapolisfed.org/research/data/us/calc/ With ‘Dec 1977=100’ (for income graphs) CPI-U-RS1990=198.0; CPI2005=286.7 So $30,7571990$* (286.7/198.0) = $44,536 These are values graphed 2005$ Price Deflators (GDP Deflator, etc.) Work in similar ways but based on output of economy not prices Other Real and Nominal Values Example: real vs. nominal GDP If GDP is $990B in $2000.. (this is nominal) and GDP is $1,730B in $2001 (also nominal) Then nominal GDP growth = 75% If 2000 2001 GDP equal to $1450B “in $2000”, then that is a real value and real growth = 46% Then we call 2000 a “base year” Use this “GDP deflator” to adjust nominal to real GDP deflator = 100 * Nominal GDP / Real GDP =100*(1730/1450) = 119.3 (changed by 19.3%) Nominal Discount Rates Market interest rates are nominal They ideally reflect inflation to ensure value Buy $100 certificate of deposit (CD) paying 6% after 1 year (get $106 at the end). Thus the bond pays an interest rate of 6%. This is nominal. Whenever people speak of the “interest rate” they're talking about the nominal interest rate, unless they state otherwise. Real Discount Rates Suppose inflation rate is 3% for that year i.e., if we can buy a “basket of goods” today for $100, then we can buy that basket next year and it will cost $103. If buy the $100 CD at 6% nominal interest rate.. Sell it after a year and get $106, buy the basket of goods at thencurrent cost of $103, we will have $3 left over. So after factoring in inflation, our $100 bond will earn us $3 in net income; a real interest rate of 3%. Real / Discount Rates Market interest rates are nominal They reflect inflation to ensure value Real rate r, nominal i, inflation m “Real rates take inflation into account” Simple method: r ~ i-m <-> r+m~i More precise: r (im) 1m Example: If i=10%, m=4% Simple: r=6%, Precise: r=5.77% Discount Rates - Similar For investment problems: If B & C in real dollars, use real disc rate If in nominal dollars, use nominal rate Both methods will give the same answer Unless told otherwise, assume we are using (or are given!) real rates. Garbage Truck Example City: bigger trucks to reduce disposal $$ They cost $500k now Save $100k 1st year, equivalent for 4 yrs Can get $200k for them after 4 yrs MARR 10%, E[inflation] = 4% All these are real values See “RealNominal” spreadsheet Similar Idea : Exchange Rates / PPP Big Mac handout Common Definition of inputs Should be able to compare cost across countries Interesting results? Why? What are limitations? Hyperbolic Discounting