Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

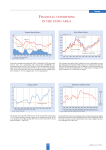

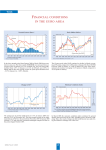

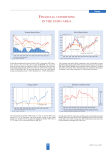

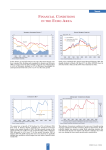

Trends FINANCIAL CONDITIONS IN THE EURO AREA In the three-month period from October to December 2009 short-term interest rates declined. The three-month EURIBOR rate decreased from an average 0.74% in October to 0.71% in December. Yet the ten-year bond yields grew from 3.80% in October to 3.88% in December. In the same period of time the yield spread increased from 3.06% (October) to 3.17% (December). The German stock index DAX grew in December 2009, averaging 5,957 points compared to 5,415 points in October. The Euro STOXX also increased from 2,865 in October to 2,908 in December. The Dow Jones International also grew, averaging 10,433 points in December compared to 9,857 points in October. The annual rate of growth of M3 decreased to – 0.2% in November 2009, from 0.3% in October. The three-month average of the annual growth rate of M3 over the period from September 2009 to November 2009 declined to 0.6%, from 1.6% in the period August 2009 to October 2009. Between April and October 2009 the monetary conditions index remained rather stable after its rapid growth that had started in mid-2008, signalling greater monetary easing. In particular, this is the result of decreasing real short-term interest rates. CESifo Forum 4/2009 64 Trends EU SURVEY RESULTS According to the second Eurostat estimates, GDP increased by 0.4% in the euro area (EU16) and by 0.3% in the EU27 during the third quarter of 2009, compared to the previous quarter. In the second quarter of 2009 the growth rate had amounted to – 0.1% for the euro area and – 0.3% for the EU27. Compared to the third quarter of 2008, i.e. year over year, seasonally adjusted GDP declined by 4.0% in the euro area and by 4.3% in the EU27. In December 2009, the Economic Sentiment Indicator (ESI) for the EU27 and the euro area continued to improve for nine consecutive months since its trough in March 2009. In this month the ESI increased by 4.1 points in the EU27 and by 2.5 points in the euro area, to 92.0 and 91.3 respectively. Yet, in both areas, the ESI level is still below the longterm averages. * The industrial confidence indicator is an average of responses (balances) to the questions on production expectations, order-books and stocks (the latter with inverted sign). ** New consumer confidence indicators, calculated as an arithmetic average of the following questions: financial and general economic situation (over the next 12 months), unemployment expectations (over the next 12 months) and savings (over the next 12 months). Seasonally adjusted data. Managers’ assessment of order books improved from – 51.4 in October to – 46.6 in December 2009. In September 2009 the indicator had reached – 55.4. Capacity utilisation increased to 71.4 in the fourth quarter of 2009 from 70.2 in the previous quarter. In December 2009, the industrial confidence indicator increased by 3 points in the EU27 and the euro area (EU16), while the consumer confidence indicator increased by 1 point also in the both areas. However, these indicators stood below the long-term average in both areas in September. 65 CESifo Forum 4/2009 Trends EURO AREA INDICATORS The Ifo indicator of the economic climate in the euro area (EU16) improved in the fourth quarter of 2009 for the third time in succession. Its rise is primarily the result of more favourable expectations for the coming six months, but also the assessments of the current economic situation have improved slightly. This shores up hopes that the recovery in the euro area economy will continue in the first half of 2010. The exchange rate of the euro against the US dollar averaged 1.46 $/€ in December 2009, a decrease from 1.49 $/€ in November. (In October 2009 the rate had amounted to 1.48 $/€ .) Euro area (EU16) unemployment (seasonally adjusted) amounted to 10.0% in November 2009, compared to 9.9% in October. It was 8.0% in November 2008. EU27 unemployment stood at 9.5% in November 2009, compared to 9.4% in October. The rate was 7.5% in November 2008. In November 2009 the lowest rate was registered in the Netherlands (3.9%) and Austria (5.5%). Unemployment rates were highest in Latvia (22.3%) and Spain (19.4%) in November 2009. Euro area annual inflation (HICP) was 0.5% in November 2009, compared to – 0.1% in October. This is an evident decrease from a year earlier, when the rate had been 2.1%. The EU27 annual inflation rate reached 1.0% in November, up from 0.5% in October. A year earlier the rate had amounted to 2.8%. An EU-wide HICP comparison shows that in November 2009 the lowest annual rates were observed in Ireland (– 2.8%), Estonia (– 2.1%) and Latvia (– 1.4%), and the highest rates in Hungary (5.2%), Romania (4.6%) and Poland (3.8%). Year-on-year EU16 core inflation (excluding energy and unprocessed foods) fell slightly to 1.0% in November from 1.1% in September. CESifo Forum 4/2009 66