Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

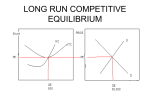

Economics of Strategy Market Structure and Dynamic Competition Defining Markets • “that set of suppliers and demanders whose trading practices establishes the price of a good” – George Stigler and Robert Sherwin Close substitutes • same or similar product performance characteristics • same or similar occasions for use • same geographic market Product performance characteristics • subjective analysis of “similar” products • to reduce subjectivity, list the attributes which you believe are most influential in the consumers purchase decision Occasions for use • Where is the product used? • When is the product used? • How is the product used? Geographic Market • Is the product sold by competitors where customers – are not affected by transportation costs • costs of time for the consumer to travel to an alternative location to purchase • costs of shipping the product to the customers location – are not affected by tax differences – convenience is not a major factor When is the product used? How is the product used? • To listen to music… – – – – – Radio CD Player Tape Player Eight…. No don’t go there Computer Files? Problems • identifying precise product performance characteristics is subjective and imprecise • does not answer “how good a substitute is it?” – Use elasticity to solve this • transportation costs can be influential • convenience can be influential but the price customers are willing to pay for it is subjective Defining the Market • Market definition is the identification of the market(s) in which the firm is a player • Two firms are in the same market if they constrain each other’s ability to raise the price • It is important to define the market if market shares need to be computed (for anti-trust economics or business strategy formulation) Well-Defined Market • If the market is well defined, firms outside the candidate market will not be able to constrain the pricing behavior of those inside • A thought experiment: If all the firms inside the candidate market colluded, can they raise the price by at least 5%? If they can, the market is well defined Coca Cola’s Market • Is Coca Cola’s market, the market for cola drinks or the market for all potable liquids (including tap water)? • In the face of anti-trust concerns, Coke would have preferred the broader definition • Judicial system found the carbonated drinks market to be the relevant one Geographic Competitor Identification • When a firm sells in different geographical areas, it is important to be able identify the competitor in each area • Rather than rely on geographical demarcations, the firm should look at the flow of goods and services across geographic regions Two Step Approach to Identifying Geographic Competitors • First step is to find out where the customers come from (the catchment area) • The second step is to find out where the customers from the catchment area shop • With the technological innovations, some products like books and drugs are sold over the internet bringing in virtual competitors Market Structure • Markets are often described by the degree of concentration • Monopoly is one extreme with the highest concentration - one seller • Perfect competition is the other extreme with innumerable sellers Measuring Market Structure • A common measure of concentration is the N-firm concentration ratio - combined market share of the largest N firms • Herfindahl index is another which measures concentration as the sum of squared market shares • Entropy could be another measure of concentration – How fast do competitors disappear and appear? Hirfindahl Index Structure Perfect Competition Monopolistic Competition Oligopoly Monopoly Herfindahl Index Usually < 0.2 Usually < 0.2 0.2 to 0.6 > 0.6 Intensity of Price Competition Fierce Depends on the degree of product differentiation Depends on inter-firm rivalry Light unless there is threat of entry Market Structures • Chart Market Structure and Dynamic Competitive Forces • A monopoly market may produce the same outcomes as a competitive market (threat of entry) • A market with as few as two firms can lead to fierce competition • Schumpeter’s “gale of creative destruction” Perfect Competition • Many sellers who sell a homogenous product and many well-informed buyers • Consumers can costlessly shop around and sellers can enter and exit costlessly • Each firm faces infinitely elastic demand • PRICE TAKERS Zero Profit Condition • With perfect Competition economic profits are driven to zero • Percentage contribution margin or per unit profits – PCM = (P - MC)/P • where P is price and MC is marginal • When profits are maximized PCM = 1/ where is the elasticity of demand • Since is infinity, PCM = 0 Conditions for Fierce Price Competition • Even if the ideal conditions are not present, price competition can be fierce when two or more of the following conditions are met – – – – – There are many sellers Customers perceive the product to be homogenous There is excess capacity Competitive Contestable Markets exist Many Sellers • With many sellers, cartels and collusive agreements difficult to create/maintain • Cartels fail since some players will be tempted to cheat since small cheaters may go undetected • Even if the industry PCM is high, a low-cost producer may prefer to set a low price Homogenous Products • Make for better substitutes! – Customers are more likely to price shop when the product is perceived to be homogenous and hence sellers are more likely to compete on price • Customers switching from a competitor is likely to be the largest source of revenue gain Excess Capacity • When a firm is operating below full capacity it can price below average cost as price covers the variable cost • If industry has excess capacity, prices fall below average cost and some firms may choose to exit • If exit is not an option (capacity is industry specific) excess capacity and losses can persist Contestable Markets • the viable threat of competition from interloper firms is enough to keep firms acting as if it had actual competitors. • Critical role of entry to dissipate profits • Low barriers to entry required Monopoly • A monopolist faces little or no competition in the product market • Monopolist can act in an unconstrained way in setting prices • A monopolist profit maximizes – equilibrate marginal revenue and marginal costs – price on the demand curve • PRICE SEARCHERS Monopoly and Output • A monopolist perpetually understocks the market and charges too high a price - Adam Smith • Price exceeds the competitive price • Price exceeds the marginal costs of production • Output is below the competitive level Monopoly and Innovation • A monopolist often succeeds in becoming one by either producing more efficiently than others in the industry or meeting the consumers’ needs better than others • Hence, consumers may be net beneficiaries in situations where a firm succeeds in becoming a monopolist Monopoly and Innovation • Monopolists are more likely to be innovative (relative to firms facing perfect competition) because they can capture some of the benefits of successful innovation • Since consumers also benefit from these innovations, they can be hurt in the long run if the monopolist’s profits are restricted Monopolistic Competition • There are many sellers and they believe that their actions will not materially