Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Zero-configuration networking wikipedia , lookup

Passive optical network wikipedia , lookup

Net neutrality wikipedia , lookup

Airborne Networking wikipedia , lookup

Policies promoting wireless broadband in the United States wikipedia , lookup

TV Everywhere wikipedia , lookup

Net neutrality law wikipedia , lookup

List of wireless community networks by region wikipedia , lookup

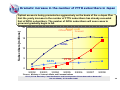

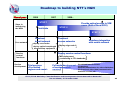

International Telecommunication Union An ’s NGN NGN Anintroduction introduction to to NTT NTT’s and in Japan Japan and new new services services in Naotaka MORITA Vice Chairman of SG13, ITU-T Senior Research Engineer, Supervisor NTT Service Integration Labs. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 Outline 1. The current status and future direction of Japan’s telecommunications market 2. The worldwide telecommunications market and standardization activities 3. NTT’s plans for the deployment of its NGN 4. Future visions for the NGN ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 2 Japan today in 2005 (as of September 2005) ITEMS NUMBER NOTE Population 127.8 M 11/2005, 20% is older than 64. Householders 50.4 M 03/2005 Fixed lines 59.6 M 03/2005 ISDN 8.0 M 10 M at peak in 2001 Mobile 91.8 M 03/2006, 79.8 M have internet access, 70% of total population 3G PHS W-CDMA 26.5 M DoCoMo & Vodafone cdma2000 21.8 M au 4.7 M 03/2006, 6.7 M at peak in 1997 Broadband DSL Optical VoIP 48.3 M 70% growth last year 24.2 M 06/2006, 40% of householders 14.5 M 06/2006, Saturated !! 6.3 M 06/2006, 0.85 M increase in Q2 of 2006, 84% coverage in 2004 8.3 M 0AB type has started. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 3 Measures taken to prolong the lifetime of NTT’s PSTN facilities ••NTT’s NTT’sPSTN PSTNconsists consistsof ofseveral severalthousand thousandswitches. switches. ••Although Althoughaathen-state-of-art then-state-of-artswitching switchingsystem system(NS8000) (NS8000)was wasdeveloped developedaround around10 10years yearsago, ago, the rapid progress in technology since then has resulted in the discontinuation of production the rapid progress in technology since then has resulted in the discontinuation of production of ofsome somecomponents componentsused usedin inthe thesystem. system.Currently, Currently,we weare aretrying tryingto toprolong prolongthe thelifetime lifetimeof ofthe the switches by re-establishing sources for such components. switches by re-establishing sources for such components. POI Transit switch Transit switch Other carriers POI NW between prefectures Several hundreds Transit switch NTT West NW inside a prefecture Several thousands Local switch Local switch NTT East Transit switch 0.35µm 0.5µm 3.3V PS 5V PS 0.6µm 0.8µm 1.0µm 1.2µm 90 nt in ue d Several tens Other carriers Di sc o NTT Communications Integration degree Migration to more highly integrated LSI that operates with lower voltage power supply 1.8, 2.5V PS 0.25µm 95 00 Year 05 NW inside a prefecture Local switch Local switch NS8000 (developed around 10 years ago) ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 4 Maturing of IP telephony technology in Japan yIP yIPtelephony telephonyis isspreading spreadingfrom frombusiness businessusers users(IP-PBX). (IP-PBX).Low Lowrates rates(or (orfree free between betweenspecific specificpoints) points) offered offeredby byISPs ISPshave haveincreased increasedthe thenumber numberof ofIP IPphone phone users usersin inJapan Japanto tomore morethan than10 10million. million. yNTT yNTTalready alreadyprovides providesan anIP IPphone phoneservice service“Hikari “HikariPhone” Phone”using usingthe theordinary ordinary telephone telephonenumbering numberingplan. plan. OCN.Phone OCN 2 Free Affiliated ISP’s IP network Free 8.4 yen/3 min *1 4 Non-affiliated ISP’s IP phone (13ISPs) PSTN phone 8.4 yen/3 min *1 5 6 Million 14 (178ISPs) *1 3 Increase of subscribers to IP phone service Affiliated ISP’s IP phone 11.3yen/3 min Mobile phone network PSTN phone Mobile phone Number of subscribers 1 12 11.46 10 8 8.305 6 4 5.276 2 0 March 2004 March 2005 March 2006 Int’l phone network 7 Discount rate Int’l phone *1: not changed by distance *Source: NTT Communications, Inc.: http://www.ocn.ne.jp/english/personal/option/voip/ ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 5 PSTN • Time is ripe for an IP network to replace PSTN. • Migration to the IP network will reduce both capital and operational expenditure. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 6 Paradigm shift of Japan’s telecommunications market •The •Thenumber numberof of mobile mobilephone phonesubscribers subscribershas hasfar far exceeded exceededthe thenumber numberof of subscribers subscribersto tofixed-line fixed-linetelephony. telephony. •The •Thenumber numberof of Internet Internet users userscontinues continuesto to increase. increase. Internet (Fixed line + mobile phone) Subscribers [million] 120 ● Internet users: 106.24 million 100 ● Mobile phone Mobile phone users: 91.48 million 80 ● 60 40 POTS + ISDN Fixed-line-phone users: 58.79 million Broadband (Optical, ADSL, etc.) ● 20 ● 3/94 3/95 3/96 3/97 3/98 3/99 3/00 3/01 3/02 3/03 3/04 3/05 Broadband users: 19.49 million IP phone users: 8.3 million Sources: Ministry of Internal Affairs and Communications, Consortium for Promotion of Mobile Computing, InfoCom Research Inc., and others. