Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

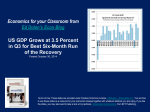

Economics for your Classroom from Ed Dolan’s Econ Blog Quantitative Easing: A Tutorial Revised March 2013 Terms of Use: These slides are provided under Creative Commons License Attribution—Share Alike 3.0 . You are free to use these slides as a resource for your economics classes together with whatever textbook you are using. If you like the slides, you may also want to take a look at my textbook, Introduction to Economics, from BVT Publishing. Behind the Mystery of Quantitative Easing Central banks—the Federal Reserve, the European Central Bank, the People’s Bank of China, and others—are among the most powerful institutions in the world One of their potentially most powerful but most mysterious instruments is Quantitative Easing or QE This tutorial attempts to explain the mechanics of QE and its effects to date on the US economy Federal Reserve Building, Washington, DC Photo by Agnosticpreacherskid, http://upload.wikimedia.org/wikipedia/commons/8/8d/Marriner_S._Eccle s_Federal_Reserve_Board_Building.jpg Revised version March 2013 Ed Dolan’s Econ Blog The Central Bank Balance Sheet: Assets Fig 1 gives a stylized balance sheet of a typical central bank Net domestic assets consist of all assets denominated in the country’s own currency, e.g., bonds issued by its government, adjusted by subtracting certain liabilities and capital Net foreign assets consist of all assets denominated in foreign currencies, e.g., bonds issued by foreign governments, adjusted by subtracting foreign liabilities, if any Revised version March 2013 Ed Dolan’s Econ Blog The Central Bank Balance Sheet: Liabilities The sum of the items on the liabilities side of the balance sheet are called the monetary base, which consists of two parts Reserve deposits that private commercial banks hold with the central bank Currency (paper money and coins) Revised version March 2013 Ed Dolan’s Econ Blog The Central Bank and Commercial Banks The central bank balance sheet is linked to those of commercial banks through reserves of liquid assets held by commercial banks: Reserves of currency used to fill ATM machines and serve other needs Reserve deposits in accounts that commercial banks maintain with the central bank Loans to consumers and firms are banks’ main income-earning assets Bank deposits held by consumers and business firms are banks largest category of liabilities Revised version March 2013 Ed Dolan’s Econ Blog The Complete Financial System We complete our stylized picture of the financial system by adding the balance sheet of the “nonfinancial public,” consisting of all private firms except commercial banks and all households The public balance sheet is linked to the central bank via currency—an asset of the public and a liability of the central bank Bank deposits are an asset of the public and a liability of commercial banks Loans—an asset of commercial banks and a liability of the public—are the last important link among the balance sheets Revised version March 2013 Ed Dolan’s Econ Blog The Money Stock and the Equation of Exchange The nation’s money stock or money supply consists of the total value of currency and bank deposits held by the public. (Currency held by banks is not included) In practice, bank deposits form 80 to 90 percent of the money stock in the monetary systems of developed countries, and currency plays a minor role Revised version March 2013 Ed Dolan’s Econ Blog Central Bank Open Market Operations Open market operations are one of the most important tools that central banks use to control the money stock These are purchases or sales of assets (usually government securities) from or to the public via open secondary markets—hence the name “open market” operations. Note: This and subsequent slides use “Taccounts,” which are simplified balance sheets that only show items that change as a result of whatever operation we are discussing Revised version March 2013 Ed Dolan’s Econ Blog Open Market Operations Step-by-Step Step1: The central bank adds to its holdings of domestic securities by buying them from security dealers or other members of the public Step 2: The central bank pays for the securities using a payment order that is executed through the banking system. Sellers of the securities receive payment as deposits added to their bank accounts Step 3: To complete the payment process, the central bank adds an equal amount to the reserve deposit of the commercial bank or banks where the sellers keep their accounts Revised version March 2013 Ed Dolan’s Econ Blog Further effects of open market operations The first three steps in the open market operation result in an increase in bank reserves and a equal increase in the money stock, in the form of bank deposits To complete the story, banks may use the added reserves as a basis for making new loans. If they do, the proceeds of the loans are paid out to the borrowers in the form of added bank deposits. The result is a further multiple expansion of the