Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

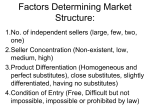

Strategy & Investing Chris Argyrople, CFA Concentric Corporate Strategy & Investing 1 Competitve Strategy What is more important? • • • • • Price Financial Performance (growth) Corporate Strategy Industry Factors Implementation Answer: They are All Important Finance and Strategy must be analyzed together. 2 Industry Analysis (Hooke: Security Analysis on Wall Street) • Serious research starts at industry level • In-depth industry study is prerequisite for a proper security analysis • Chosen industries don’t have to be stellar performers, they just have to be reasonable • Don’t be afraid to have a contrary opinion. If you want different results than others, you must invest in different securities 3 Competitive Strategy: The Core Concepts (Michael Porter) • Competition is the core to success or failure • Two key questions: – Industry Attractiveness – Firm’s Position within Industry • Creating Competitive Advantage: – Create value for buyers that exceed the cost of creating it – Either provide lower prices or more benefit @ same price 4 Structural Analysis of Industries • Industry attractiveness is the fundamental determinant of any firm’s profitability • Goal of Strategy: Change the Rules in Firm’s Favor • Product sexiness does not drive profitability – industry structure does – Many high-tech industries like PC hardware are not profitable for all participants (Compaq, Packard Bell) – Low-tech businesses can be very profitable: 5 Postage Meters Affecting Industry Structure • Most important for firms to alter industry structure in their favor • Not all 5 forces will be equally important for each firm in any industry • Each industry has unique structure • Firms can easily destroy industry structure (as easy as they can improve it) by reducing entry barriers (through new designs), or extended price cutting 6 Reaction by Competition • Whenever firms make a move, they must consider the competitive reactions. If competitors imitate your price cut, everyone could be worse off • “Industry destroyers” are often 2nd tier firms stretching to overcome competitive disadvantages • Leading firms usually dictate structure, but anything they do usually affects all firms 7 Value to Buyer is Source of Value • Satisfying buyer needs is core of success in any business • Happy customers are necessary but not sufficient for profitability • Industry structure determines who captures the value • If buyers have lots of power, they keep the value for themselves – leaving little for the firms (same concept for suppliers) 8 Capturing Value • If an industry’s product creates minimal value – small profits for industry • If value created for buyers, structure is crucial: – Autos – lots of value but small profits – Medical Services – value and higher profits 9 Porter 5 Forces Model Buyers Substitutes Industry Rivalry Potential Entrants Suppliers 10 Competition Industry = Group of firms that produce products which are close substitutes ** Industry factors are often more important than firm specific issues Example: Highly Profitable Pharmaceuticals Software Less Profitable Grocers Retailing 11 6 Major Entry Barriers • SCALE ECONOMIES – Can be present everywhere: Manufacturing, Design, Purchasing, Sales, Service, etc. • PRODUCT Differentation / Technology • CAPITAL • SWITCHING COSTS – Capital PLUS Training • DISTRIBUTION CHANNELS • GOVT. POLICY / REGULATION 12 Advantages Independent of Scale • • • • PROPRIETARY TECHNOLOGY FAVORABLE RAW MATERIAL ACCESS GOOD LOCATIONS GOVT. SUBSIDIES, LICENSES, PATENTS • LEARNING CURVE • FIRST MOVER ADVANTAGE 13 Warning Signs RIVALRY Price competition usually hurts everyone (unless it successfully drives out competition). Beware of price competition. It is usually very bad news for a stock. EXIT BARRIERS - perpetuate Overcapacity Types: Labor, no buyers for assets, govt. restrictions, emotional exit barriers. 14 Buyer Power • Number of Customers. – An industry is powerful when there are many small customers. No customer has significant impact. • Uniqueness of Product. – If no substitute readily exists, then an industry has power over customers. • Brand Preferences. – Buyers who prefer a certain brand (cigarettes, 15 for example) have lower power. Buyer Power • Size of Purchase. – If cash outlay is low, customers do not have power. For large purchases like automobiles, buyers can exert power because their demand is very price elastic. • Switching Costs. – High switching costs give the industry strength. • Significance of Product Quality. – If industry’s quality is not important (to the quality 16 of the buyer’s product), the customer will minimize Buyer Power • Threat of Vertical Integration. – If a buyer has a credible threat of vertical integration, he exerts more power. • Information Available to Buyers. – Lack of information about capacity, markups, etc. put buyers at a disadvantage. • Low Profits 17 Supplier Power • Product Substitutes. – Industry has power over vendors if substitutes to the supplier’s product exist. • Number of Suppliers. – A large number of suppliers can’t exert influence. • Entry Barriers in the Supplier’s business. – If the entry barriers are low, companies can squeeze out suppliers through vertical integration. • Ability to Delay Purchase of Vendor’s Product. 