Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

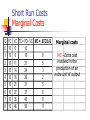

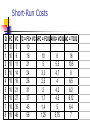

Producer Decision Making Frederick University 2013 Producer Decision Making The firm Profit = total revenues – total cost Production Inputs Labor Land Capital Process Product or service generated – value added Output Production Function The relationship between inputs and outputs is stated by the PRODUCTION FUNCTION Inputs – the factors of production classified as: Land – all natural resources of the earth Labour – all physical and mental human effort involved in production Price paid to acquire land = Rent Price paid to labour = Wages and salaries Capital – buildings, machinery and equipment not used for its own sake but for the contribution it makes to production Price paid for capital = Interest Production Function Mathematical representation of the relationship: Q = f (L,N,K) Output (Q) is dependent upon the amount of capital (K), Land (N) and Labour (L) used Economic and Accounting Costs Costs vs. expenditures Opportunity cost Explicit and implicit cost Sunk cost Depreciation Economic cost vs. Accounting cost – an example One year ago, Tom and Jerry set up a vinegar bottling firm (called TJVB). Tom and Jerry put €50,000 of their own money into the firm. (They used this money to pay for equipment, labor, etc.) They rented equipment for € 30,000; They hired one employee to help them for an annual wage of € 20,000; Tom gave up his previous job, at which he earned € 30,000, and spent all his time working for TJVB; Jerry kept his old job, which paid € 30 an hour, but gave up 10 hours of leisure each week (for 50 weeks) to work for TJVB; The prevailing interest rate was 10% The cash cost of TJVB (for raw materials and like) were € 10,000 for the year. Economic cost vs. Accounting cost – an example Explicit costs 30000+20000+10000 = 60000 Implicit costs 30000+10x50x30+10%x50000 =30000+15000+5000 = 50000 Accounting costs 60000 = explicit cost Economic costs 60000+50000=110000 Implicit cost +explicit cost Economic and Accounting Profit Accounting profit = TR – accounting cost Economic profit = TR – economic cost Normal profit = implicit cost = the profit that might be earned elsewhere Technological choice Technology – a way of putting resources together Efficient technology vs. inefficient technology Technological choice and consumer choice Consumer choice MUa/Pa = MUb/Pb The firm as a consumer: MUL/PL = MUK/Pk Technological choice MPL/PL = MPK/Pk Analysis of the production function Short run Short run There is at least one fixed factor Firm’s decisions are constrained by the fixed factor If the demand changes, the firm can respond only by changing the quantity of output, not the scale of production short run The Law of Diminishing Returns total, average and marginal product L 0 1 2 3 4 5 6 7 8 TPL 0 15 32 57 80 95 108 119 128 short run The Law of Diminishing Returns total, average and marginal product L 0 1 2 3 4 5 6 7 TPL 0 15 32 57 80 95 108 119 MPL APL 15 17 25 23 15 13 11 15 16 19 20 19 18 17 Analysis of the Production Function long run Long run All factors are variable The firm can change its production capacity – the scale of production Short-Run vs. Long-Run Costs Short run – Diminishing marginal returns results from adding successive quantities of variable factors to a fixed factor Long run – Increases in capacity can lead to increasing, decreasing or constant returns to scale Returns to Scale RS = % change in the output : % change in production factors Economies of Scale RS > 1 Constant Returns to Scale RS = 1 Diseconomies of Scale RS < 1 Short Run Costs In buying factor inputs, the firm will incur costs Short run costs are classified as: Fixed costs Variable costs Short-Run Costs Q 0 1 2 3 4 5 6 7 8 FC VC TC = FC+ VC 10 0 10 10 6 16 10 11 21 10 14 24 10 16 26 10 21 31 10 27 37 10 35 45 10 46 56 Short run – there is at least one fixed factor Fixed cost – does not vary with the output Variable cost – directly related to variations in output The Law of diminishing marginal returns Short-Run Costs Total Cost - the sum of all costs incurred in production TC = FC + VC Average Cost – the cost per unit of output AC = TC/Output Marginal Cost – the cost of one more or one fewer units of production MC = TCn – TCn-1 units Short Run Costs Marginal Costs Q 0 1 2 3 4 5 6 7 8 FC 10 10 10 10 10 10 10 10 10 VC TC = FC+ VC MC = 0 10 6 16 11 21 14 24 16 26 21 31 27 37 35 45 46 56 ΔTC/Δ Q 6 5 3 2 5 6 8 11 Marginal costs МС –Extra cost involved in the production of an extra unit of output Short-Run Costs Q 0 1 2 3 4 5 6 7 8 FC 10 10 10 10 10 10 10 10 10 VC TC = FC+ VC AFC = FC/Q AVC= VC/Q AC = TC/Q MC = TC/ΔQ 0 10 6 16 10 6 16 6 11 21 5 5,5 10,5 5 14 24 3,3 4,7 8 3 16 26 2,5 4 6,5 2 21 31 2 4,2 6,2 5 27 37 1,7 4,5 6,12 6 35 45 1,4 5 6,4 8 46 56 1,25 5,75 7 11 Short-Run Costs Q 0 1 2 3 4 5 6 7 8 FC 10 10 10 10 10 10 10 10 10 VC TC = FC+ VC AFC = FC/QAVC= VC/Q AC = TC/Q 0 10 6 16 10 6 16 11 21 5 5,5 10,5 14 24 3,3 4,7 8 16 26 2,5 4 6,5 21 31 2 4,2 6,2 27 37 1,7 4,5 6,12 35 45 1,4 5 6,4 46 56 1,25 5,75 7 The Revenues of the Firm Total Revenue TR = P x Q Average Revenue AR = P Marginal Revenue MR = Δ TR/Δ Q Profit Profit = TR – TC The reward for enterprise Profits help in the process of directing resources to alternative uses in free markets Relating price to costs helps a firm to assess profitability in production Profit Normal Profit – the profit that might be earned elsewhere (the minimum amount required to keep a firm in its current line of production) Economic (Abnormal or Supernormal) profit – profit made over and above normal profit The Profit of the Firm Short Run Long Run Maximum Profit Maximum Profit MC = MR P > AC Minimum Loss MC = MR P > AVC MC = MR P > AC