Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

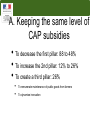

2013 : French position on CAP project ALVES Paulo Mateus FURTADO Caio César LABAQUE German LE BELLEGUY Maxime RAMBAUD Mathis THIBAULT Benoït ERASMUS IP Gödöllo Summer School Introduction I. The CAP in France • Aid distribution • Production cost: France vs Mercosur II. Analysis of CAP impacts • Socioeconomic • Environmental • What we expect about CAP? • Why to reform the CAP? III. Possibles scenarios post 2013 • Keeping the same level of CAP subsidies • Decreasing the level of CAP subsidies IV. Conclusion Introduction General aspects: Total area: 55 millions ha Use land area: 32 millions ha 62 % for crops production 34 % for grassland 2 % of vineyard Agro-food economy 3,5 % of the national GDP 66,8 billion of € 3,4 % of the employment Half of the value come from cereals and wine production Farms structures 348 000 farms Average of 73,3 hectares/ farm 3 people for 100 ha Different productions • Crops • Vegetables • Wine • Livestock •Dairy production •Beef •Pork •Poultry I. The CAP in France A. Aid distribution I Pillar (1000€) II Pillar (1000€) France 8946,9 959,4 Germany 5704 1186,9 Hungary 513,6 537,5 Source: DG Agri EU Budget & Used land French CAP Subsidies Source: Agreste B. Production cost France vs Mercorsur France MERCOSUR WHEAT 1080€/Ha 330€/Ha CORN 1207€/Ha 512€/Ha PORK 1,53€/Kg 1,11€/Kg POULTRY 1,44€/Kg 0,90€/Kg MILK 0,29€/L 0,20€/L Source: Office-Elevage / EMBRAPA / INTA II. Analysis of CAP impacts In which field can the CAP impact on? A. Socioeconomic • • • • • • 15,5 millions (25%) of French live in the countryside 770 000 employs (3,4% of active population) French culture (countryside without farmers is not countryside) Agriculture: 3,5% of GDP 66,8 billions Euros Cereals: • 70,2 million tons Cattle: • • • • bovins: 19,9 millions Pork : 14,8 millions Poultry: 182,9 millions Tourism : Cheese, wine production, cattle, local products SOCIAL / ECONOMICS Strengths Weaknesses 1st agriculture power in Europe Strong agro indstry companies Good agriculture knowledges Good mecanisation of farm Good management skills Developped Agrotourism Development of local products with strong added value Strong agriculture culture in the countryside Rural developement Expensive labor force Strict environmental legislation Expensive land Small average size of exploitations Low R&D investments Increasing of unemployment rate Rural exod Difficulties to innovate Opportunities Threats Increasing of world food demand Increasing of agrofood product prices Increasing competitivness of Eastern European countries Food security Increasing of EU food demand Increasing of EU purchasing power Environment • Cereals: 94460 km2 (51% of arable land) • Cattle in mountains • Rural development: • • • improving the competitiveness of agriculture and forestry; improving the environment and countryside; improving the quality of life in rural areas and encouraging diversification of the rural economy. Environmental Strengths Weaknesses Good environmental legislation Intensive agriculture and environment together? Landscape management Opportunities Threats Environment supported by the EU Increasing of CO2 emmission Aids moving from the I pillar to II pillar Degradation of biodiversity Payment in Ecological services (carbon) C. What we expect about CAP? • Food security (quantity) • Food safety (quality) • Preservation of biodiversity • Landscape maintenance • Food price stabilisation • Profitable agriculture for farmers D. Why to reform the CAP? • Take in account the environmental work of farmers • Reduce market food fluctuation prices • Favorise label and regional products • Favorise the competitiveness of farmers • Good relation between retailers/farmers • Invest more in R&D III. Possibles scenarios post 2013 A. Keeping the same level of CAP subsidies B. Decreasing the level of CAP subsidies A. Keeping the same level of CAP subsidies • To decrease the first pillar: 88 to 48% • To increase the 2nd pillar: 12% to 26% • To create a third pillar: 26% • • To remunerate maintenance of public goods from farmers To dynamise innovation B. Decreasing the level of CAP subsidies Catastrophic scenario 30% 2013 - 2020 104 400 farms 9,6 millions ha 231 000 farmers go to unemployment 4,65 millions of rural exod 20,04 billions € GDP Conclusion • Regarding the 2nd scenario we conclude that the socioeconomics and environmental problems generated by a possible reduction of CAP is too huge for France • A consensus has to be taken in order to keep food safety and food security in Europe against the emergence of third countries like Brazil & Argentina Thank you for your attention !!!