Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Ragnar Nurkse's balanced growth theory wikipedia , lookup

Business cycle wikipedia , lookup

Transition economy wikipedia , lookup

Economic planning wikipedia , lookup

Production for use wikipedia , lookup

Criticisms of socialism wikipedia , lookup

Rostow's stages of growth wikipedia , lookup

Steady-state economy wikipedia , lookup

Economics of fascism wikipedia , lookup

Protectionism wikipedia , lookup

Non-monetary economy wikipedia , lookup

Economic calculation problem wikipedia , lookup

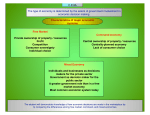

Next >> A nation’s economic system greatly affects its trade relationships. 2 To identify different types of economic systems To explain how natural, human, and capital resources affect a nation’s ability to trade 3 To explain the stages of economic development and their effects on trade To differentiate between an absolute and a comparative advantage 4 You must understand a nation’s economic system in order to effectively conduct business there. 5 Economic Systems and International Trade Understanding economics will help you understand economic systems and international trade. economics the study of how a society chooses to use resources to produce and distribute goods and services for people’s consumption 6 Economic Systems and International Trade There is a strong link between a country’s form of government and its type of economic system. Economic systems influence the use of resources and impact a country’s ability to compete in international trade. 7 Types of Economic Systems Market Economies Mixed Economies Types of Economic Systems Command Economies 8 Market Economies The United States has a market economy. The ideas of capitalism, or the free enterprise system, are associated with a market economy. market economy an economic system in which economic decisions are made in the marketplace 9 Market Economies One force that drives purchases by consumers and businesses is supply. supply the amount of goods and services that producers provide at various prices 10 Market Economies The other force that drives purchases is demand. The meeting place between supply and demand is the equilibrium price. demand the amount or quantity of goods and services that consumers are willing to buy at various prices 11 Market Economies 12 Market Economies Profit is the driving force of the market economy. There are different forms of profit: – Personal – Company – Governmental 13 Market Economies Two other forces drive market economies : Private property rights Relatively free and competitive marketplaces 14 Market Economies In any market, there are some goods that require governmental regulation, such as dangerous chemicals. 15 Command Economies A command economy is also known as a planned economy. The government, or a national leader, decides what will be produced, how, and for whom. command economy an economic system in which a central authority makes all key economic decisions 16 Command Economies Two Types of Command Economies Strong Command Economy Moderate Command Economy There is heavy government control. State owns major resources. Government owns much of the land, and private property rights are limited. State may control minerals and ores, airlines, and other enterprise. The goal is full employment. The goal is full employment. These countries are often communist states. These countries are often socialist states. Cuba is an example. France and Sweden are examples. 17 Mixed Economies Most countries have a mixed economy. Some argue that socialism is a mixed economy. mixed economy an economic system in which the marketplace determines some economic decisions, and the government makes some decisions 18 Mixed Economies Characteristics of Mixed Economies The government oversees defense, education, building and repairing roads, fire protection, and other general services. Everything else is bought and sold in the marketplace. Either the government or the marketplace tends to dominates. 19 Economic Resources Natural Resources Human Resources Economic Growth Capital Resources 20 Natural Resources Natural resources are raw materials found in nature that are located on the ground and in the water. Nations rich with resources are able to export raw materials and manufactured goods made from those materials. 21 Natural Resources Countries with few natural resources must import key resources, which makes everyday goods more expensive. 22 Natural Resources Two Types of Natural Resources Renewable (can be replaced) Nonrenewable (will not grow back) Agricultural products Iron ore Trees Coal Fish Oil Seaweed Diamonds Water Gold and other minerals 23 Human Resources Human resources are: Workers Managers Contractors The term human resources is distinct from the term population. Other employees 24 Human Resources Skilled Labor There is a strong connection between a country’s literacy level and the number of skilled workers in a population. Unskilled Labor Unskilled labor refers to laborers who have less education and fewer skills that require training. Physical Labor Jobs that require physical labor require unskilled and semi-skilled workers to perform tasks. Mental Labor Mental labor jobs require special knowledge, negotiation skills, and creativity. Wages in these jobs are often higher. 25 Capital Resources Capital is the term for money, or funding, that helps a company buy items needed to start up and maintain a business. Capital comes from investors and the sale of stock to outside investors. 26 Capital Resources When a country has a high level of national debt and a large deficit, it is more difficult to obtain capital. A lack of capital can restrict the development of new businesses and economic growth. 27 Capital Resources Entrepreneurial resources are the funds that help start new companies. Infrastructure refers to all the large-scale public systems and services necessary for economic activity. Good infrastructure provides for economic growth. 28 Economic Decisions Scarcity Factors Affecting Economic Decisions Opportunity Costs 29 Scarcity Scarcity can refer to time, money, natural resources, human resources, or capital resources. scarcity a term used to describe a situation in which there is a limited amount of a commodity Scarcity drives trends in decision-making. 30 Opportunity Costs Opportunity cost is the cost associated with taking one course of action instead of another. Managers and government officials use a method called “cost-benefit analysis” to determine whether the benefits are higher than the cost. 31 Economic Conditions Economists look at several factors to describe the economic well-being of a country. Gross Domestic Product Levels of unemployment Cost of Living Purchasing Power Parity Inflation Rate Balance of Trade Interest Rate Levels Level of Foreign Debt 32 Gross Domestic Product The total value of goods and services produced in a country each year is known as the country’s gross domestic product (GDP). 33 Gross Domestic Product To calculate the GDP, economists add the total value of goods and services sold: To consumers By businesses Increased productivity will cause the GDP to rise. From the government To other countries 34 Cost of Living The cost-of-living index is a measure of how much a typical family must spend to live. A rise in the cost of living means it costs more to live. 35 Inflation Inflation is the increase in currency relative to the availability of goods and services. The Consumer Price Index (CPI) is a measure of a country’s inflation rate. 36 Interest Rates An interest rate is the cost of borrowing money, expressed as an annual percentage. Most economists believe that lower interest rates are better for the majority of people. 37 Unemployment Levels The unemployment rate is a measure of the number of people who are looking for jobs but are unable to find them. The unemployment rate is the difference between the current rate compared to the baseline rate. 38 Purchasing Power Parity Purchasing power parity (PPP) is an estimate of the exchange rate needed to equalize the purchasing power of currencies from different countries. Economic stability exists when PPP is stable and changes very little over time. 39 Balance of Trade A balance of trade is based on the number of imports as compared to the number of exports. A country is better off when the balance of trade is near zero, which means balanced. 40 Level of Foreign Debt When a national government owes money to foreign banks, individuals in other countries, and other national governments, it has a foreign debt. 41 Economic Cycles High employment, strong growth in GDP, positive consumer environment Unemployment is very high Peak Rising Recession Decline Decline toward another recession Companies begin hiring and economic activity increases 42 Stages of Economic Development Four Stages of Economic Development Post-Industrialized Value of total sales of services is greater than the value of physical goods produced Trade with foreign countries, manufacture of physical Industrialized goods dominant, manageable unemployment Small middle class, technological dualism, regional dualism, Developing low savings rates, poor banking facilities High unemployment, few natural and human resources, high Underdeveloped poverty level, dependent on other nations 43 Absolute or Comparative Advantage A country has an absolute advantage when it can produce a good or a service more efficiently than any other country. A comparative advantage is an advantage gained by a product a country makes more efficiently on a personal best level. 44