Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

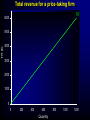

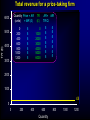

Chapter 5&6 Main Lecture on Revenue and Perfect Competition Revenue • We have looked at Production and then Cost so we have anaylsed our technical capabilities and the costs of producing output, • on average • and at the margin (one more unit) • Now we have to examine what we get for an additional unit REVENUE • Thus we need to defining total, average and marginal revenue • We start by examining revenue curves when firms are price takers • By this we mean that firms are small relative to the total market and that they do not have much influence over the price charged. • In such a market if they raise price people will go elsewhere… • … and if they reduce price (even if it were profitable) they would not be able to cope with the resultant demand. Revenue • That is, they perceive the price they can receive as constant. • So as far as they are concerned the demand curve is horizontal. • That means they believe: • They can sell as much as they want at the going price. – average revenue (AR) – marginal revenue (MR) S AR, MR (£) Price (£) Deriving a firm’s AR and MR: price-taking firm Pe D O Q (millions) (a) The market O Q (hundreds) (b) The firm S AR, MR (£) Price (£) Deriving a firm’s AR and MR: price-taking firm Pe D O Q (millions) (a) The market O Q (hundreds) (b) The firm REVENUE • Defining total, average and marginal revenue • Revenue curves when firms are price takers (horizontal demand curve) – average revenue (AR) – marginal revenue (MR) – total revenue (TR) Total revenue for a price-taking firm Quantity (units) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 Price 5 5 5 5 5 5 5 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm Quantity (units) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 Price 5 5 5 5 5 5 5 TR (£) 0 1000 2000 3000 4000 5000 6000 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm Quantity (units) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 Price 5 5 5 5 5 5 5 TR TR (£) 0 1000 2000 3000 4000 5000 6000 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm TR 6000 TR (£) 5000 4000 3000 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm Quantity Price = AR (units) = MR (£) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 5 5 5 5 5 5 5 TR (£) AR= TR/Q 0 1000 2000 3000 4000 5000 6000 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm Quantity Price = AR (units) = MR (£) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 5 5 5 5 5 5 5 TR (£) AR= TR/Q 0 1000 2000 3000 4000 5000 6000 5 5 5 5 5 5 5 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm Quantity Price = AR (units) = MR (£) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 5 5 5 5 5 5 5 TR (£) 0 1000 2000 3000 4000 5000 6000 AR= MR TR/Q 5 5 5 5 5 5 5 2000 1000 0 0 200 400 600 Quantity 800 1000 1200 Total revenue for a price-taking firm Quantity Price = AR (units) = MR (£) 6000 0 200 400 600 800 1000 1200 TR (£) 5000 4000 3000 5 5 5 5 5 5 5 TR (£) 0 1000 2000 3000 4000 5000 6000 AR= MR TR/Q 5 5 5 5 5 5 5 5 5 5 5 5 5 5 2000 1000 £5 0 0 200 400 600 Quantity 800 1000 1200 Mathematics of Revenue: Total Revenue Average Revenue TR P.Q TR P.Q P Q Q Marginal Revenue When P is constant d (TR) d ( P.Q) P dQ Q When is a firm a price taker? • PERFECT COMPETITION • Assumptions – firms are price takers – treat P as constant – freedom of entry – identical products – perfect knowledge VERY Short-run equilibrium of industry and firm under perfect competition P £ S D O O Q (millions) (a) Industry VERY Short-run equilibrium of industry and firm under perfect competition P £ S Pe D O O Q (millions) (a) Industry VERY Short-run equilibrium of industry and firm under perfect competition P £ S Pe D = AR = MR AR D O O Q (millions) (a) Industry q (thousands) (b) Firm VERY Short-run equilibrium of industry and firm under perfect competition P £ MC S Pe D = AR = MR AR D O O Q (millions) (a) Industry qe q (thousands) (b) Firm Very Short-run equilibrium of industry and firm under perfect competition P £ MC S Pe D = AR = MR AR AC D O O Q (millions) (a) Industry At what level of output should the firm