Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

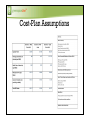

OUTER HEBRIDES ENERGY SUPPLY COMPANY Scoping Study on behalf of COMHAIRLE NAN EILEAN SIAR Dr. Neil Finlayson Donald Macritchie GreenspaceLive Ltd Nigel Walker William Allan Sweett (UK) Ltd Aims and Objectives of the Scoping Study • to explore the feasibility of an Outer Hebrides Energy Supply Company • • • • development of a business case an effective governance structure a route map for delivery cost benefit analysis of the use of existing grid infrastructure • detailed risk assessment Background • In 2010, the UK Government legislated to allow Local Authorities to generate and retail electricity, and to invest in such schemes. • Substantial opportunity for Comhairle nan Eilean Siar to invest in Hebridean renewable generation scheme • Secure a return for the community, create skilled jobs, drive down energy costs for local customers and address fuel poverty issues • Unique and ambitious UK energy supply project Outer Hebrides Energy Projects I Large-scale Onshore Wind Stornoway Wind Farm • • • • 36 3.6 MW turbines – 130MW could produce 410 GWh of renewable electricity per year community has opportunity to purchase 20% of generation (floating share of generation rather than individual turbines) project will enable the community to invest in Stornoway Wind Farm in return for ownership (by an elected Community Trust) of up to 26 MW (20%) of generation International Power • Beinn Mhor wind farm • installed capacity of up to 140MW • expected be fully operational in 2018 Markets • • • • Hebridean residents and businesses Attractive custom tariffs for local residents • eg explore innovative tariffs based on availability of the resource rather simple time-of-day tariffs – islands heat loss is highest when the wind is strongest • community tariffs UK customers for clean renewable energy ‘anchor customers’ • Comhairle nan Eilean Siar, Arnish, Hebridean Housing Partnership, BiFab, BASF and the NHS • retail chains • large municipal Green Deal projects (eg £100m Birmingham Energy Savers project, low carbon Inverness) • Data centres - can consume up to 100 to 200 times as much electricity as standard offices • Highlands and Islands Enterprise £126.4 million next generation fibre broadband project Energy Demand of the Outer Hebrides • DECC estimate 2008 • estimates energy consumption as 513 GWh Barriers • • • • Competition – • SSE and other members of the ‘big six’ • mid-size renewable energy suppliers/aggregators such as Good Energy, Smartest Energy and Co-operative Energy are busily signing long-term power purchase agreements with local generators Liquidity – • relatively low levels of liquidity in electricity forward trading markets, posing problems for smaller independents • makes it difficult for independent suppliers and generators to buy and sell energy at the volume and in the timescales they need to operate effectively Big-six dominance - vertically-integrated generators have less need to trade and are able to hedge between their supply and generation activities. Grid Connection Case Studies • GOTLAND GEAB • UK Public Sector • • • • • • • 25% owned by Gotland municipality, 75% owned by Vattenfall 150 employees Scale of wind-farms and interconnector similar to Hebrides Gotland at least ten years ahead in windfarm implementation Partnerships, especially with large utilities are critical • • • • • Well regarded UK ESCOs Local Authorities instrumental in their formation Risk partially or entirely transferred to the private sector Wider range of energy activities than currently envisaged for OHESC Historically smaller in scale than is currently envisaged for OHESC Very large projects eg Birmingham Energy Savers expected to emerge with Green Deal legislation Could UK ‘city-ESCOs’ be potential customers/partners for OHESC? Case Studies • Good Energy - Mid-Sized UK Electricity Independent • • • • • • • • • Mid-sized private firm operating across UK In 2011 turnover of £21.6m, an EBITDA of £2.8m and a profit before tax of £1.06m Founded in May 2000 to develop and distribute renewable electricity within the UK Has over 75,000 gas, electric and generation customers in total Knowledgeable on Power Purchase Agreements, FIT, trading and, perhaps crucially, marketing Existing relationships with local Hebridean generators Possible joint venture partner? Group plans to generate around 50 per cent. ‘of its own electrons’ Medium term target of owning and operating 110MW of renewable generation assets and to maintain this percentage as the supply side of the business grows. Electricity Generation and Retail - Business Functions • • • • • • • • • • • • • • • • • Operation and maintenance of generation assets Responsibility for scheduling decisions Responsibility for interactions with the Balancing Market Responsibility for determining hedging policy Responsibility for implementing hedging policy Interaction with wider market participants to buy/sell energy Holding of un-hedged positions (either long or short) Procurement of fuel for generation Procurement of allowances for generation Holding of volume risk on positions sold (either internal or external) Matching of own generation with own supply Forecasting of total demand Forecasting of wholesale price Forecasting of customer demand Determination of retail pricing and marketing strategies Bearing of shape risk after initial hedge until market allows full hedge Bearing of short term risk for variance between demand and forecast Cost-Plan Assumptions Cost-Plan Results • • • • Marginally profitable in worst-case scenario Expenditures need much more detailed analysis ROC model not FitCfD ROC multiplier makes ESCO competitive with UK Central FiT CfD Financing • • • • • • • • Partner Funding self-funded by industry partners often replaced post-construction with commercial debt, resulting in a lower cost of capital Commercial Debt Provided by banks on normal commercial terms. Project Finance separate company is established ring-fences the cash flows of the project, against which project finance is secured common model for PPP contract periods often in excess of 15 years. EIB Lending EIB lending for renewable energy reached EUR 6.2bn in 2010 EIB has other financing means, such as equity and carbon funds. The Bank also provides technical assistance to develop projects. European Energy Efficiency Fund Green Investment Bank availability of £18bn of capital to fund renewable projects for purposes of (a) risk mitigation (b) refinancing commitments guaranteeing other funders an exit strategy; and (c) capital provision. Low Carbon Networks (LCN) Fund established by Ofgem Local Authority Prudential Borrowing Risks • weather risk • forward trading risk • many other risks • hedging is critical • eg between generation and supply • or renewable-fossil fuel Company Structure - Options • High risk/reward Owner Operator • Medium risk/reward Joint Venture • Low risk/reward Arm’s Length Possible Joint Venture Partners Route Map Conclusions A substantial new company from the Outer Hebrides could enter the UK electricity market in 2016-2017 retailing clean, green Hebridean electricity to local and export markets. Innovative and attractively priced tariffs could be offered to the local community and companies investing in the community. Substantial numbers of skilled staff could be employed in the Hebrides focused on renewable electricity generation, retailing and marketing, customer support, billing, market trading and engineering. This study indicates that OHESC appears to be a viable proposition and presents a route map to enable the company to be formed.