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 7 Shift of NTT Group’s main revenue source to broadband services •The •Therevenue revenuefrom frombroadband broadbandbusiness businesshas hasbeen beenpicking pickingup. up. •It •It is isnecessary necessaryto togrow growbroadband broadbandbusiness businessinto intocarriers’ carriers’ main mainrevenue revenuesource. source. Japan’s broadband market Billion US$ 40 40 Consolidated revenue of NTT Group (Billion US$) 70 30 9 7 34 34 32 32 33 12 12 13 16 18 20 40 40 41 38 36 10 0 :Consumer :Business 15 19 2005 2006 2007 Year (Source: EC Research Corp.) 11 8 8 40 49 21 16 12 12 80 30 24 10 90 50 30 20 100 60 31 46 45 Revenue from broadband market Mobile Internet and data communication Fixed-line analog telephone (POTS) 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 8 Increase in ARPU of broadband services •There •Thereis isaashift shiftfrom fromlow-price low-priceIP IPtelephony, telephony,exploiting exploitingIP IPtechnology, technology,to tothe the provision provisionof ofvalue-added value-addedservices, services,such suchas asvideo videodelivery deliveryand andvideophone, videophone, exploiting the availability of broadband access. exploiting the availability of broadband access. •The •Theprovision provisionof of value-added value-added services services is is increasing increasingARPU. ARPU. Normalized ARPU 4 3 Added ARPU 2 Basic ARPU 1 0 Fixed line telephone service IP phone *1 IP phone + supplementary services IP phone + supplementary services (future) *1: Broadband access charge (including ISP charge) ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 9 Revenue source of telecom carriers Carriers need to shift their main revenue source from the telephony service to broadband services. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 10 Promotion of optical access by u-Japan Strategy The TheJapanese Japanesegovernment’s government’s “u-Japan” “u-Japan” Plan Plan proposes proposes the the full full development development of of broadband broadbandinfrastructure infrastructureby byinstalling installingoptical opticalfiber fibernetworks networksnationwide. nationwide. 1. 100% broadband network The projected status of a 100% broadband network, through which broadband services are made available to all communities, is as follows: (1) Overall, a variety of wireline and wireless technologies will be seamlessly linked. (2) In areas where cost-effective investment is difficult, broadband infrastructure will be built taking both investment efficiency and the needs of communities into account. (3) Of these varieties of broadband service, super-high-speed broadband access, mostly based on FTTH, will cover 90% of households nationwide. Source: Proposed status of broadband networks in 2010 Proposed on Aug. 11, 2006 ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 11 Dramatic increase in the number of FTTH subscribers in Japan Subscribers [millions] Optical Opticalaccess accessis isbeing beingpromoted promotedso soaggressively aggressivelyon onthe thebasis basisof of the theu-Japan u-JapanPlan Plan that the yearly increase in the number of FTTH subscribers has already exceeded that the yearly increase in the number of FTTH subscribers has already exceeded that thatof ofADSL ADSLsubscribers. subscribers.The Thenumber numberof ofADSL ADSLsubscribers subscriberswill willsoon sooncease ceaseto to grow growand andgradually graduallybegin beginto tofall. fall. 20 Official data* forecast 15 ADSL 10 5 CATV FTTH 0 3/2002 3/2003 3/2004 3/2005 3/2006 3/2007 3/2008 *Source: Ministry of Internal Affairs and Communications ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 12 National policy of Japan The spreading of optical access is a national policy. There are positive signs that optical access will indeed become widespread. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 13 Rapid reduction in the charge for broadband access in Japan •Competition •Competitionhas hasintensified intensified into intoaaprice pricewar, war,bringing bringingdown downthe thecharges chargesfor forADSL ADSL and andeven evenFTTH FTTHdramatically. dramatically. •This has resulted •This has resultedin in aasignificant significantreduction reductionin intelecom telecomtraffic trafficrevenue. revenue. Change in monthly charge for broadband access (examples) Yen USD 13000 □ Basic type □ 9000 B-flet’s 90 70 7000 □ New Family Type 5000 △ □ 1.5M △ 3000 □ △ Condo Type 2002 2003 50 30 □ △ 1.5M Type Flet’s-ADSL 2001 Hyper Family Type □ 4100 yen □ 2500 yen 2004 2005 ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 14 Creation of new business •NTT •NTTwill willnot notonly onlyincrease increasetraffic