Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

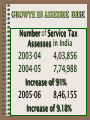

INTRODUCTION OF SERVICE TAX & ITS NEED IN THE ALL-ROUND DEVELOPING ECONOMY SERVICE TAX ? It is an Indirect Tax on service industry. Service is a performance of any duties or work for another. Levied upon specified services and not on tangible objects. Levied upon specified persons on service provided to specified consumers. SERVICE TAX ? Tax is levied on service and not on Manufacturing,Profession, Income, Profit or Sale of Goods. Service Tax is thus carrying the tax to the point of consumption i.e. the last point. Need For Taxing Services For moving towards fullfledged ‘VAT’. To include service sector into the stream of central taxation. For broadening tax base. For collection of more revenue Dr. Manmohan singh introduced service tax in 1994 Service tax introduced in 1994 Increase In Taxable Categories of Services 100 Categories of Taxable Services 100 90 100 80 71 80 63 70 53 60 50 42 40 27 30 27 18 20 10 93 3 3 6 0 1994 1996 1998 2001 2003 Categories of services 2005 2007 Sectoral structure of world economies Percentage of GDP High Income Countries Service 66% 32% 2% Middle Income Countries Low Income Countries Agriculture SERVICE SECTOR in INDIA at 55% Service 52% 35% 11% Service 35% 38% 25% Industry Services Change in contribution Sectors Of Economy PRAPORTION OF DIFFERENT SECTORS OF ECONOMY AGRICULTURE 18.5% of GDP SERVICE 55.1% of GDP SERPASSING OTHER SECTORS - 68.6% Growth INDUSTRY 26.4% of GDP PER CAPITA INCOME OVER TIME Share of services in GDP Finance Minister Speaks “………….Growth will be sustenance by increased production and value added in agriculture, a marked amount in industrial production and continued buoyancy in the performance of service sector”. He further added that he would like to align Indian Tariff strongly to those of ASEAN Countries and would also desire to have a uniform rate of tax on goods and services. REVENUE GROWTH 40000 38169 Rs. (in crores) 35000 30000 23055 25000 20000 14150 15000 8300 10000 5000 411 846 1022 976 1788 2072 2612 3305 4125 0 199495 199697 service tax 199899 200001 Years 200203 200405 200607 GROWTH IN ASSESSEE BASE Number of Service Tax Assesses in India 2003-04 2004-05 4,03,856 7,74,988 Increase of 91% 2005-06 8,46,155 Increase of 9.18% Salient Features Of Service Tax Extend to whole of India except J&K.. Service provider is normally responsible for payment of tax. In specified situations the person receiving the service is liable to pay service tax. Service Tax can be charged on specified taxable services. Service Tax is levied @ 12% of value of service charged with 2% Educational Cess & 1% Secondary Higher Education Cess. Service Tax credit is allowed across goods and services. Salient Features Of Service Tax Service provider is responsible for payment of tax. Service Tax liability created when charged but has to be paid only when payment is received. Threshold exemption from 1.4.2007 exempting from service tax, the aggregate value of taxable services not exceeding eight lakh rupees received by the service provider during a financial year. Salient Features Of Service Tax Export of services without payment of service tax has been made with effect from 15.3.2005. Import of services brought into the tax net. Administered by the Central Excise Commissionerates working under the Central Board of Excise & Customs through the process of self-assessment, revision, appeals, penalties, etc. Powers given to Government to grant exemption and rebates in appropriate cases. Definition Of Words ‘Service Provider’ and ‘Categories of Services’ as defined can only be taxed. Understanding the definition of specified words is important for interpretation. 100 Categories of services are presently taxable out of 107 specified categories of service on 74 types of person liable to pay and 8 broad types of person to receive the service. Mission of Ministry of Finance Realizing the revenues in a fair, equitable and efficient manner Administering the Government's economic, tariff and trade policies with a practical and pragmatic approach. Facilitating trade and industry by streamlining and simplifying Customs, Excise and Service Tax Processes and helping Indian business to enhance its competitiveness. Creating a climate for voluntary compliance by providing guidance and building mutual trust. Combating revenue evasion, commercial frauds and social menace in an effective manner. CONCLUSION SERVICE TAX ADMINISTRATION Requires revamping and separate comprehensive legislation. Distinct Administrative Machinery Aimed to bring in greater clarity, streamlined-procedures, greater taxpayer assistance & new tax culture of voluntary compliance Information on WEB SITE Web Sites loaded with information provided by the Government to guide assesses in service tax matters: www.finmin.nic.in www.cbec.gov.in www.excise.gov.in www.exciseandcustoms.gov.in www.exciseandservicetax.nic.in I sincerely acknowledge the guidance and feed back received from my brother colleagues specially Mr. Naveen Garg, Chartered Accountant and Mr. Arvind Sharma, Advocate. I express my sincere thanks to my office staff in assisting me for preparation of this presentation. R-13/24, RAJ NAGAR, OPP. A.L.T.C., GHAZIABAD PH: 0120-2820380, 2821407