Produce? AC qe q (thousands) (b) Firm Produce where MR = MC RULE ALWAYS P £ MC S Pe D = AR = MR AR AC D O O Q (millions) (a) Industry AC qe q (thousands) (b) Firm At Qe how much does profit does the firm make? P £ MC S Pe D = AR = MR AR AC D O O Q (millions) (a) Industry AC qe q (thousands) (b) Firm At Qe how much does profit does the firm make? P £ MC S Pe D = AR = MR AR AC D O O Q (millions) (a) Industry AC qe q (thousands) (b) Firm At Qe how much does profit does the firm make? P £ MC S Pe D = AR = MR AR AC D O O Q (millions) Area = (a) Industry (AR-AC)*qe AC Qe Q (thousands) (b) Firm Supernormal Profits • What was included in total costs when we drew the TC and AC curves? • We included the cost of capital, labour, and raw, materials and ……………. • An appropriate return for the entrepreneur for his or her labour, capital invested and risk • So what does the yellow area represent? • (AR – AC)*qe = • Supernormal profit Supernormal Profit P £ MC S Pe D = AR = MR AR AC D O O Q (millions) (a) Industry AC qe q (thousands) (b) Firm PERFECT COMPETITION – Produce where MR = MC – Under perfect Competition P = MR – So MR= P = MC – possible supernormal profits = (AR-AC)*q Very Short-run equilibrium of industry and firm under perfect competition Supernormal Profit P £ MC S P D = AR = MR AR AC D O O Q (millions) (a) Industry AC qe q (thousands) (b) Firm P So supernormal profits attract more firms to the industry. Before S = Qe= n* qe now S = Q1= (n+a) * qe S P MC £ D = AR = MR AR AC D O O Q (millions) (a) Industry AC qe q (thousands) (b) Firm Before S = Qe= n* qe now S = Q1= (n+a) * qe So Supply curve moves out! P S P S1 MC £ D = AR = MR AR AC D O Qe Q1 Q (millions) (a) Industry O AC Q Q (thousands) (b) Firm Price falls P S Pe S1 MC £ D = AR = MR AR AC D O O Q (millions) (a) Industry AC Qe Q (thousands) (b) Firm P S Pe S1 MC £ AR AC D = AR = MR D O O Q (millions) (a) Industry AC Q (thousands) (b) Firm .. And a new LONG RUN equilibrium is established at Pe,Qe P S P S1 MC £ AR AC Pe D = AR = MR D O O Q (millions) (a) Industry AC Qe Q (thousands) (b) Firm PERFECT COMPETITION • Short-run supply curve of industry • Long-run equilibrium of the firm – all supernormal profits competed away – Since AR=AC and – (AR-AC)*Q=0 LONG RUN Equilibrium under Perfect Competition requires that AR=P=MR=MC=AC P S1 MC £ D = AR = MR Pe Pe D O O Q (millions) (a) Industry AC Qe Q (thousands) (b) Firm Suppose now demand falls. What happens to supply now? P MC S1 £ Pe P0 P1 D1 O D0 O Q (millions) (a) Industry Qe Q (thousands) (b) Firm AC Suppose now demand falls. Our same MR = MC rule applies, but there is one more consideration P MC S1 £ Pe P0 P1 D1 O D0 O Q (millions) (a) Industry Qe Q (thousands) (b) Firm AC Our same MR = MC rule applies, but there is one more consideration We need to check where the AVC curve lies. Why? P MC S1 AC £ AVC Pe P0 P1 D1 O D0 O Q1 Q 0 In this case P > AVC so will continue to produce. By doing so, cover AVC and make some contribution to covering Fixed Costs Our same MR = MC rule applies, but there is one more consideration We need to check where the AVC curve lies. Why? P MC S1 £ AVC Pe P0 P1 D1 O D0 O Q1 Q 0 But overall making a (supernormal) loss = FC – (P-AVC) AC What if P is below AVC? P MC S1 £ AVC Pe P0 P1 D1 O D0 O AC Qe In this case we can’t cover variable costs, so better to close down and only lose FC Deriving the short-run supply curve S P £ MC a P1 D1 = MR1 D1 O O Q (millions) (a) Industry Q1 Q (thousands) (b) Firm Deriving the short-run supply curve S P £ MC a P1 b P2 D1 = MR1 D2 = MR2 D1 D2 O O Q (millions) (a) Industry Q2 Q (thousands) (b) Firm Deriving the short-run supply curve S P £ MC a P1 D1 = MR1 D2 = MR2 b P2 c P3 D1 D3 O AVC D2 O Q (millions) (a) Industry D3 = MR3 Q3 Q (thousands) (b) Firm Deriving the short-run supply curve S P £ S a P1 b P2 c P3 D1 D3 O D1 = MR1 D2 = MR2 D3 = MR3 AVC D2 O Q (millions) (a) Industry Q (thousands) (b) Firm PERFECT COMPETITION • Short-run supply curve of industry • Long-run equilibrium of the firm – all supernormal profits competed away – long-run industry supply curve What happened to Supply here in the Long Run P MC S S £ 1 LRS D = AR = MR Pe Pe D O D1 O Q (millions) (a) Industry AC