Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

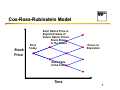

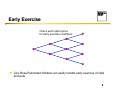

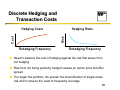

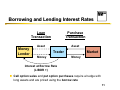

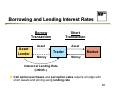

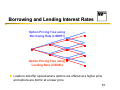

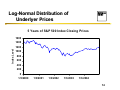

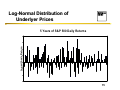

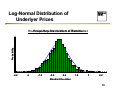

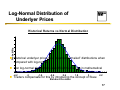

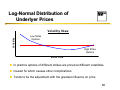

Option Pricing Beyond Black-Scholes Dan O’Rourke January 2005 Black-Scholes Formula (Historical Context) Produced a usable model where all inputs were easily observed Coincided with the introduction of exchange traded options Provided a methodology to create options 1 Black-Scholes Formula (Present) Standard by which all models are compared Market Convention Closed-Form Solution – Computationally fast – “Clean” Derivatives Traders prefer a simple model with a few approximated parameters to an exact model with many precise parameters that are difficult to calculate 2 Black-Scholes Pricing Assumptions Constant Interest Rates Exercise Only at Maturity No Dividends Continuous Hedging No Transaction Costs Equal Borrowing & Lending Interest Rates Constant Volatility Log-Normal Distribution of Underlyer Prices 3 Scope of Discussion Plain-Vanilla Options vs. Exotic Options Underlying Assets – Equities (Stocks, Stock Indexes, Funds) – Debt Instruments (Bonds, Rates, Swaps) – Commodities (Metals, Energy, Agriculture) – Currencies – Others (Real Estate, Inflation, Weather) Arbitrage Pricing vs. Relative Value 4 Two General Methods for Relaxing the Assumptions Numerical Approximation Models – Cox-Ross-Rubinstein/Binomial Models – Monte-Carlo Based Models Adjustments to the Black-Scholes Inputs – Although not theoretically correct, inputs can be adjusted to approximate reality creating a practical model 5 Cox-Ross-Rubinstein Model Flexible Intuitive Approximations yield results comparable to Black-Scholes formula Simple framework provides solutions for many exotic options Relatively computationally efficient 6 Cox-Ross-Rubinstein Model Stock Price Price Today Each Option Price is Expected Value of Future Option Prices Stock Rises In the Future Prices at Expiration Stock Falls In the Future Time 7 Early Exercise Check each option price for early exercise conditions Cox-Ross-Rubinstein Models can easily handle early exercise of calls and puts 8 Dividends Tree “breaks” and drops by dividend amount Discrete future dividends are difficult to model Hard to predict across the distribution of prices Difficulty in placing dividends on a tree 9 Discrete Hedging and Transaction Costs Hedging Risks R isk C o st Hedging Costs Rehedging Frequency Rehedging Frequency Need to balance the cost of hedging against the risk that arises from not hedging Risk from not being perfectly hedged creates an option price bid-offer spread The larger the portfolio, the greater the diversification of single-name risk which reduces the need to frequently re-hedge 10 Borrowing and Lending Interest Rates Money Lender Loan Transaction Purchase Transaction Asset Asset Trader Money Market Money Interest at Borrow Rate (LIBOR +) Call option sales and put option purchases require a hedge with long assets and are priced using the borrow rate 11 Borrowing and Lending Interest Rates Asset Lender Borrow Transaction Short Transaction Asset Asset Trader Money Market Money Interest at Lending Rate (LIBOR -) Call option purchases and put option sales require a hedge with short assets and pricing using lending rate 12 Borrowing and Lending Interest Rates Option Pricing Tree using Borrowing Rate (LIBOR+) Option Pricing Tree using Lending Rate (LIBOR-) Leads to bid-offer spread where options are offered at a higher price and options are bid for at a lower price 13 Log-Normal Distribution of Underlyer Prices 5 Years of S&P 500 Index Closing Prices 1600 1400 Index Level 1200 1000 800 600 400 200 0 1/3/2000 1/3/2001 1/3/2002 1/3/2003 1/3/2004 14 Log-Normal Distribution of Underlyer Prices Logarithm ic Return 5 Years of S&P 500 Daily Returns 15 Log-Normal Distribution of Underlyer Prices Probability Frequency Distribution of Distribution Returns Historical Returns vs Norm al -4.2 -3 -1.8 -0.6 0.6 1.8 3 4.2 Standard Deviation 16 Log-Normal Distribution of Underlyer Prices Probability Historical Returns vs Norm al Distribution Historical underlyer prices tend to exhibit “fat tailed” distributions when compared with log-normal Non log-normal distributions are difficult to describe in mathematical terms -4.2 -3 -1.8 -0.6 0.6 1.8 3 Traders compensate for this by introducing the concept of Skew 4.2 Standard Deviation 17 Log-Normal Distribution of Underlyer Prices Vollatility Volatility Skew Low Strike Options High Strike Options Strike Price In practice options of different strikes are priced at different volatilities Inexact fix which causes other complications Tends to be the adjustment with the greatest influence on price 18 Final Comments Models are only approximations of market behavior and all have restrictive assumptions As long as there is uncertainty in inputs, there will be uncertainty in outputs Markets in many ways are irrational, it may not be possible to create a rational pricing model Traders make money by both buying and selling, knowing the exact value is not a necessity 19