Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

A Day’s Work for

New Dimensions

an International Consulting Firm

Glenn Meyers

Insurance Services Office, Inc.

CAS/ARIA Financial Risk

Management Seminar

DFA - Dynamic Financial Analysis

• Coined by the CAS in 1994.

• Best defined in terms of the problems it

seeks to solve.

– How much capital does an insurer need?

– For how much time is the capital needed?

– What decisions does an insurer make to

provide the greatest return on its capital?

• Underwriting

• Asset management (Include hedges)

Outline of Talk

• Multi-dimensional aspects of insurer capital

management

• Provide simple (perhaps artificial) examples

focusing on particular dimensions.

– Short and long tailed lines

– Catastrophe options and reinsurance

• Describe (but not solve) a multi-dimensional

insurer problem in capital management.

• Compare approach with efficient frontier

methods.

Assignment #1

Lineland Life Insurance Company

•

•

•

•

Writes one life insurance policy

Face value $1

t is the term of the policy

Mortality assumptions

– Probability of death in [0,t] = q

– Uniform distribution of deaths within [0,t]

Assignment #1

Lineland Life Insurance Company

• Investors provide $1 of capital.

• Capital is invested at rate I

compounded continuously.

• In return for exposing the capital to loss

they demand a return of R

compounded continuously.

R > I

• Find minimum premium, P, it must get.

Assignment #1

Lineland Life Insurance Company

Case 1 - Claim occurs at time T

The return is a continuous annuity of I

R T

1 e

PV withclaim I

R

E PV with claim

R

t 1 e

0 I

R

z

F

G

H

q

d

t

I

1 e R t

q

1

R

t R

I

J

K

Assignment #1

Lineland Life Insurance Company

Case 2 - Claim does not occur

Return = PV[Annuity] + PV of Capital

R t

1 e

PV without claim I

R

e

R t

F

1 e

E PV without claim a

1 qf G

H

R t

I

R

e

R t

I

J

K

Assignment #1

Lineland Life Insurance Company

• Receives P immediately.

• Receives annuity until claim occurs or

the term ends.

1 = P + E[PV with Claim] + E[PV without Claim]

Assignment #1

Lineland Life Insurance Company

I

R

q

6%

10%

0.100

t

P

P-q

1

2

3

4

5

6

7

0.131

0.160

0.185

0.208

0.229

0.248

0.264

0.031

0.060

0.085

0.108

0.129

0.148

0.164

P increases when capital must be held longer.

Background - Capital Requirements

Define Terms

X = Random Insurer Loss

F( x) = Pr{ X x}

f ( x) = F ( x)

af

LEV L

z

a1 F(L)f

L

x

f

(

x

)

dx

L

0

= Standard Deviation of X

C = Required Insurer Capital

Background - Capital Requirements

Three Formulas

#1 Probabililty of Ruin

F(C E[ X ]) 1

is determined by judgment of insurer

management.

Insurer management always knows what

the rating agencies - NAIC, Best, S&P

think they should have.

Value at Risk -- VaR = C+E[X]

Background - Capital Requirements

Three Formulas

#2 Expected Policyholder Deficit (EPD)

a

f

LEV C E[ x]

1

E[ X]

is determined by judgment of insurer

management.

Sensitive to amount of insolvency

Background - Capital Requirements

Three Formulas

#3 Standard Deviation Formula

C T

T is determined by judgment of insurer

management.

Normal approximation to ruin formula, but

you can use this formula as is.

Easiest to work with

Assignment #2

Lineland Property Insurance Company

• Losses have a Gamma(100,100)

distribution.

• Claims settle quickly

– Time value of money is not an issue.

• Investors expect 10% ROE.

• Find the Cost of Capital.

Gamma Distribution Mathematics

Cumulative Distribution Function

a f

F( x) ; x /

a

f

GammaDist x, , , TRUE

Expected Value

a f

af

1

EX

Excel

Formula

Gamma Distribution Mathematics

Limited Expected Value (LEV) Function

a f a

af

1

LEV L

1;L / L 1 1;L /

f b a

fg

a

f

xa

1 GammaDist( x, , , TRUE)f

exp GammLn( 1) GammaLn() GammaDist( x, 1, , TRUE)

Variance

E X2

a f

af

2 2

2 1

2 Var X E X 2 E X

a f

2

2

Excel

Formula

Assignment #2

Lineland Property Insurance Company

Probability of Ruin

• E[X] = 10,000

• F(12,472) = 0.99

Capital = 2,472 @ 1.0% Level

• Cost of capital = 247

Assignment #2

Lineland Property Insurance Company

Expected Policyholder Deficit

• E[X] = 10,000

• LEV[12,091] = 9,990

LEV[12,091]