Qe Q (thousands) (b) Firm Various long-run industry supply curves under perfect competition S1 P a D1 O Q (a) Constant industry costs Various long-run industry supply curves under perfect competition S1 P b a D1 D2 O Q (a) Constant industry costs Various long-run industry supply curves under perfect competition S1 P S2 b a c D1 D2 O Q (a) Constant industry costs Various long-run industry supply curves under perfect competition S1 P S2 b a c D1 Long-run S D2 O Q (a) Constant industry costs What if there are external economies to scale in the Long Run? 1. Demand moves out P MC S £ D = AR = MR Pe Pe D O D1 O Q (millions) (a) Industry AC Qe q (thousands) (b) Firm What if there are external economies to scale in the Long Run? 2. Firm moves up MC curve. S1 = nq1 P MC S D = AR = MR Pe Pe D O £ Q0 Q (millions) (a) Industry D1 O AC q0 q1 q (thousands) (b) Firm What if there are external economies to scale in the Long Run? P 3. Supernormal Profits – So firms join the industry MC S D = AR = MR Pe Pe D O £ Q0 Q (millions) (a) Industry D1 O AC q0 q1 q (thousands) (b) Firm 4. But with External Economies of scale as S curve moves out, P AC curve starts to move down MC S S £ 1 D O D = AR = MR Pe Pe Q0 Q (millions) (a) Industry D1 O AC q0 q (thousands) (b) Firm 4. So with External Economies of scale, P Find new equilibrium with lower AC, higher supply and lower price MC S £ AC S1 Pe Pe D O D = AR = MR Q0 Q (millions) (a) Industry D1 O q0 q (thousands) (b) Firm So if there are external economies to scale in the Long Run? P MC S S £ 1 D1 D = AR = MR Pe LRS Pe D O O Q (millions) (a) Industry AC Qe Q (thousands) (b) Firm So if there are external economies to scale in the Long Run? P MC S S £ 1 D1 D = AR = MR Pe LRS Pe D O O Q (millions) (a) Industry AC Qe Q (thousands) (b) Firm Various long-run industry supply curves under perfect competition P S1 b a D1 O D2 Q (c) Decreasing industry costs: external economies of scale Various long-run industry supply curves under perfect competition P S1 S2 b a c D1 O D2 Q (c) Decreasing industry costs: external economies of scale Various long-run industry supply curves under perfect competition P S1 S2 b a c Long-run S D1 O D2 Q (c) Decreasing industry costs: external economies of scale What if there are external Diseconomies to scale in the Long Run? P MC S £ D = AR = MR Pe Pe D O D1 O Q (millions) (a) Industry AC Qe q (thousands) (b) Firm External Diseconomies to Scale I want you to analyse the various effects on the market and the firm when this occurs. Classes on week 6: Hand in Short Essay Structure 1. Motivate: Why might this occur? 2. Anaslyse (both firm and market) 3. Evaluate How many words? Inframarginal Producers • In some industries such as agriculture, new entrants may have higher costs than existing producers (worse land etc.) Classes on week 7: Hand in Short Essay Structure 1. Motivate: Why might this occur in other industries 2. Anaslyse (both firm and market) 3. Evaluate instance and implications How many words? Essay Writing • Length: Approximately 800-1000 words, or about 3 sides of A4 paper, including diagrams (depends on how big your diagrams are). • See p 32 -35 in Economics Handbook for further advice on essay writing. PERFECT COMPETITION • Short-run supply curve of industry • Long-run equilibrium of the firm – all supernormal profits competed away – long-run industry supply curve • Incompatibility of INTERNAL economies of scale with perfect competition PERFECT COMPETITION • Advantages of perfect competition – P = MC – production at minimum AC – only normal profits in long run – responsive to consumer wishes: consumer sovereignty – competition efficiency – no point in advertising PERFECT COMPETITION • (ALLEGED) Disadvantages of perfect competition – insufficient profits for investment – lack of product variety – lack of competition over product design and specification • Not really valid set of criticisms PERFECT COMPETITION • Disadvantages of perfect competition – There are none • Except perhaps…. – Disadvantage is that it may not be a valid version of reality – Recall assumptions firms are price takers OK freedom of entry and exit iffy identical products Few examples perfect knowledge iffy