18 Supplier Power • Existence of Unions. – A unionized industry may discourage new entrants, thus giving existing suppliers power. • Industry Capacity Relative to Demand. – Excess capacity in a supplier’s product line diminishes vendor strength • Product Differentiation or Brand Loyalty. – Undifferentiated products with low brand allegiance can’t exert power. 19 Supplier Power • Importance of Supplier’s Product to Industry’s Product. – If the supplier’s product is unimportant to industry quality, then suppliers have less power. • Industry small % of Supplier’s Sales – Sometimes a product is too small to waste time on • Supplier’s Ability to Forward Integrate into Industry’s Business 20 Product Substitutes • Existence of Substitutes. – How close are substitutes to your company’s products? • Price / Quality advantage of Substitutes. • Advent of New Technologies. – Usually the biggest risk – often can blindside a slow-moving, large beauracracy. • Switching Costs. – Often a product is designed as a system input. Switching requires product redesign and Re- 21 Industry Rivalry • Industry Growth Rate is the fundamental determinant of an industry’s competitiveness. – Growth: firms expand without price competition. • Industry Cost Structure. – High fixed costs provide incentives to fill incremental excess capacity at below market prices. This is bad. • Scale Economies. 22 Industry Rivalry • Exit Barriers. (can increase competitiveness) Examples: – Government restrictions – Emotional attachment (management, entrepreneur) – Unique Assets. Difficult to sell. – Costs to close plant & layoff employees. • Brand Loyalty and Product Differentiation. • Switching Costs. 23 • Number of Competitors. Industry Rivalry • AMOUNT OF PRICE COMPETITION. • BEWARE OF PRICE COMPETITION. • Strategic Importance. If the business is of strategic importance to competitors, then rivalry will be strong. Conversely, if some competitors have vertically integrated into the business, they will not be as fierce. 24 Types of Generic Strategies 1) COST LEADERSHIP 2) DIFFERENTIATION 3) FOCUS (Niche) Cost or Differentiation Focus Stuck in the Middle Guaranteed Low Profitability Firms that Switch Strategies too Often 25 Generic Strategies: Low Cost, Differentiation, Focus Lower Cost Differentiation Broad Target Cost Leadership Differentiation Narrow Target Cost Focus Differentiation Focus 26 Cost Leadership • There can only be one – don’t want to be one of several firms vying for the spot. • Must convince others to abandon this strategy, depends on preemption • Low cost producer guaranteed a good position – at equivalent prices, the low cost producer has higher margins • Sources of advantage: scale economies, low-cost designs, proprietary technology, better access to raw materials etc. 27 Differentiation • Be unique on some dimension that is valued by buyers • Get Premium Pricing for differentiation • Differentiation can be based on product, delivery system, marketing approach etc. • Price Premium must exceed added cost of differentiation to add value 28 Focus: Cost & Differentiation Focus • Focuser selects a target segment (or niche) and tries to get competitive advantage in the segment (even though no overall advantage) • Exploit cost advantage in certain segments • Differentiation focus = exploit buyers’ special needs in those segments • Narrow focus is not sufficient for good performance 29 Example of Focus • Craft beer like Sam Adams – differentiation focus • Low cost – Royal Crown cola 30 Stuck in the Middle • Stuck in the Middle – try to be everything to everybody • Firms often try to get competitive advantage through all strategies and achieves none • Firm stuck in the middle can still be profitable if other competitors are stuck or if the industry itself is highly profitable 31 3 Conditions for being both Cost Leader & Differentiation • Can simultaneously achieve both cost leadership & differentiation if: 1. Competitors are stuck in the middle 2. Cost is affected by share or interrelationships 3. Firm pioneers a major innovation 32 Risks of Cost Leadership • • • • Competitors Imitate Technology Changes Other bases for cost leadership erode Cost focusers achieve even lower costs in target segments • Proximity in differentiation is lost 33 Risks of Differentiation • Competitors Imitate • Bases for differentiation become less important to buyers • Differentiation focusers achieve greater differentiation in target segments • Cost proximity is lost 34 Risks of Focus • Target Segment becomes structurally unattractive: – Structure Erodes – Demand Decreases – Segment’s differences narrow (& thus broad competitors enter space) – Advantages of a broad line increase – New Focusers in sub-segment industry 35 Other Points • Build / Hold / Harvest – this is not strategy, these are results of strategy • Acquisitions are not strategy – they are a means of achieving a strategy • Market share does not describe competitive position. Share is not a cause of competitive advantage but a result of it. 36 Product Life Cycle SALES Intro or Startup Growth Maturity Decline Transition Phase TIME 37 Changes in Growth • DEMOGRAPHICS • TRENDS (Social) • CHANGES IN SUBSTITUTES (Cost & Qual) • CHANGES IN COMPLEMENTS • PENETRATION • TECHNOLOGY / PRODUCT CHANGE 38 