EPD 1

0.0010

E[ X]

Capital = 2,091 @ 0.10% Level

• Cost of Capital = 209

Assignment #2

Lineland Property Insurance Company

Standard Deviation

• E[X] = 10,000

• Std[X] = 1000

• Select T = 2.33

Capital = 2,330

• Cost of Capital = 233

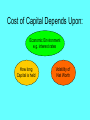

Cost of Capital Depends Upon:

Economic Environment

e.g. interest rates

How long

Capital is held

Volatility of

Net Worth

Parameter Uncertainty

for Gamma(,)

• Let be a random variable

– E[] = 1

– Var[] = b

• Select at random

• Conditional distribution given

Gamma(,)

Parameter Uncertainty

for Gamma(,)

A simple, but nontrivial example

1 1 3b, 2 1, 3 1 3b

k p k

p

k

p

Pr 1 Pr 3 1 / 6 and Pr 2 2 / 3

E[] = 1 and Var[] = b

Assignment # 2´

Capital Requirements with

Parameter Uncertainty

b 0.02

1 100 1 75.51

2 100 2 100.00

3 100 2 124.49

a

af

f

a

f a

, x / 1 2 , x / 2 , x / 3

FU x

6

3

6

f

Assignment # 2´

Capital Requirements with

Parameter Uncertainty

Probability of Ruin

• E[X] = 10,000

• FU(14,443) = 0.99

Capital = 14,443 @ 1.0% Level

• Cost of capital = 444

Assignment # 2´

Capital Requirements with

Parameter Uncertainty

Probability of Ruin

Capital

Capital

Threshold w/o PU

with PU

1.0%

2,472

4,443

Expected Policyholder Deficit

Capital

Capital

Threshold w/o PU

with PU

0.10%

2,091

4,129

Standard Deviation

Capital

Capital

Threshold w/o PU

with PU

2.33

2,330

4,049

Assignment #3

Lineland Property Insurance Company

Considers Renewing a Policy

• The renewal business has a Gamma(100,1)

loss distribution.

• Lineland has a Gamma(100,99) loss

distribution without the renewal.

Property of the Gamma Distribution

• Lineland has a Gamma(100,100) loss

distribution with the renewal.

This Property Assumes Independence

Assignment #3

Lineland Property Insurance Company

Considers Renewing a Policy

• What is the marginal capital needed for the

renewal business?

• Calculate capital needed without the business.

• Calculate capital needed with the business.

• Marginal capital is the difference.

Assignment #3´

Find Marginal Capital

Assuming Parameter Uncertainty

• The random variable affects all business

(including renewal) simultaneously.

• The renewal’s parameter changes at the

same time as the for the remaining business.

• The renewal’s losses are correlated with the

rest of the losses.

In case you are interested -- = 0.195

Assignment #3 and #3´

Results

Probability of Ruin @ 1.0%

C

b

C-R

C

0.00 2,460.59 2,472.26 11.67

0.02 4,409.12 4,443.25 34.13

Expected Policyholder Deficit @0.1%

C

b

C-R

C

0.00 2,083.58 2,091.11 7.53

0.02 4,100.04 4,129.19 29.15

Standard Deviation @ 2.33

C

b

C-R

C

0.00 2,318.32 2,330.00 11.68

0.02 4,015.75 4,049.11 33.66

With Parameter

Uncertainty

Total Capital

Double

Marginal Capital

Triple +

How do you use the

marginal cost of capital?

• Allocate the total cost of capital in proportion

to the marginal cost of capital.

– No consensus among actuaries yet.

• Add the allocated cost of capital to the

expected loss and expense to see if you can

make money at the “going market premium.”

• Can be done at individual insured level, or the

line of business level.

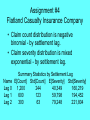

Assignment #4

Flatland Casualty Insurance Company

• Claim count distribution is negative

binomial - by settlement lag.

• Claim severity distribution is mixed

exponential - by settlement lag.

Name

Lag 0

Lag 1

Lag 2

Summary Statistics by Settlement Lag

E[Count] Std[Count] E[Severity] Std[Severity]

1,200

244

40,349

160,219

600

123

59,798

194,452

300

63

79,248

221,804

Assignment #4

Flatland Casualty Insurance Company

Outstanding Aggregate Loss Statistics

Lags 0-2

Lags 1-2

Lag 2

Aggregate Loss Statistics for OS Losses

E[Loss]

99th Pct

EPD = 0.1% Std Dev

108,071,943 158,505,938 155,520,667 19,835,337

59,653,299 91,387,990 90,579,282 12,265,291

23,774,319 40,533,916 41,250,295 6,283,149

The aggregate loss model included parameter uncertainty

affecting all claim count distributions simultaneously.

