Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

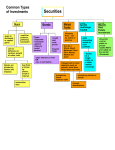

Unit 4 Saving and Investing 1. Compare consumer choices for saving and investing. 2. Explain the relationship be tween saving and investing. 3. Examine reasons for saving and investing, e.g., time value of money. 4. Compare the risk, return, liquidity, manageability, and tax aspects of investment alternatives. 5. Demonstrate how to buy and sell investments. 6. Analyze factors affecting the rate of return on investments (e.g., Rule of 72, simple interest, compound interest). 7. Evaluate sources of investment information. 8. Examine how agencies that regulate financial markets protect investors. 9. Demonstrate how to evaluate advisors’ credentials and how to select professional advisors and their services. Savings Plans • Regular Savings Accounts – often called passbook accounts • Little or no minimum balance • Withdraw money on demand • Called share accounts at credit unions • • • • Very liquid Compounds interest Flexible amounts and withdrawal times FDIC Insured Savings Plans • Money is left on deposit for a stated period of time (term) at a specific rate of return • Maturity Date – the date the money becomes available to you • Three key limitations: • Time specification-Your money is on deposit for 1 month to 5 years • There is a penalty for taking your money before the maturity date • Amount specification-You must deposit a minimum amount • FDIC insured Certificates of Deposit (CD) • Check for the best rate • Consider the economy—if rates are high you may want to buy long-term • Do not “roll-over” at maturity without checking rates • When do you need the money • Consider different CD’s at different rates and maturity dates CD Investment Strategies • • • • Minimum balance required Rates fluctuate monthly as market changes Penalty if you fall below minimum balance Limited amount of checks can be written each month Money Market Accounts • Series EE Savings Bond • Buy at reduced rate, interest rate and time determine maturity date • If cashed after less than 5 years—there is a 3-month penalty of interest • Continues to earn interest for 30 years • Interest is tax-exempt from state and local taxes • Federal taxes are paid when bond is cashed in • If used for higher education, there are no taxes on interest U.S. Savings Bond • Rate of Return – the percentage of increase in the value of your savings • Compounding – interest is earned on both the principal and previously earned interest • Can be compounded every day, month, quarter or year Evaluating Savings Plans • • • • Inflation – compare earning rate with inflation rate Tax Consideration – tax-exempt or tax-deferred savings Liquidity – can I get to my money Restrictions and fees – fees and/or service charges Evaluating Savings Plans Financial institutions must inform you of: • Fees on deposit accounts • Interest rate • Annual percentage yield (APY) – based on stated annual interest rate and the frequency of compounding • Terms and conditions of the savings plan Truth in Savings Investments • Pay YOURSELF FIRST! • EMERGENCY FUND – A savings account that you can access quickly to pay for unexpected expenses or emergencies. • Often thought to be 3 – 8 months of expenditures—very liquid FINANCIAL GOALS Take advantage of 401K or 403B plans employer often matches Elective Savings Programs Special Savings Effort Gifts, inheritances and windfalls FINANCIAL GOALS Investment Growth & Liquidity Time Value of Money – increase in an amount of money due to interest earned over time Rule of 72 – divide the number 72 by your interest rate amount to find out how long it will take to double your investment ◦ Example: Invest $1,000 at 6% =72 / 6 = 12 years to double your amount to $2,000 =72 /12 years = 6, you would need 6% interest to double your investment to $2,000 in 12 years Retained Earnings – profits that a company reinvests, usually for expansion or to conduct research and development. Investment Liquidity – the ability to buy or sell an investment quickly without substantially reducing its value. Investment Growth & Liquidity Safety and risk Safe investment – low return (chance of losing your money is fairly small) Speculative Investment – high risk investment that might earn a large profit in a short time (large return on investment, but you may lose all you invest) ◦ Return on investment will be DIRECTLY related to the risk you take INVESTMENT DECISIONS Inflation Interest Rate Business Failure Financial Market Global Investment 5 COMPONENTS OF RISK • • Varying risk: SAFE: • Government Bonds • Savings Accounts • Certificates of Deposit – – – – • High Risk: – – – – Stocks Corporate bonds Mutual Funds Real Estate Commodities Options Precious Metals and gems Collectibles; coins, stamps, comic books INVESTMENT RISKS A collection of all investments held by an individual ◦ Should be diverse ◦ Diversification-the process of spreading your assets among several different types of investments to reduce risk. Investment Portfolio SAVINGS ACCOUNTS/CDs REAL ESTATE COLLECTIBLES SECURITIES ◦ ◦ ◦ ◦ ◦ BONDS MUTUAL FUNDS OPTIONS COMMODITIES STOCKS Savings & Investing Options Resale for profit Rental Income REAL ESTATE Coins Stamps Beanie Babies Sports cards COLLECTIBLES A bond is lending money to a corporation or government entity for a period of time Corporate Bond – a written pledge to repay a specific amount of money along with interest Government Bond – a written pledge of a government or a municipality such as a city to repay a specific sum of money with interest BONDS A mutual fund is an investment in which investors pool their money to buy stocks, bonds, and other securities selected by professional managers who work for an investment company. MUTUAL FUNDS Contract between a buyer and a seller that gives the buyer the right to buy a particular asset at a later date for an agreed upon price ◦ Example: Buyer agrees on the option to buy 100 shares of stock XYZ for $5 in the future. The stock’s value on that particular date turns out to be $10. If the buyer exercises his right to buy at $5, then his stock value is much greater than what he actually paid for it. OPTIONS Something for which there is a demand but there is no difference in quality, no matter who produces it ◦ Resources such as agricultural products