Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

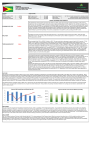

Guyana Prepared by: Rajesh Ramroop [email protected] Last updated: October 2014 COUNTRY Guyana Real GDP growth (%) 2014 Next General Election Exchange Rate (GYD/USD) CREDIT RATING 5.60% Jul‐05 200 S&P Foreign Currency S&P Local Currency Moody's Foreign Curre Not rated Not rated Not rated Major Trade Partners Major Exports GDP Composition US; T&T; EU; Canada; Venezuela; China; Suriname; Jamaica Agricultural products; Fuels and Mining products Services (64%); Agri (22%); Mining (10%); Manu (7%) RECENT ECONOMIC DEVELOPMENTS ECONOMIC OUTLOOK Real GDP expanded by 5.2% in 2013 following growth of 4.8% one year earlier. For 1Q14 sugar output (17.2%) and rice (+9.6%) increased due to favorable weather conditions and increased yields respectively. The manufacturing sector showed decreases in alcoholic (-5.8%) and non-alcoholic (-18.5%) beverages due to a decline in outdoor social events. In the mining sector bauxite production increased (+0.8%) while gold declined (-12.2%) due to increased volatility in world market gold prices and diamond production (-30.3%) due to lower investments. In the quarrying sector there were increases in stone production (+21.7%) due to increased demand in the construction sector while sand production declined (-43.0%). The economy is projected to grow by 5.6% in 2014. Positive INFLATION Stable TRADE BALANCE/ BOP Stable FISCAL ACCOUNTS According to the Urban Consumer Price Index (CPI) there was a 0.4% increase in prices for 1Q14 compared to a 0.57% decline for 1Q13. This was due to moderate increases in food driven by sugar, honey and related products, meat and milk products and increases in fuel and fuel related products prices as well. Inflation is projected at 5.0% for 2014 (4.3% - IMF) due to expected increases in fuel and commodity prices. Export receipts fell by 10.1% in 1Q14 due to a decline of US$28.3 million in export receipts of gold by US$28.3 million and US$7.9 million in rice. Merchandise imports declined by 10.9% to US$401.7 million due to declines in imports of capital goods (-25.7%), intermediate goods (-6.9%) and consumption goods (-4.3%). Remittances declined by 5.1% (US$4.4 million) to US$81.0 million compared to 1Q13. The overall balance of payments recorded a larger deficit of US$70.3 million for 1Q14 from a deficit of US$52.8million for 1Q13. This downturn was primarily due to a lower capital account surplus along with lower unrequited transfers. The capital account registered a lower surplus of US$66.1 million due to lower portfolio investment which decreased by 43% to US$5.0 million and lower foreign direct investment which fell by 60% to US$53.4 million in March 2013. Inflows from bilateral and multilateral agencies declined by 10.6% to US$36.1 million as a result of disbursements from PetroCaribe. The current account deficit narrowed by 35.6 % (US$66.2 million) to US$119.6 million due to a lower merchandise trade and services account deficit. The overall deficit on the balance of payments was financed mainly by a drawdown of gross international reserves which were equivalent to 4.3 months of imports at the end of the quarter. The external current account balance is forecasted at -14.6% of GDP for 2014 (-15.9% of GDP - 2013) by the IMF. The Central Government’s overall surplus decreased due to a reduction in current revenue and higher current and capital expenditure for the period. Current revenue declined due to lower excise taxes and dividends, current expenditure expanded on account of higher employment cost and materials and supplies and capital expenditure increased due to the continuation of infrastructural projects. Capital revenue was lower due to a reduction in project grants. External debt (-4.6%) declined due to lower disbursements of US$5.1 million by the Inter-American Development Bank for project financing, delivery of US$30.9 million credit under the Venezuelan PetroCaribe Agreement and the debt write off of US$35.9 million under the CARICOM Multilateral Clearing Facility. Domestic debt (-3.9%) decreased as a result of lower issuance of 364-day treasury bills while the stock of debentures remained constant at G$3,898 million. External debt service increased 8.0% to US$16.6 million, due to the repayment of principal and interest payments to multilateral Institutions and the continuation of both principal and interest payments to India and China while domestic debt service payments decreased by 78.0% to G$339 million mainly due to a 38.9% decline in interest payments on treasury bills. Public sector primary expenditure is forecasted at 30.8% of GDP (29.9% of GDP -2013)with the public sector primary balance forecasted at -3.1% of GDP (-2.8% of GDP -2013). Public sector gross debt is forecasted at 57.8% of GDP for 2014. Stable OUTLOOK Guyana is forecasted to expand at a rate of 5.6% in 2014. Both the IMF and BMI are more conservative and have estimated growth rates of 3.3% and 4.0% respectively mainly due to expected downward pressures on the price of gold. The country remains susceptible to the volatility of global commodity prices but this volatility is expected to be tempered by the improved performance in the Advanced Countries. On the fiscal accounts there are concerns over debt sustainability but the government has been implementing measures to address it. On May 29th the Caribbean Financial Action Task Force (CFATF) citing the inability of Guyana’s government to pass its Anti-Money Laundering and Countering the Financing of Terrorism Act, blacklisted the country and referred them to the Financial Action Task Force (FATF). The immediate effect is that Caribbean banks will now have to increase the level of scrutinization of financial transactions associated with the country. Global blacklisting by the FATF will entail that correspondent international banks perform the same level of monitoring which is an expensive process and may result in closed relations with Guyana’s bank, negatively affecting areas such as financial transactions and remittances. First Citizens Research & Analytics holds a stable view on Guyana from a fundamental point of view, but acknowledges the country's poor infrastructure and need for diversification to non-commodity sectors as well as political instability due to tensions between the country’s government and opposition. 25 6 15 10 5.4 4.4 4.8 5.3 proj 5.8 proj 4 5 2 0 -5 GUYANA GDP % 8 20 2009 2010 2011 2012 H1 2013 -10 GDP Agriculture Mining and Quarrying Manufacturing Services 0 2010 2011 2012 2013 2014 DISCLAIMER This report has been prepared by First Citizens Investment Services Limited, a subsidiary of First Citizens Bank Limited. It is provided for informational purposes only and without any obligation, whether contractual or otherwise. All information contained herein has been obtained from sources that First Citizens Investment Services believes to be accurate and reliable. All opinions and estimates constitute the author’s judgment as at the date of the report. First Citizens Investment Services does not warrant the accuracy, timeliness, completeness of the information given or the assessments made. Opinions expressed may change without notice. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein. The securities discussed in this report may not be suitable to all investors, therefore Investors wishing to purchase any of the securities mentioned should consult an investment adviser. DISCLOSURE We, First Citizens Investment Services Limited hereby state that (1) the views expressed in this Research report reflects our personal view about any or all of the subject securities or issuers referred to in this Research report, (2) we are a beneficial owner of securities of the issuer (3) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report (4) we have acted as underwriter in the distribution of securities referred to in this Research report in the three years immediately preceding and (5) we do have a direct or indirect financial or other interest in the subject securities or issuers referred to in this Research report.