Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Capital gains tax in Australia wikipedia , lookup

Environmental, social and corporate governance wikipedia , lookup

Early history of private equity wikipedia , lookup

Private equity in the 2000s wikipedia , lookup

Mark-to-market accounting wikipedia , lookup

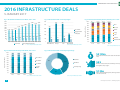

Press Release 5th January 2017 ________________________________________________________________________________________________________ Asian Market Drives Record Investment in Unlisted Infrastructure Assets in 2016 Global infrastructure projects attract an all-time high of $413bn of investment in 2016, propelled by aggregate transaction value of $131bn in Asia Preqin’s end-of-year update on the unlisted infrastructure deal market finds that while the number of financings in 2016 remained consistent with recent years, the aggregate deal value surpassed all previous years. In total, 1,772 deals were completed for infrastructure assets equalling $413bn, although Preqin expects these figures to rise by up to 5% as more information becomes available. This marks an increase of 14% from the $362bn in total deal value seen in 2015, and a sizeable increase from the aggregate deal value of $327bn recorded in 2014. The number of transactions remained similar to the levels seen in 2015 and 2014, which saw 1,743 and 1,787 deals completed respectively, as average asset valuations within the market continue to rise. Asia has seen a significant push for infrastructure investment over the past few years, and saw the highest level of financings of any region in 2016; 552 deals were completed for a record $131bn as fund managers noted the potential for development within the region. Europe is also a prominent market for infrastructure deal activity, and the region saw the highest number of deals (555) for a total of $97bn, while the mature infrastructure market in North America also attracted significant levels of capital ($96bn). Given the demand for infrastructure in less developed countries, it is perhaps unsurprising that the rest of the world saw 237 financings for $89bn, and accounts for five of the top 10 largest deals of 2016. Other Key Infrastructure Deals Facts: Rise of Renewables: As the global push towards alternative energy sources continues, renewable energy has become increasingly prominent; in 2016, renewables accounted for 42% of all deals, up from 39% in 2015 and 37% in 2013. Transport represented 25% of deals in 2016, a decline from 30% in 2015. Deals by Project Stage: Through 2016, greenfield and secondary sites accounted for the highest proportion of infrastructure deals, with 42% and 38% of global financings respectively. However, a fifth of all transactions completed were for assets in the brownfield stage of development. Deals by Value Band: As valuations and the average deal size have risen, large-cap deals have accounted for a higher proportion of the market. Financings larger than $1bn represented 13% of infrastructure deals in 2016, up from 10% the previous year, although assets smaller than $100mn still represented the majority (51%) of transactions in 2016. Largest Deals: Natural resources pipelines account for four of the top 10 largest infrastructure deals in 2016, including the two largest in the UK and Indonesia. Three of the largest 10 financings were for assets in Australia, while two were for refinery plants in Indonesia. To access further information and analysis, please see the factsheet below: Comment: “Infrastructure projects remain central to the development of countries across the world, and as a result the asset class has become home to a diverse range of firms and institutional investors. The constant need for, and evolution of, modern transport systems, alternative power sources and technological structures make the industry an attractive proposition. Moreover, Donald Trump’s infrastructure programme could spur a wave of private investment in the US as participants look to capitalize on the potential for subsidized ownership. However, as demand for infrastructure has increased over the last decade, greater competition for assets – particularly secondary stage assets in developed economies – has pushed valuations upwards. Low interest rates have also contributed to higher pricing demands, as leverage becomes cheaper, which will be a concern for firms. As such, it will be interesting to see if the pace of the market can be sustained moving into 2017 or if managers struggle to deploy their available capital in attractive projects.” Tom Carr – Head of Real Assets Products, Preqin New York London Singapore San Francisco Hong Kong +1 212 350 0100 +44 20 3207 0200 +65 6305 2200 +1 415 316 0580 +852 3958 2819 www.preqin.com / [email protected] Manila ______________________________________________________________________________________________ Note to Editors: Preqin is spelled without the letter ‘U’ after the ‘Q’, the company name being an amalgamation of the former name, Private Equity Intelligence. About Preqin: Preqin is the leading source of information for the alternative assets industry, providing data and analysis via online databases, publications and bespoke data requests. Preqin has built a reputation in the alternative assets industry for providing the most comprehensive and extensive information possible. Leading alternative assets professionals from around the world rely on Preqin’s services daily, and its data and statistics are regularly quoted by the financial press. For more information, please visit: www.preqin.com For more information, please contact: Tom Carr +44 (0)20 3207 0355 or [email protected] For general press enquiries, please contact: William Clarke +44 (0)20 3207 0265 or [email protected] New York London +1 212 350 0100 +44 20 3207 0200 Singapore San Francisco Hong Kong +65 6305 2200 +1 415 316 0580 +852 3958 2819 www.preqin.com / [email protected] Manila DOWNLOAD THE DATA PACK 2016 INFRASTRUCTURE DEALS 5 JANUARY 2017 Fig. 1: Global Annual Infrastructure Deals, 2007 - 2016 Fig. 2: Infrastructure Deals in 2016 by Region 2,000 600 555 1,750 1,787 1,743 1,772 90% 500 1,519 1,550 1,600 400 1,200 1,106 1,099 1,133 1,000 No. of Deals 300 800 Aggregate Deal Value ($bn) 237 600 400 253 307 177 200 196 284 255 362 327 276 413 200 131 97 96 100 70% 60% 50% 1% 1% 16% 16% 1% 1% 10% 11% 12% 8% 8% 11% 1% 1% 13% Other 12% 6% 10% 21% Utilities 30% 23% 25% Energy Social 30% 37% 40% 39% 42% 2008 2009 2010 No. of Deals 2011 2012 2013 2014 2015 2016 0 0% North America Aggregate Deal Value ($bn) Europe Asia Rest of World Source: Preqin Infrastructure Online Fig. 4: Infrastructure Deals by Value Band, 2013 - 2016 2013 9% 10% 10% 9% 10% 9% 80% 30% 27% 25% Total value of infrastructure deals announced in 2016. 8% 28% 50% Greenfield $500-999mn 38% 42% $100-499mn Brownfield 52% 53% 56% 51% Less than $100mn Secondary Stage 555 Number of deals announced in Europe in 2016, the highest of any region. 40% 30% 2016 Source: Preqin Infrastructure Online $413bn 13% 60% 2015 Fig. 5: Infrastructure Deals in 2016 by Project Stage $1bn or More 70% 2014 Source: Preqin Infrastructure Online 100% 90% Transport Renewable Energy 10% 2007 Telecoms 40% 20% 89 0 Proportion of No. of Deals 2% 2% 80% 428 1,325 1,400 100% 552 Proportion of No. of Deals 1,800 Fig. 3: Infrastructure Deals by Primary Industry, 2013 - 2016 20% 10% $13bn 20% Value of Turban Refinery Plant, the largest deal announced in 2016. 0% 2013 2014 2015 2016 Source: Preqin Infrastructure Online 1 Source: Preqin Infrastructure Online © Preqin Ltd. 2017 / www.preqin.com DOWNLOAD THE DATA PACK 2016 INFRASTRUCTURE DEALS 5 JANUARY 2017 Fig. 6: 10 Largest Infrastructure Deals Announced Globally in 2016 Asset Location Primary Industry Investor(s) Deal Size (mn) Stake (%) Deal Date Tuban Refinery Plant Indonesia Natural Resources Refineries PT Pertamina, Rosneft 13,000 USD 100 Apr-16 Ausgrid Australia Power Distribution AustralianSuper, IFM Investors 16,000 AUD 50 Oct-16 ITC Holdings Corp. US Power Distribution Fortis Inc. 11,300 USD 100 Feb-16 India Defence Dassault Systemes, Reliance Infrastructure 7,900 EUR 100 Sep-16 Australia Seaports Future Fund, Global Infrastructure Partners, OMERS, QIC Global Infrastructure 9,700 AUD 100 Sep-16 Mexico Mobile Phone Networks Axtel, CDPQ, CKD-IM, Grupo Multitel, IFC Asset Management Company, International Finance Corporation, Invex, Megacable, Morgan Stanley Infrastructure, Unidentified Investor/s 7,000 USD 100 Nov-16 National Grid's Gas Distribution Networks (UK) UK Natural Resources Pipelines Allianz Capital Partners, Amber Infrastructure Group, China Investment Corporation, Dalmore Capital, Hermes Investment Management, Macquarie Infrastructure and Real Assets (MIRA), Qatar Investment Authority 5,400 GBP 61 Dec-16 Nova Transportadora do Sudeste Gas Pipeline Brazil Natural Resources Pipelines BC Public Service Pension Plan, Brookfield Asset Management, China Investment Corporation, GIC 5,200 USD 90 Sep-16 Cilacap Refinery Plant Indonesia Natural Resources Refineries PT Pertamina, Saudi Aramco 5,000 USD 100 May-16 WestConnex M5 East Tunnel (Stage 2) PPP Australia Transport ACS Group, CIMIC Group, Samsung C&T Corporation 5,000 USD 100 Jun-16 Dassault Reliance Aerospace Port of Melbourne Red Compartida Contract Source: Preqin Infrastructure Online LOOKING FOR MORE DATA AND ANALYSIS? Preqin provides information, data and research on the infrastructure industry across fund performance, fundraising, fund managers, investors, deals, fund terms and more. If you have more detailed requests for private equity data or any questions, please contact us: : +44 (0)20 3207 0265 : www.preqin.com : [email protected] 2 © Preqin Ltd. 2017 / www.preqin.com