or minerals ◦ Petroleum (gasoline), Paper, Milk, Rice, Gold, Silver ◦ Price based on market as a whole, not on quality of product COMMODITIES Equity capital – money that a business gets from its owners to operate; unit of ownership in a company ◦ Public corporations- sell their stocks openly on the stock market ◦ Private corporations- (closely held) only issue stock to a small group of people STOCKS To gain larger returns than they can get from more conservative investments such as savings accounts or government bonds. WHY BUY STOCK You are not guaranteed what you paid for each share Current value is determined by how much another investor will pay for share – supply and demand A corporation does not have to pay dividends. FACTORS TO CONSIDER WHEN INVESTING IN STOCK A form of Equity – to make money you buy low, sell high – so you make money through appreciation of stock value. The price is how much a buyer is willing to pay. • Common stock – a unit of ownership of a company, it entitles the owner or stockholder to: • • • • • voting privileges growth profits maybe dividends Stock splits Common Stock Dividends – Profit can be paid to shareholders as dividends or be used to “grow” the business May be a specific amount of money or percentage of par value (assigned dollar value printed on the stock certificate that does not change with market price) Stock Splits – divided into twice the number worth half as much ◦ When stock value is higher than “ideal range” ◦ Considered a positive sign to business growth Common Stock (Cont) Shareholder meeting – required to be held one per year Right to vote - one vote for each share they own Preemptive right – current stockholder have first right to buy any new stock a corporation offers Common Stock (Cont) Preferred stock – a type of stock that gives the owner the following advantage: ◦ Cash dividends before common stockholders Attracts more conservative investors Receive dividends first so often purchased if steady income is desired Not considered a good investment for most people Preferred Stock A safe investment that generally attracts conservative investors Strongest and most respected companies ◦ Stable earnings ◦ Consistent dividends Blue-Chip Stocks Pays higher-than-average dividends compared to other stocks ◦ Examples: Dow Chemical Bristol-Myers Squibb Gas and Electric companies Income Stock A corporation whose potential earnings may be higher than the average earnings predicted for industry ◦ Examples in early 2000’s: Home Depot Southwest Airlines Growth Stock Market value tends to reflect the state of the economy ◦ Economy up, market value up ◦ Economy down, market value down Buy on a downturn of the economy to ride as the economy improves Cyclical Stocks A stock that remains stable during declines in the economy ◦ Steady income even when economy declines Defensive Stocks Capitalization- total amount of stocks and bonds issued by a company Large-cap stocks- corporation issued a large number of shares Small-cap stocks- stock issued by a company with less than $500 million capitalization (higher risk) CAP STOCKS Typically sell for less than $1 a share Issued by new companies whose sales are very unsteady Prices go up and down wildly—hard to track Can be risky Penny Stocks NYSE – New York Stock Exchange - The largest stock exchange in the world by dollar value and has 2,764 listed companies. NASDAQ - National Association of Securities Dealers Automated Quotations – the largest electronic screen-based trading market in the United States AMEX - American Stock Exchange – small to mid-sized stocks Stock Exchanges Securities & Exchange Commissionregulatory agency of the stock market and prevents corporate abuses SEC Bull Market –when investors are optimistic about the economy and buy stocks Bear Market – when investors are pessimistic about the economy and sell stocks Market Conditions Newspapers in the financial section ◦ Wall Street Journal The Internet Stock Advisory Services Corporate News Publications ◦ Barron’s ◦ Smart Money Sources for Evaluating Stocks FINANCIAL PLANNER – a specialist who is trained to offer specific financial help and advice ◦ Decision is based on: Income level Willingness to make your own plan PERSONAL INVESTMENT PLAN Fee-only planners – charge an hourly rate or percent of the value of the investments they manage Fee-offset planners – charge an hourly rate but reduce it with commissions they make through your investments FINANCIAL PLANNERS Fee and commission planners – fixed fee for a financial plan and earn commission from products they sell Commission only planners- earn through commissions they make on sales of insurance, mutual funds and other investments FINANCIAL PLANNERS Should provide the following services: ◦ ◦ ◦ ◦ ◦ Assess current financial position Offer written plan with recommendations Discuss plan and answer questions Keep track of your progress Guide you to other financial experts and services as needed FINANCIAL PLANNERS CFP – Certified Financial Planner ChFC – Chartered Financial Consultant Check the credentials before working with a planner Certification of Financial Planners Evaluate investment – research before investing Monitor investment – track the value of the investments Keep accurate records – to notice increase in profits or to reduce losses Managing your Investments Consider tax consequences ◦ Tax-exempt – income not taxed (gov’t bonds) ◦ Tax-deferred – income that is taxed at a later date (IRA’s, 401K’s) ◦ Capital Gain – profit from the sale of an asset; taxed on how long the asset was owned ◦ Capital Loss – sale of an investment for less than its purchase price Managing your Investments • • • • • Internet Newspapers and News Programs Business Publications Government Publications Corporate Reports • Investor Services: • Prospectus – a document that discloses information about a company’s earning, assets and liabilities, its products or services, and its management • Free newsletters mailed to clients • Examples: Moody’s Investment Service or Value Line SOURCES OF INVESTMENT INFORMATION Statistical Averages ◦ Dow Jones Industrial Average- average that consists of 30 of the largest and most widely held public companies ◦ Standard & Poor’s Stock Index -the stocks of 500 corporations, all of which are from the US. SOURCES OF INVESTMENT INFORMATION