Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

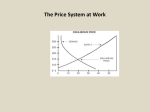

Economia Dominika Ostrowska My topics: 1. Marginal Revenue 2. Surplus 3. Shortage Marginal Revenue If people will buy 100 units of a product when its price is $10.00, as the picture below illustrates, total revenue for sellers will be $1000. The height is price and the width is quantity, and since price multiplied by quantity is total revenue, this shown area is total revenue. Marginal revenue is the increase in revenue that results from the sale of one additional unit of output. Marginal revenue is calculated by dividing the change in total revenue by the change in output quantity. While marginal revenue can remain constant over a certain level of output, it follows the law of diminishing returns and will eventually slow down, as the output level increases. Marginal revenues and costs can be further broken down into long run and short run. This reflects times over which decisions can be made. A decision to increase output a little can be made over the short term, but a larger increase may require purchasing equipment, building a new factory etc, which takes longer. Economic surplus Two related quantities: consumer surplus and producer surplus. Consumes surplus or consumers' surplus is the monetary gain obtained by consumers because they are able to purchase a product for a price that is less than the highest price that they would be willing to pay. Producer surplus or producers' surplus is the amount that producers benefit by selling at a market price that is higher than the least that they would be willing to sell for. On a standard supply and demand diagram, consumer surplus is the area (triangular if the supply and demand curves are linear) above the equilibrium price of the good and below the demand curve. This reflects the fact that consumers would have been willing to buy a single unit of the good at a price higher than the equilibrium price, a second unit at a price below that but still above the equilibrium price, etc., yet they in fact pay just the equilibrium price for each unit they buy. Shortage A shortage is a situation where there is an excess at some price of quantity demanded over quantity supplied. On a supply and demand curve a shortage is represented by points below the equilibrium price. When a shortage exists buyers are competing with one another for limited quantities of goods. For sellers, it is an opportunity to raise prices and increase sales. Buyers, on the other hand, become frustrated because they are willing to spend money, but cannot find a particular good or service to purchase. A shortage emerges at any price below the equilibrium price of 50 cents. A prime candidate to generate a shortage is a price of 30 cents. Quantity Supplied: At 30 cents, the quantity supplied is only 200 tapes. Because the price is relatively low, sellers are guided by the law of supply and are not willing and able to offer much of the good for sale. Thank you