(g =.02 - analogous to b =.02 above.)

Assignment #4

Flatland Casualty Insurance Company

Capital is released over time as losses are paid.

Required Capital for OS Losses

Pr{Ruin}@1.0% [email protected]% Std Dev x 2.33

Lags 0-2

50,433,995

47,448,724

46,216,335

Lags 1-2

31,734,691

30,925,983

28,578,127

Lag 2

16,759,597

17,475,976

14,639,737

Assignment #4

Flatland Casualty Insurance Company

What is the cost of providing the capital?

i = Interest rate on invested capital

r = Rate of return needed to attract capital.

C0 = Capital needed at beginning of year 0.

Re lease t C t 1 (1 i) C t

The cost of capital, R, satisfies:

3 Re lease

t

C0 R

t

r

t 1 1

a f

Assignment #4

Given i = 6% and r = 10%

What is the cost of providing the capital?

Required Capital for OS Losses

Pr{Ruin}@1.0% [email protected]% Std Dev x 2.33

Lags 0-2

50,433,995

47,448,724

46,216,335

Lags 1-2

31,734,691

30,925,983

28,578,127

Lag 2

16,759,597

17,475,976

14,639,737

Time t

1

2

3

Expected Return at Time t

21,725,344

19,369,665

20,411,187

16,879,175

15,305,566

15,653,078

17,765,172

18,524,534

15,518,122

Cost of

Capital

3,386,713

3,272,953

3,065,288

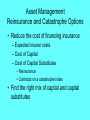

Asset Management

Reinsurance and Catastrophe Options

• “Value will be determined not by the ability

of an [insurance] enterprise to accumulate

capital and sit on it.

• Rather it will be determined by a company’s

franchise with its customers and its ability to

originate risk.

• In this scenario the capital markets become

the more efficient warehouse of [insurance]

risk.”

Asset Management

Reinsurance and Catastrophe Options

• Reduce the cost of financing insurance

– Expected insurer costs

– Cost of Capital

– Cost of Capital Substitutes

• Reinsurance

• Contracts on a catastrophe index

• Find the right mix of capital and capital

substitutes

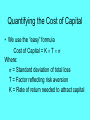

Quantifying the Cost of Capital

• We use the “easy” formula

Cost of Capital = K T

Where:

= Standard deviation of total loss

T = Factor reflecting risk aversion

K = Rate of return needed to attract capital

Quantifying Basis Risk

Ran RMS cat model through insurers and index.

Event

1

2

3

4

5

6

7

8

9

10

Index

Value

100.0

89.04

87.56

83.48

83.20

82.15

80.95

80.55

79.19

77.48

Event

Probability

0.00000121

0.00000121

0.00000181

0.00000702

0.00000702

0.00000466

0.00000791

0.00005060

0.00000702

0.00000181

Max Event

Contract

Direct

Reinsurance Event Loss

Probability

Value

Insurer Loss

Recovery

Given Max

0.00000121 1,125,200,000 1,212,550,269 16,000,000

71,350,269

0.00000121 1,021,700,000 1,509,161,589 16,000,000

471,461,589

0.00000181 1,021,700,000 1,303,694,653 16,000,000

265,994,653

0.00000702 939,300,000

761,956,629 16,000,000 (193,343,371)

0.00000702 939,300,000

734,137,782 16,000,000 (221,162,218)

0.00000466 939,300,000

735,660,852 16,000,000 (219,639,148)

0.00000791 939,300,000 1,004,861,128 16,000,000

49,561,128

0.00005060 939,300,000 1,071,076,934 16,000,000

115,776,934

0.00000702 856,900,000

688,269,904 16,000,000 (184,630,096)

0.00000181 856,900,000 1,652,933,116 16,000,000

780,033,116

+ about 9000 more

• Compare variability before and after

• Is the risk reduction worth the cost?

Minimize Sum of

Cost Elements

• Insurer Capital

Cost of Capital = K T (Net Losses)

• Reinsurance

Transaction Cost + Expected Cost

• Cat index contracts

Transaction Cost + Expected Cost

Use cat model results to back out transaction costs.

References

Missing transaction costs are in the first paper.