trafficrevenue revenuebut butalso alsoseek seekto togenerate generatenon-traffic non-traffic revenue. revenue. •NTT •NTTalready alreadyattempts attemptsto tocreate createnew new businesses businessesin incollaboration collaborationwith withaavariety varietyof of players outside the telecom industry. players outside the telecom industry. Examples of FMC in service “OCN .Phone” .Phone” service series using FOMA N900iL ASP ASP groupware groupware Internet Highly secure download of electronic value using mobile terminal Linkage by groupware VoIP infrastructure Cordless IP phone using wireless LAN Mobile connection OCN Use of OCN content Examples of ee-commerce in services Electronic money service using mobile terminals NTT DoCoMo (FOMA) Mobile e-commerce system center PDA Contactless smart card Internet Download e-value E-money PC-FOMA videophone, videoconference Secure access to enterprise network $ $ CAFIS E-ticket content Mobile packet access point Linkage with business applications Use of electronic value using contactless smart card Branch Head Office Enterprise system Away from office Use e-money as SF email Business applications Groupware .. . Automatic gate at subway station Buy drinks using e-money Vending machine Pass through admission gate using e-ticket Event hall Concert hall Data FOMA® FOMA® N900iL M1000 PC FOMA® FOMA® N900iL M1000 PC FOMA® FOMA® N900iL M1000 SF: Stored Fare ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 15 Status of competition in Japan Competition has intensified into a price war, making it necessary to create new markets that will generate revenue. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 16 NTT’s actions to deal with the competition ItIt is isurgent urgentfor forNTT NTTto toincrease increaseprofit profitby byincreasing increasingrevenue revenuein inaddition additionto to reducing reducing capital capitaland andoperational operationalexpenditure. expenditure. z Promote broadband & ubiquitous services like FMC and triple play > Revenue shift from telephony Revenue from telephony Revenue from Broadband and ubiquitous services Cost z Establish service delivery platform for new seamless businesses > Expand telecom market z Migrate telephone network to IP > Reduce capital and operational expenditure ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 17 1. The current status and future direction of Japan’s telecommunications market 2. The worldwide telecommunications market and standardization activities 3. NTT’s plans for the deployment of its NGN 4. Future visions for the NGN ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 18 Roles of carriers and vendors and their collaboration Technologies Technologiesare arebeing beingstudied, studied,with withcarriers carrierspresenting presentingrequirements requirementsand andvendors vendors proposing proposingsolutions. solutions.Standards Standardsorganizations organizationsprovide providethe thefora forafor forsuch suchdiscussions. discussions. Discuss Discuss Network Network Architecture Architecture with with carriers carriers and and propose propose solutions solutions to to meet meet the the requirements. requirements. Present Present requirements requirements for for network network components components by by defining defining Network Network Architecture Architecture Requirements Carriers Solutions Vendors Protocol Architecture SNI Testing of interoperability ITU-T, ETSI/TISPAN, ATIS, IETF, 3GPP, OMA, MSF, etc. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 19 Future direction sought by all carriers The Theexternal externalenvironment environmentof of carriers carriersworldwide worldwidehas haschanged changedfrom fromone onewhere wherethe the telephone telephonenetwork networkwas wasthe themain mainnational nationalinfrastructure. infrastructure.All Allcarriers carriersare arestriving strivingto to face facethis thischallenge challengeby byrestructuring restructuring and and transforming transforming themselves themselves into into carriers carriers fit fit for forthe thenew newage. age. Be versatile as a service providing company Technical innovation Changes in lifestyle Provide FMC and triple play services: to meet customer’s demand, extending mobile and Internet features. FMC: Fixed-Mobile Convergence Carriers Restructuring Collaborate with other business areas: e-commerce, banking, physical distribution, home appliances, etc. Changes in telecom policy National infrastructure based on POTS Competition Reduce capital and operational expenditure: by leveraging IP-technology to achieve a competitive price Save cost as a facility operating company Telecom carriers should meet the requirements of the new age by building the NGN ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 20 1. The current status and future direction of Japan’s telecommunications market 2. The worldwide telecommunications market and standardization activities 3. NTT’s plans for the deployment of its NGN 4. Future visions for the NGN ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 21 Approach to NGN Build