Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

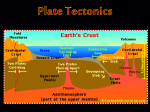

REGULATION OF CATASTROPHIC INSURANCE: MEXICO INSURANCE SUPERVISION IN AMERICA PANEL: NATURAL DISASTERS AND CLIMATIC CHANGE NORMA ALICIA ROSAS RODRÍGUEZ PRESIDENT, INSURANCE AND SURETY NATIONAL COMMISSION (CNSF-MÉXICO) SEPTEMBER 9th, 2016 INSURANCE FOR CATASTROPHIC RISKS • Seismic activity in Mexico is one of the most relevant around the world. Therefore in 1999 the CNSF established a regulation for earthquake insurance in order to estimate the risk premium and the probable maximum losses (PML) linked to the portfolio of each insurance company. This regulation has been updated throughout the last years. • Furthermore, due to a rise in the frequency of hydro-meteorological events, as well as in the level of assurance in high-risk areas, the CNSF started in 2004 a project to establish a regulation on insurance for hurricane and other hydro-meteorological risks, which was implemented in 2007. TECTONIC PLATES OF THE AMERICAN CONTINENT 1. North American Plate 1 2. Cocos Plate 2 3. Pacific Plate 6 4. Nazca Plate 3 5 4 5. South American Plate 6. Caribbean Plate TECTONIC PLATES OF THE AMERICAN CONTINENT 1. Placa NorthNorteamericana American Plate 2. Placa Cocosde PLate Cocos 3. Placa Pacificdel Plate Pacífico Subduction Zone in Mexico SUBDUCTION ZONE IN MEXICO Pacific Plate North American Plate Cocos Plate SUBDUCTION ZONE OF MEXICO Pacific Plate North American Plate Mexico City Area Cocos Plate North American Plate Cocos Plate INSURANCE FOR CATASTROPHIC RISKS Mexico is located in an area with a high incidence of hurricanes. Hurricane Odile, 2014 Hurricane Wilma, 2005 REGULATORY FRAMEWORK The regulatory framework establishes the following: Additional Profits Limit: 90% of PML Rate Uses of the reserve: Operational cost, acquisition, profit and XL coverage. Ceded claims in case of insolvency of reinsurers Coverage purchase in case of hardening of reinsurance Risk premium On going Risk Reserve Reinstallation cost coverage Held claims Catastrophic Reserve [Long term] RESEARCH • Experts from the Engineering Institute of the Autonomous National University of Mexico (UNAM) conducted extensive research for modeling the regulatory framework for earthquake, hurricane and other hydrometeorological insurance. The purpose of this research was to obtain models to estimate: o Risk Premium, and o Probable Maximum Losses (PML) for the insurance policy portfolio. • The research focused on mathematical models and statistical information both of Earthquake and of Hurricanes and other Hydro-meteorological Risks (hurricane, storm, overflow of rivers and lakes, underwater earthquake). CALCULATION OF EARTHQUAKE PML REGULATION PARAMETERS IN MEXICO (1/3) • The RS-CNSF model applied for the earthquake regulation in Mexico calculates the Probable Maximum Losses (PML) using the following parameters: a) A return period of the event of 150 years. b) The maximum value of damage that it would exceed, with a 10%of probability, taking into account all the earthquakes that have the return period of the given event (150 years), involving a percentile of 90% over the vulnerability curve. CALCULATION OF EARTHQUAKE PML REGULATION PARAMETERS IN MEXICO (2/3) • This means that: a) for an event with a return period of 150 years (with possibility to occur of 1 in 150), and b) with a probability of 10% (1/10) to exceed certain level of damage, when that event occurs, there is a posibility of 1 in 1500 that the estimated damage exceeds the vulnerability curve in 90%. • This estimation corresponds to the «return period of bankruptcy» or «possibility of ruin». HURRICANE SIMULATION REGULATION PARAMETERS IN MEXICO (3/3) • Among the most significant elements of the conducted research is the simulation of hurricanes (path and strength), which was made taking into account the historical record of the original path of hurricanes that have affected the country. • Hurricane simulation was performed by a disturbance of the original paths, in order to use the value of the losses caused by wind, flood and tide, and thus modeling the loss functions. • In addition, the vulnerability functions were built to estimate the simulated losses and, under this context, to model the loss functions by wind, storm, tide, flood, hail and tsunami. From these functions it is possible to estimate the Probable Maximum Losses and the Risk Premium associated with the portfolio of insurance policies of an institution. EARTHQUAKE SYSTEM AND HURRICANE AND OTHER HYDRO-METEOROLOGICAL RISKS SYSTEM • Based on the reseach conducted by the Engineering Institute of the Autonomous National University of Mexico (UNAM), two separate systems were developed, namely two software packages that allow to perform the estimation of risk premiums (which are the basis of the Ongoing risk reserve estimation) and the PML (which is the basis for solvency requirements for these type of risks). CONCLUSIONS • The stability and integrity of the insurance markets exposed to catastrophic risks largely depends on having technical elements to properly assess the insurance institutions’ solvency. o Technical risk assessment instruments for the measurement of technical reserves and solvency. • o For risks of low frequency and high severity. Supervision implications for catastrophic risks in the case of composite undertakings. • The creation of catastrophic risk reserves is established according to geographical features and natural risks to which Mexico is exposed. • The Solvency Capital Requirement considers in its calculation risks of catastrophic nature. REGULATION OF CATASTROPHIC INSURANCE: MEXICO NORMA ALICIA ROSAS RODRÍGUEZ PRESIDENT, INSURANCE AND SURETY NATIONAL COMMISSION (CNSF-MÉXICO) www.gob.mx/cnsf [email protected] SEPTEMBER 9th, 2016