Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Coronary artery disease wikipedia , lookup

Electrocardiography wikipedia , lookup

Heart failure wikipedia , lookup

Quantium Medical Cardiac Output wikipedia , lookup

Myocardial infarction wikipedia , lookup

Antihypertensive drug wikipedia , lookup

Hypertrophic cardiomyopathy wikipedia , lookup

Arrhythmogenic right ventricular dysplasia wikipedia , lookup

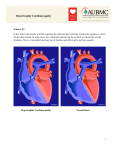

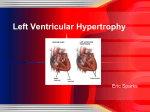

Solutions Medical Underwriting at Work for You LIFE AND DISABILITY INSURANCE Underwriting Applicants with LVH and HOCM What the differences could mean for insurability By Linda Cullings, R.N. Senior Medical Underwriter Michael, 41, an accountant, is applying for term life insurance and disability insurance (DI). He has a history of hypertension, which has been well controlled with medication. At a recent physical, his blood pressure and his cardiovascular exam were normal. Michael’s electrocardiogram (EKG) showed high voltages and deep t-wave inversions in the inferior and lateral leads, suggesting left ventricular hypertrophy (LVH). An echocardiogram was done and showed that the thickness of the intra-ventricular septum was 1.4 centimeters and the posterior wall was 1.2 centimeters. All other echo measurements were normal. A recent stress test demonstrated excellent exercise capacity and was negative for ischemia. Jason, 51, a business owner, is applying for life insurance and DI. Three years ago, he was diagnosed with hypertrophic obstructive cardiomyopathy (HOCM). His most recent echo shows left atrium of 4.1 centimeters, a left ventricular dimension of 4.5 centimeters, intra-ventricular septum thickness of 1.7 centimeters and a posterior wall dimension of 1 centimeter. Jason’s EKG shows deep t-wave inversions. His echocardiograms have been stable for the three years since the HOCM was discovered. Enlarged Left Ventricle Left ventricular hypertrophy and hypertrophic obstructive cardiomyopathy are two cardiac conditions in which the muscular wall of the heart’s left ventricle is enlarged. However, they are not the same. LVH is an adaptive response to high blood pressure and is characterized by symmetrical, or concentric, hypertrophy of the left ventricle. In HOCM there is asymmetrical hypertrophy of the left ventricle in which the septum (the wall separating the left and right ventricles) is enlarged. This hypertrophy may cause an obstruction of blood flow, particularly when the heart is stressed, such as during exercise. HOCM is usually inherited and occurs in the absence of an obvious cause. It may also be called idiopathic hypertrophic sub-aortic stenosis (IHSS) or asymmetrical septal hypertrophy (ASH). An elevated ratio between the thickness of the intraventricular septum and the posterior wall of the heart is considered one of the diagnostic criteria for this type of cardiomyopathy. Continued > If your client has been diagnosed with LVH or HOCM… Here are questions to ask your clients who have been diagnosed with LVH or HOCM: •What did the physicians tell you that you have? When was it diagnosed? •What type of cardiac testing have you had? •Have you ever been hospitalized with problems related to this? If yes, when? •Have you ever been advised to change your activities based on your diagnosis? •What medications are prescribed? For Producer or Broker/Dealer Use Only. Not for Public Distribution. Underwriting Applicants with LVH and HOCM What the differences could mean for insurability Continued > LVH and Hypertension Left ventricular hypertrophy, when caused by hypertension, is a health concern because it indicates that hypertension in the affected individual has started to have important physiological effects. These individuals may also have other manifestations of high blood pressure, such as kidney damage and an elevated risk of stroke and heart attack. If hypertension and LVH are left untreated or are poorly controlled, the heart eventually will no longer be able to pump blood effectively, leading to congestive heart failure. Left ventricular hypertrophy, while a significant health concern, may improve when blood pressure is controlled with medications. Not all people with hypertrophic obstructive cardiomyopathy have symptoms, so they may not realize they have the condition. Some people may exhibit one or more of these symptoms: • Chest pain • Dizziness • Shortness of breath • Hypertension • Fainting during exercise. Unfortunately, for some, the first manifestation of this disease is a fatal arrhythmia. Of those with HOCM, about 1 to 3 percent each year may have a fatal arrhythmia.1 Generally speaking, hypertrophic obstructive cardiomyopathy is a more immediate concern than mild or moderate forms of LVH because it is associated with sudden death. The only effective treatment is surgical reduction of the left ventricular muscle. Life Underwriting Michael would qualify for a standard rating with his left ventricular hypertrophy. Jason would qualify for a moderate substandard rating for his hypertrophic obstructive cardiomyopathy. Disability Underwriting Michael would qualify for DI with 75 percent extra premium and a two- year benefit period limit. Jason would not qualify for disability insurance with hypertrophic obstructive cardiomyopathy. The cases presented here are hypothetical. Specific ratings will vary based on a client’s complete medical history. 1. Maron BJ. Hypertrophic cardiomyopathy: a systematic review. JAMA. Mar 13 2002;287(10):1308-20. Life insurance products are issued by MetLife Investors USA Insurance Company, Irvine, CA 92614, Metropolitan Life Insurance Company, New York, NY 10166, and in New York only by First MetLife Investors Insurance Company, New York, NY 10166. All guarantees are subject to the claims-paying ability and financial strength of the issuing insurance company. Variable products are distributed by MetLife Investors Distribution Company, Irvine, CA 92614. All are MetLife companies. May 2012 Life Insurance Products: • Not A Deposit • Not FDIC-Insured • Not Insured By Any Federal Government Agency • Not Guaranteed By Any Bank Or Credit Union • May Go Down In Value First MetLife Investors Insurance Company Metropolitan Life Insurance Company 200 Park Avenue New York, NY 10166 metlife.com MetLife Investors USA Insurance Company MetLife Investors Distribution Company 5 Park Plaza, Suite 1900 Irvine, CA 92614 BDUW22549 L0412254078[0513] © 2012 METLIFE, INC. PEANUTS © 2012 Peanuts Worldwide For Producer or Broker/Dealer Use Only. Not for Public Distribution.