Build NGN NGN that that is is of of high high quality, quality, flexible flexible and and secure secure Smooth migration from existing fixed-line to IP telephony, and from copper to optical access Develop and spread broadband and ubiquitous services that allow fixedmobile convergence (FMC) Open network that allows collaboration with other carriers and xSPs Expand business opportunities by exploiting broadband and ubiquitous services xSP: Provide new business opportunities Strengthen competitive edge and financial base, and contribute to achievement of u-Japan ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 22 Major targets of NTT’s NGN by 2010 •Migrate •Migrate30 30million millioncustomers customersto tooptical opticalfiber fiberaccess accessand andnext-generation next-generationnetwork network services services •Increase •Increaseannual annualsales salesof ofsolutions solutionsand andnon-traffic non-trafficbusinesses businessesby byUS$ US$55billion billion •Maintain •Maintainthe thesame samelevel levelof ofequipment equipmentinvestment investmentfor forfixed-line fixed-linecommunications communications operations operations(cumulative (cumulativetotal, total,2006-2010: 2006-2010:US$ US$50 50billion) billion) •Reduce •Reduceannual annualcosts costsfor forPSTN PSTNoperation operationby byUS$ US$88billion. billion. Non-traffic businesses Solutions Present 2010 Costs for the fixed-line communications business Reduce annual costs by US$ 8 billion by 2010 Billion US$ Investment in equipment Sales increase Increase annual sales by US$ 5 billion by 2010 Equipment investment for fixed communications operations 9 9.4 8 About equal to the present level Optical fiber access/ Next-generation network Cumulative total: US$ 50 billion Existing fixed-line telephone network 2002 2003 2004 2010 Costs for fixed-line communications business Sales of solutions and nontraffic businesses using the next-generation network Present ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 2010 23 Basic concept of NTT’s NGN Community, e-commerce ASPs and various service players Broadcast, content providers Lifestyle support, home appliance manufacture SNI IP-based network enabling provision of seamless fixed and mobile services Home network SDP IMS Safe, secure, and convenient network equipped with features of both the existing fixed-line telephone and IP networks Disclose Service Node Interface (SNI) to enable various service players to provide a wide array of applications on the NGN NGN Office, hotspot, etc. SDP: Service Delivery Platform IMS: IP Multimedia Subsystem ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 24 Roadmap to building NTT’s NGN Fiscal year Steps in introducing the NGN 2006 2007 2008– STEP 1 Provide optical access to 30M users (End of fiscal 2010) STEP 2 Field trials STEP 3 Core network Construct transit network Construct access networks -deploy core nodes -deploy optical wavelength transmission equipment Seamless integration with mobile network deploy edge nodes Deploy service control functions Service control functions IMS deployment (conforming to ITU standards) Service development Trial services <For limited regions and users> Full-scale development of next-generation services •Broadband Internet access •IP telephony •Multicast transmission for video distribution •Bi-directional video (data) communication •Ethernet services, etc. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 25 Overview of Field Trials of NTT’s NGN •Trial period: One year from Dec. 2006 •Areas: Tokyo and its surroundings and Osaka Various services through tie-ups with IThome appliance manufacturers and ASPs Open connectivity functions IP multicast function NGN Security functions End-to-end quality control Base station IP telephony FMC Video distribution Internet access ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 26 1. The current status and future direction of Japan’s telecommunications market 2. The worldwide telecommunications market and standardization activities 3. NTT’s plans for the deployment of its NGN 4. Future visions for the NGN ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 27 New activities for the NGN Upgrade the fixed-line telephone network to an IP telephone network by applying the latest broadband IP technology - Provide broadband and IP telephony services at attractive prices - Reduce capital and operational expenditure Deploy new broadband services - Provide seamless services, such as triple play and FMC services - Create non-traffic services Create new markets by collaborating with various service players on the network - Disclose Service Node Interfaces - Provide the Service Delivery Platform, to promote collaboration. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 28 Conclusion As one of the first carriers in the world to implement an NGN, NTT will be happy to share with other countries our experiences and expertise of NGN trials and deployment. ITU-T/ITU-D Workshop "Standardization and Development of Next Generation Networks" Dar es Salaam, 3-5 October 2006 29