affect their competitors • Each seller sells a differentiated product • Unlike under perfect competition, in monopolistic competition each firm’s demand curve is downward sloping rather than flat • Usually very elastic demand for the firm - many close substitutes Vertical and Horizontal Differentiation • Vertically differentiated products unambiguously differ in quality • Horizontally differentiated products vary in certain product characteristics to appeal to different consumer groups • An important source of horizontal differentiation is geographical location Spatial Differentiation • Video rental outlets (or grocery stores) attract clientele based on their location • Consumers choose the store based on their “transportation costs” • Transportation or transactions costs prevent switching for small differences in price Spatial Differentiation • The idea of spatial location and transportation costs can be generalized for any attribute • Consumer preferences will be analogous to consumers’ physical location and the product characteristic will be analogous to store location Spatial Differentiation • “Transportation costs” will be the the cost of the mismatch between the consumers’ tastes and the product’s attributes • Products are not perfect substitutes for each other • Some products are better substitutes (low “transportation costs”) than others Theory of Monopolistic Competition • An important determinant of a firm’s demand is customer switching • Switching is less likely when – customer preferences are idiosyncratic – customers are not well informed about alternative sources of supply – customers face high transportation costs Theory of Monopolistic Competition Theory of Monopolistic Competition • The demand curve DD is for the case when all sellers change their prices in tandem and customers do not switch between sellers • The demand curve dd is for the case when one seller changes the price in isolation and customers switch sellers • Sellers’ pricing strategy will depend on the slope of dd Theory of Monopolistic Competition • If dd is relatively steep, sellers have no incentive to undercut their competitors since customers cannot be drawn away from them • If dd is relatively flat (stores are close to each other, products are not well differentiated) sellers lower prices to attract customers and end up with low contribution margins Monopolistic Competition and Entry • Since each firm’s demand curve is downward sloping, the price will be set above marginal cost • If price exceeds average cost, the firm will earn short run economic profit • But ease of entry with short run economic profits will attract new entrants until each firm economic profit is zero • Long run economic profit is zero Theory of Monopolistic Competition • Even if entry does not lower prices (highly differentiated products), new entrants will take away market share from the incumbents • The drop in revenue caused by entry will reduce the economic profit • If there is price competition (where products that are not well differentiated) the market mimics pure competition and the erosion of economic profit will be quicker Oligopoly • Market has a small number of sellers • Pricing and output decisions by each firm affects the price and output in the industry • Oligopoly models (Cournot, Bertrand) focus on how firms react to each other’s moves Cournot Duopoly • In the Cournot model each of the two firms pick the quantities Q1 and Q2 to be produced • Each firm takes the other firm’s output as given and chooses the output that maximizes its profits • The price that emerges clears the market (demand = supply) Cournot Reaction Functions Cournot Equilibrium • If the two firms are identical to begin with, their outputs will be equal • Each firm expects its rival to choose the Cournot equilibrium output • If one of the firms is off the equilibrium, both firms will have to adjust their outputs • Equilibrium is the point where adjustments will not be needed Cournot Equilibrium • The output in Cournot equilibrium will be less than the output under perfect competition but greater than under joint profit maximizing collusion • As the number of firms increases, the output will drift towards perfect competition and prices and profits per firm will decline Bertrand Duopoly • In the Bertrand model, each firm selects its price and stands ready to sell whatever quantity is demanded at that price • Each firm takes the price set by its rival as a given and sets its own price to maximize its profits • In equilibrium, each firm correctly predicts its rivals price decision Bertrand Reaction Functions Bertrand Equilibrium • If the two firms are identical to begin with, they will be setting the same price as each other • The price will equal marginal cost (same as perfect competition) since otherwise each firm will have the incentive to undercut the other Cournot and Bertrand Compared • If the firms can adjust the output quickly, Bertrand type competition will ensue • If the output cannot be increased quickly (capacity decision is made ahead of actual production) Cournot competition is the result • In Bertrand competition two firms are sufficient to produce the same outcome as infinite number of firms Bertrand Competition with Differentiation • When the products of the rival firms are differentiated, the demand curves are different for each firm and so are the reaction functions • The equilibrium prices are different for each firm and they exceed the respective marginal costs Bertrand Competition with Differentiation • When products are differentiated, price cutting is not as effective a way to stealing business • At some point (prices still above marginal costs), reduced contribution margin from price cuts will not be offset by increased volume by customers switching Price-Cost Margins and Concentration • Theory would predict that price-cost margins will be higher in industries with greater concentration (fewer sellers) • There could be other reasons for interindustry variation in price-cost margins (regulation, accounting practices, concentration of buyers and so on) Price-Cost Margins and Concentration • It is important to control for these extraneous factors if one need to study the relation between concentration and pricecost margin • Most studies focus on specific industries and compare geographically distinct markets Evidence on Concentration and Price • For several industries, prices are found to be higher in markets with fewer sellers • In markets where the top three gasoline retailers had sixty percent share prices were 5 percent higher compared to markets where the top three had a fifty percent share • For service providers such as doctors and physicians, three sellers were enough to create intense price competition Economies of Scale and Concentration • Industries with large minimum efficient scales compared to the size of the market tend to have high concentration • The inter-industry pattern of concentration is replicated across countries • When production/marketing enjoys economies of scale, entry is difficult and hence profits are high Concentration and Profitability • The concentration and profitability have not been shown to have a strong relationship • Possible explanations: – Differences in accounting practices may hide the differences in profitability – When the number of sellers is small it may be due to inherently unprofitable nature of the business