• “The Cost of Financing Catastrophe

Insurance” by Glenn Meyers and John Kollar 1998 DFA Call Paper Program

• Catastrophe Risk Securitization: Insurer

and Investor Perspectives” by Glenn Meyers

and John Kollar - 1999 CAS Spring Meeting Call

Paper Program

Assignment #5

Analyze Three Insurers

• Insurer #1 - A medium national insurer

Highly correlated with the index

• Insurer #2 - A large national insurer

Moderately correlated with the index

• Insurer #3 - A small regional insurer

Slightly correlated with the index

Search for Best Strategy to

Minimize Cost of Financing

Insurance

• Search for the combination of index and

reinsurance purchases that minimizes

total cost of providing insurance.

Questions

• How many index contracts at each

strike price?

• What layer of reinsurance?

Results of Search

Contract

Range

5-20

25-40

45-55

60-70

75-85

90-100

Number of Index Contracts

Insurer #1 Insurer #2 Insurer #3

47,400

93,100

0

74,400

118,100

6,300

59,500

67,900

0

47,600

28,600

0

81,400

545,100

0

37,200

634,800

0

Reinsurance

Retention 73,000,000 457,000,000 54,000,000

Limit

13,000,000 36,000,000 105,000,000

Financing With Reinsurance

and Catastrophe Options

Expected Net Loss

Cost of Capital

Cost of Reinsurance

Cost of Catastrophe Options

Cost of Financing Insurance

Insurer #1

Insurer #2 Insurer #3

16,315,629 62,086,995 1,464,410

53,470,927 143,662,761 12,914,922

2,088,287

1,848,530 1,726,342

22,252,015 42,409,101

249,427

94,126,858 250,007,387 16,355,100

Financing Without Reinsurance

and Catastrophe Options

Expected Net Loss

Cost of Capital

Cost of Reinsurance

Cost of Catastrophe Options

Cost of Financing Insurance

Insurer #1

Insurer #2 Insurer #3

34,839,348 95,417,229 2,385,629

68,768,384 166,962,499 15,356,683

0

0

0

0

0

0

103,607,732 262,379,728 17,742,312

Differences in Costs

Without Reins & Options

With Reins & Options

Difference

Pct Difference

Insurer #1

Insurer #2 Insurer #3

103,607,732 262,379,728 17,742,312

94,126,858 250,007,387 16,355,100

9,480,874 12,372,341 1,387,212

9.2%

4.7%

7.8%

Assignment #6

Spaceland Property and Casualty

• Short tailed property exposure

– Include catastrophe exposure

• Long tailed casualty exposure

– Include unsettled claims from prior years

• Capital Management Questions

– Catastrophe options/reinsurance?

– Casualty reinsurance?

Assignment #6

Spaceland Property and Casualty

Underwriting Management Decisions

• Allocate the cost of capital to the lines of

insurance - in proportion to the marginal

cost of capital.

• Allocate the cost of reinsurance and/or

catastrophe options to the lines of

insurance - in proportion to the marginal

costs.

Assignment #6

Information and Technology

Requirements

• An Aggregate Loss Model

• Size of loss distributions by settlement lag

• Correlation structure between lines of

insurance

• A catastrophe model

• Exposure underlying catastrophe index

References

• “Underwriting Risk” by Glenn Meyers

– 1999 CARe Call Paper Program

• “Estimating Between Line Correlations

Generated by Parameter Uncertainty” by

Glenn Meyers

– 1999 DFA Call Paper Program

• These papers should be eventually

available at CAS web site.

• Currently available on my personal web site

http://www.crimcalc.com/glenn.htm

Relationship Between this

Capital Cost Allocation Method

and the Efficient Frontier Methods

• They are equivalent

– (loosely speaking)

• I say “loosely speaking” because:

– There is a lot of loose speaking about the

meaning of “risk.”

– There is a lot of loose speaking about the

meaning of “allocated cost of capital.”

Relationship Between the

Capital Cost Allocation Methods

and the Efficient Frontier Methods

• The intuition

• Allocated cost of capital depends upon

marginal risk.

• Making decisions that yield a higher

return on marginal capital moves you

closer to the efficient frontier.

Relationship Between the

Capital Cost Allocation Methods

and the Efficient Frontier Methods

• Some History from PCAS

– Kreps: Risk loads from marginal capital

requirements, 1990

– Meyers: Risk loads from efficient frontiers

(mimic CAPM), 1991

– Heckman: Kreps and Meyers are

equivalent, 1993 (CAS Forum)

– Meyers: Cat risk loads from marginal

capital requirements, 1997

Relationship Between the

Capital Cost Allocation Methods

and the Efficient Frontier Methods

If two are equivalent, why did I switch?

• Easier to explain

• Easier to extend

– To different measures of risk

– To different capital holding times