money supply beyond the immediate impact of the open market operation Revised version March 2013 Ed Dolan’s Econ Blog What is Quantitative Easing? In normal times, an increase in bank reserves pushes down market interest rates and encourages investment, so that even a relatively small open market operation can stimulate the economy However, when interest rates are near zero, as they have been during the crisis, very large purchases of assets may be needed to have any significant effect on the economy. Such very large central bank purchases of assets, including long-term as well as short-term securities, are known as quantitative easing (QE) Revised version March 2013 Ed Dolan’s Econ Blog Giving QE a Try Early in the crisis, the Fed undertook a large scale asset purchase program, now known as QE1, which resulted in a huge increase in the monetary base The money stock increased only slightly, because bank lending did not increase as much as reserves Even though the money stock grew, the velocity of its circulation through the economy fell and nominal GDP continued to decrease. Revised version March 2013 Ed Dolan’s Econ Blog From QE1 to QE2 Because QE1 failed to get the economy back on track, from late 2010 to mid-2011, the Fed carried out an additional large scale purchase of assets that became known as QE2 Although there is some evidence that QE2 lowered long-term interest rates, the recovery remained slow Revised version March 2013 Ed Dolan’s Econ Blog Now QE3 In September 2012 the Fed decided to begin a new round of easing, QE3 QE3 will buy $40 billion per month of mortgage-backed securities, and will continue some other bond-buying programs Unlike QE1 and QE2, QE3 has no specified end date. It will continue until the economy improves by enough to justify ending it Revised version March 2013 Ed Dolan’s Econ Blog Recycling Interest Payments When the Fed buys securities, interest it collects is a source of income for the Fed, but the Fed is not allowed to profit from it. After deducting its operating costs, it turns any surplus back to the Treasury. Does that mean that QE has no cost, so that there is, after all, such a thing as a free lunch? In the short run, yes, but there are two important qualifications The Fed The Treasury Treasury photo by David Monack, http://commons.wikimedia.org/wiki/File:GallatinTreas.jpg Revised version March 2013 Ed Dolan’s Econ Blog Qualifications to the Free Lunch Theory of QE Qualification No 1: Since 2008, the Fed has begun paying interest on banks’ reserve deposits, so not all the interest is recycled. The “free lunch” is at best a lunch at a discount price Qualification No. 2: The Fed will not be able to hold its big QE purchases of bonds forever. Sooner or later, the economy will begin to recover. The Fed’s exit strategy from QE will require selling off most of the extra securities to prevent excess money growth and the risk of inflation. Under some conditions, it might have to sell them at a loss Photo: © BrokenSphere / Wikimedia Commons Revised version March 2013 Ed Dolan’s Econ Blog Has Quantitative Easing Worked? Fed Chairman Ben Bernanke has cited estimates that QE1 and QE2 together lowered long-term interest rates by 0.8 to 1.2 percentage points The estimates suggest that output is 3 percent higher than it otherwise would be and about 2 million jobs were created Some independent observers think the impact has been smaller than the Fed’s estimates Fed Chairman Ben Bernanke Source: Fed official portrait via Wikimedia Commons Revised version March 2013 Ed Dolan’s Econ Blog How Does QE Work? Standard theory says that in normal times monetary policy works by lowering interest rates, so how can QE work when short-term interest rates are already zero? One theory says that it works by changing the relative amounts of long- and short-term securities, thereby lowering long-term rates Another theory says the most important effect is forward guidance, that is, changing people’s expectations about what the Fed will do in the future For a detailed discussion of how QE works, see this paper by Michael Woodford presented at the Fed’s 2012 conference in Jackson Hole, WY Jackson Hole, Wyoming Source: Enricokamasa via http://commons.wikimedia.org/wiki/File:Corbet%27s_Couloir_jackson_h ole.jpg Revised version March 2013 Ed Dolan’s Econ Blog Will QE Save the US Economy? There is substantial evidence that QE has made the economy somewhat better off than it would otherwise have been However, we also need responsible fiscal policy. In Fed Chairman Bernanke’s words It is critical that fiscal policymakers put in place a credible plan that sets the federal budget on a sustainable trajectory in the medium and longer runs. Monetary policy cannot achieve by itself what a broader and more balanced set of economic policies might achieve. Source of quotes: Speech of Aug 31,2012 Revised version March 2013 Ed Dolan’s Econ Blog For more slideshows and commentary, follow Ed Dolan’s Econ Blog Share Follow Click on the image to learn more about Ed Dolan’s Economics textbooks