Model Industry Analysis • Industry Classification – Life Cycle Position, Business Cycle • External Factors – Technology, Govt., Social, Demographic, Foreign • Demand Analysis – End Users, Growth, Trends & Cyclicality around trends • Supply Analysis – Concentration, Ease of Entry, Industry Capacity • Profitability – Supply/Demand Analysis, Cost Factors, Pricing • International Competition & Markets 39 Business Cycle • Three Types of Industries: – GROWTH, DEFENSIVE, CYCLICAL • Growth Industry: above average growth independent of the business cycle • Defensive Industry: Stable (mostly upward: slight dip in downturns) performance throughout business cycle (food, utilities etc.) • Cyclical Industry: Earnings track the business cycle 40 Issues in Industry Classification • Self-deception is a key problem: once an industry is classified as a “growth” industry, analysts often miss its move out of the category • Don’t paint all industry participants with the same brush – not all firms in mature industry are mature 41 External Factors Technology: What is obsolescence risk? Government: Policy can create industries (i.e. auto airbags) Social Changes: Lifestyle can affect industries (trend toward fast food etc.) Demographics: “Greying” of America (healthcare, golf industry) Foreign Influences: Foreign steel & auto are good examples 42 Demand Analysis • Top-Down Analysis: Look for correlation between economy & sales (example: cement industry correlated to GNP ) • Industry Life Cycle: Where is the industry within its life cycle? • External Factors: Qualitative Analysis Establish a sales forecast, often by extrapolating trends (look for turning points) 43 Other Issues: Demand Analysis • Customer study is key – study buying habits • Geographical differences • Growth Industries – measure penetration • Untested Industries – does product fill a need? 44 Supply Analysis • Supply is a function of excess capacity • Add up capacity of all firms • Pricing is linked to capacity: overcapacity indicates lower prices 45 Industry Pricing • Factors Influencing Pricing: – Product Segmentation – Industry Concentration – Ease of Entry – Price changes of Supply Inputs 46 Strategy & Investing • Long Term Perspective • Augments “The Numbers” • Analyze – INDUSTRY – FIRM’S COMPETITIVE ADVANTAGE • Pay Attention to: – Cash Flow, Cyclicality – Growth Rate & Changes in Growth Rates – Capacity / Substitutes / Change in Comp. Position 47 Strategy & Investing • Great Long Term Investments have Sustainable Competitive Advantage • Like to Pay a Reasonable Price for firms with a Moat around them • Growth at a Reasonable Price = GARP • Pay attention to Industry as much as firm • Who has the best strategy today? – Microsoft? - GE? Thoughts ??? - Gillette? 48 Determining Sustainability of Competitive Advantage DC Mueller, in Profits in the Long Run, found that there is incomplete regression to the mean. Why? Incomplete Regression to the Mean High Return Firm ROA Low Return Firm Time 49 Why Might Excess Profits Persist? • Maybe the high-profit groups are riskier (thus the markets require higher returns) • Some advantages are subtle to detect, especially in a world where the same resources are available to all firms. • Why might resources be immobile? – Culture, Brand Image, Location, Relationships, Patents, Scale Economies, Customer Access, etc. 50 Example of Sustainability: QWERTY Keyboard • Sometimes the answer is VERY SIMPLE • QWERTY is a sub-optimal keyboard configuration invented in 1873 • QWERTY invented to minimize typebar clashes (we don’t have typebars anymore) • All world records for typing have been set on the Dvorak keyboard, invented in 1932 • Apple IIC computers came with a keyboard that switched between QWERTY & Dvorak • TOUGH TO GET PEOPLE TO CHANGE !!! 51 Reputation & Buyer Uncertainty • People generally go back to the same place to buy their gasoline etc. • Habits are tough to break • Once you are satisfied with a product, it is difficult to get people to switch !! • Why do people still buy Intel processors when AMD might be faster & cheaper? 52 Why Early Movers Fail • Royal Crown invented diet cola • Lotus 123, D-Base all lost 90% share • These firms may not have the Complimentary Assets necessary for product leadership • Early movers often fail to innovate & next generation products are superior 53 Management is the Key Variable • Good Companies are run by Good Management Teams • Goodwill can be destroyed. This means that, Long Term, people are a company’s main assets. Example: – 1960s, General Motors, PanAm, IBM, AT&T were like Microsoft, Gillette, Coke, and GE today. – Lousy Management ruined GM, it could ruin Coke too! 54 Evaluating Management Characteristics of Good Management: • Ownership interests aligned with shareholders (i.e. they own lots of shares) • No empire building. Acts in best interests of stockholders. Examples: – Increased Dividends, Stock Buybacks etc. • Good information systems • People Focus • TRACK RECORD 55 Checklist for Management Evaluation • • • • • How have they done in the past? Are they buying or selling shares? Have you listened to the conference call? Is Mgt. more or less cautious vs. normal? Do their actions support shareholder value or empire building? • Too many options grants to themselves? • Any recent Changes to the Mgt. Team? 56