Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Participatory economics wikipedia , lookup

Fiscal multiplier wikipedia , lookup

Social credit wikipedia , lookup

Non-monetary economy wikipedia , lookup

Steady-state economy wikipedia , lookup

Economics of fascism wikipedia , lookup

Criticisms of socialism wikipedia , lookup

Consumerism wikipedia , lookup

Transformation in economics wikipedia , lookup

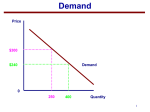

Notes on Chapter One Dr. Ibrahem Hasan AI-ezee Definition of Economics A- Economic questions arise because we face scarci~- we all want more we can get. In other words, scarcity exists when people wants exceed their ability to satisfy their wants. I. II. Because we are unable to satisfy all of our wants, we must make choices. Incentives are the rewards that encourage us, or the penalties that discourage us from taking an action. The incentives that we face will influence the choices that we make when dealing with scarcity B- Economics is a social science that studies the choices that individuals, businesses, government, entire society that make as the y cope with scarcity. It can be divided into two areas of studies: 1. Microeconomics is the study of choices that individuals and businesses make; these choices interact in the markets, and the influence of governments. Examples: Why are people buying more from (x) good and fewer from (y)? How tax imposed on costumers affect demand of particular good. 2. Macroeconomics: is the study of the performance of the national economy and the global economy. Examples: Fluctuations in the national economy The inflation rate. The unemployed rate. Productivity. The interest rate. The government budget deficit. The foreign trade deftest. Two Big Economic Questions Two big questions summarize the scope of economics: First: How do choices end up determining? What, How, and For whom goods and services get produced The three questions are explained briefly; I. What to produce: Producing some kind of goods and services will be changed over time, depending on the needs of the society and the scarcity of the available resources. II. What to produce: This question is related to how goods and services are produced by using productive resources. Productive resources are grouped into four categories: Land: It is a gift of God (nature) to produce goods and services. Labour: It is the work time and effort devoted by people to producing goods and services. Capital: It is the tools, instruments, machines, building, etc. that businesses use to produce goods and services. Note: Financial capital such as money, bonds, and stocks are not capital because they are not productive resources. Entrepreneurship: It is the human resource that organize factors of production (land, labour, and capital): It comes up with: I. New ideas about what and how to produce, II. Make business decisions, and III. Bear the risks that arise from these business decisions. 3. For whom to produce: Who gets the goods and services that are produced; depend actually on the income that people earn. A large income enables a person to buy large quantities of goods and services. A small income leaves a person with few options and small quantities of goods and services. People earn their incomes by selling the services of the factors of production they own: . Land earns rent. Labour earns wages. Capital earns interest. Entrepreneurship earns profit. Second: When do choices made in the pursuit of self- interest, also promote the social interest? This is related to answer the following questions: 4. Are goods and services produced, and the quantities in which they are produced, the right ones? Always people make choices in their own self-self interest. They make choices they think are the best for their own well-being. 5. Do the factors of production employed get used in the best possible way? 6. Do the goods and services that we produce go the people who benefit most from them? Note: When people make self-interested choices that are the best for society, they make choices that are considered in the social-interest. The Economic Way of Thinking This subject is concerned with the economists thinking about the questions we just reviewed and go about seeking answers to them. Choices and tradeoffs A: Because we face scarcity .we must make choices. And when we make a choice, we select from available alternatives, which create a tradeoff. Tradeoffs include the 'what, how, and for whom tradeoffs'. Tradeoff is an exchange- giving up thing to get something else. And it means exchange more of something for less of something else. A classic tradeoff could be explained by the terminology Guns versus Butter. Which means that every country faces such tradeoff when deciding how much of its factors of production should go toward producing National Security versus goods and services like foods and shelter. B. What, How. and for Whom 'tradeoffs' I. 'What' Tradeoffs arise when people choose how to spend their incomes, when governments choose how much to spend their tax revenues, and when businesses choose what to produce with their factors of production. 2. 'How' tradeoffs arise when businesses and government choose among alternative technologies. For example businesses might switch to using robots rather than labour in assembly lines, thereby effectively trading off labour for capital. 3. 'For Whom' Tradeoffs arise when choices change the distribution of goods and services produced across individuals. Government redistribution of income from the rich to the poor changes the incentives facing owners of productive resources, creating a Big Tradeoff: the tradeoff between efficiency and equity. C. Choice Bring Changes: The results arising from all the choices made in the society will influence the incentives surrounding the future choices by other people, businesses and government. For example; 1. Consuming decisions to consume less and save more increase the funds that are available for business to borrow and invest, increasing output. 2. Workers ' decision to decrease leisure time to acquire human capital to increase their income as well as government tax revenues, increasing how much public services the government chooses to offer. 3. iii. Businesses decisions to increase Research and Development (R&D) for innovative products rather than to increase current production improve investors expectations, increase saving. D. Opportunity Cost: Thinking about a choice as a tradeoff emphases how cost is an opportunity forgone: The opportunity cost is highest- valued alternative that we give up to get something. For example, the opportunity cost of attending college include not only the money cost of books, tuition and (perhaps} room and board, but also the money income forgone from not being able to work full time, as well as the leisure time lost from studying nights and weekends. E. People make choices at the margin. Making choices at the margin means people look at tradeoffs that arise from making small changes in an activity . Marginal Benefit is the benefit arises from an increase in an activity .For example, if you are studying four nights a week your grade in economics is 3.0. Increasing your study by extra one night your grade is 3.5. The marginal benefit is 0.5. Marginal Cost is the cost arises from an increase in an activity .For example, the cost of increasing your study time by one night a week is the cost of the additional night not spent with your friends (if that is your best alternative use of the time}. Economics is a Social Science A. Economists try to discover how the economic world works, and in pursuit of this goal, they distinguish between two type of statements Positive statements make a claim about 'what is' and can be tested to determine whether they are valid. Normative statements make a claim of 'what ought to be.' Such a statement is an opinion and cannot be tested for validity. Health-care reform provides example of the distinction. ' Universal health care will cut the amount of work time lost to illness' is a positive statement. Every Bahraini should have equal access to health care is a normative statement. Demand law is a positive statement, but questions about unemployment and inflation are normative statements. B. Economists build Models: Economists observe and measure economic activity, build economic models, and test their models. An Economic Model is a description of some aspect of the economic world that includes only those features of the world that are needed for the purpose at hand. C. Economists test their models An economic theory is a generalization that summarizes what we think we understand about the economic choices that people make and the performances. of industries and entire economies.