Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

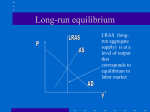

Ragan/Lipsey 11th edition (Chapter 25) Question 4 a) Beginning in a long-run equilibrium with Y=Y*, suppose there is an increase in households’ desired saving (which is equivalent to a decrease in desired consumption). The AD curve shifts to the left, reducing both real GDP and the price level. The short-run effect of the increase in desired saving is a decline in the overall level of economic activity and the creation of a recessionary gap. b) With Y<Y*, the excess supply in factor markets pushes wages and other factor prices down, thus reducing firms’ unit costs. The AS curve (eventually) begins to shift down and to the right, returning real GDP to the unchanged level of potential output (at a lower price level than in the initial long-run equilibrium). c) In the long run, after factor prices have fully adjusted, there is no change in real output since the economy returns to Y*. But there is a change in the composition of output that may have implications for the future path of potential output. Comparing the two long-run equilibria, we see that the increase in desired saving has reduced the price level in the long run. The lower price level has three effects. First, it increases private-sector wealth and thus increases consumption (partly offsetting the initial decline in consumption in part (a)). Second, at given values for the exchange rate and foreign prices, the lower domestic price level increases net exports. The third effect, which we will explain in detail in Chapter 28 and 29, is that the lower price level causes the interest rate to fall, thus stimulating domestic investment. In summary, the new long-run equilibrium has higher NX and I than the initial longrun equilibrium. As we explained in Chapter 22, this implies greater net asset accumulation and thus greater growth of potential output in the future.