Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

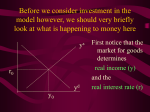

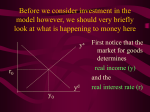

Before we consider investment in the model however, we should very briefly look at what is happening to money here ys r0 yd y0 First notice that the market for goods determines real income (y) and the real interest rate (r) •So the money market determines the nominal variables in the economy: •The price level P, •Inflation p •Nominal interest rate R= r+ p First consider the Demand for Money MD = P L (y, R) L (+,-) That is, the demand for money depends on the level of real income and the NOMINAL interest rate Why Nominal? Because lose R on all money held First consider the Demand for Money P MD = P L (Y, R) e.g Suppose we figure out L(y, R)= 8 then MD = 8P MD M Finding Money Market Equilibrium For simplicity assume for now that there is no inflation, p=0 and thus R=r (that is there is no distinction) Money Demand must equal Money supply M D MS Money Market Equilibrium IF M D MS Then M D P.L( y, r ) MS L( y , r ) P Money Market Equilibrium P MD L( y 0 , r0 ) P0 Money Market Equilibrium MD P0 MbD What happens now if there is a Boom? MD rises as y rises and r goes down L(+,-) So at every P more is demanded Money Market Equilibrium MD P0 MbD P1 So where is the new Equilibrium? So the price level has fallen in a boom as predicted by the stylised facts Money Market Equilibrium MrD P1 MD P0 Similarly in a recession MD falls as y falls and r goes up Md =PL(y ,r ) And the price level rises in a recession Money Market Equilibrium Inflation! P1 MD P0 0 1 What happens if the monetary authority increases the money supply It just causes P to rise! Business Cycle Model with Investment y=f(kt-1,Lt) y y=f(kt-1) y=f(+,+) Note production depends on the capital stock in place at the end of last period kt-1 y=f(kt-1) y Note we are treating L as a constant here y=f(kt-1,Lt) kt-1 MPk t-1 Marginal Product of Capital is decreasing kt-1 y y=f(kt-1) Note we are treating L as a constant here y=f(kt-1,Lt) kt-1 y=f(L) L But we are treating kt-1 as a constant here y=f(kt-1,Lt) y y=f(kt-1) kt-1 y=f(L) L And both functions exhibit diminishing marginal returns More generally could consider changes in K & L and then would expect something more like: 2y y k&L 2k & 2L However, right now we want to focus on the investment decision so we need to focus on capital in isolation y=f(kt-1) y MPk t-1 kt-1 And on the MPkt-1 in particular Why? kt-1 However, right now we want to focus on the investment decision so we need to focus on capital in isolation y=f(kt-1) y kt-1 MPk t-1 kt-1 Because the MPkt-1 tells us the additional output we get from one more unit of Capital MPk t-1 What other consideration do we need to think about with capital? Depreciation! kt-1 MPk t-1 So true return from capital is MPkt-1 less depreciation, d. What is its cost? The real rate of interest r MPk t-1-d kt-1 MPk t-1 So we should equate the real return on capital, MPkt-1-d, with the real rate of interest r r MPk t-1-d kt-1 k̂ * t 1 k̂ MPk t-1 * t 1 Is the desired capital stock r MPk t-1-d kt-1 k̂ * t 1 MPk t-1 Note a rise in r or d results in a lower desired capital stock r MPk t-1-d kt-1 k̂ * t 1 Higher r MPk t-1 r MPk t-1-d kt-1 k̂ * t 1 Higher d MPk t-1 r MPk t-1-d kt-1 k̂ * t 1 MPk t-1 k̂ (r, d ) * t 1 k̂ (,) * t 1 r MPk t-1-d kt-1 k̂ * t 1 k̂ * t 1 Desired Capital Stock But we are interested in investment, not desired capital stock How do we get from desired capital stock to investment? Investment is the difference between the desired capital stock, and the existing capital stock Investment is the difference between the desired capital stock, and the existing capital stock Existing Capital Stock: Capital in place last period less whatever wore out. (1-d)kt-1 Investment is the difference between the desired capital stock, and the existing capital stock i k̂ * t 1 (1 d )k t 1 i k̂ * t 1 (1 d )k t 1 i k̂ (r, d ) (1 d )k t 1 * t 1 (-,-) i(r, d , k t1 ) i(, ,) But what about d? i k̂ * t 1 (1 d )k t 1 i k̂ (r, d ) (1 d )k t 1 * t 1 (-,-) i(r, d , k t1 ) i(, ? ,) r i(r, d , k t1 ) id i r Empirically we know that: di dc dr dr And… id i r c i : : is approximat ely 4 : 1 y y Id I So what does the aggregate economy look like now? r Notice id is flatter than cd r0 cd id i0 c0 And total aggregate demand is id plus cd r r0 cd id i0 yd=cd + id) c0 y0 r And equilibrium depends on aggregate demand and supply ys r0 cd id i0 yd=cd + id) c0 y0 So now we have described the model with Investment.. r ys r0 id cd yd=cd + id) i0 c0 y0 And we are now in a position to return to our business cycle shocks. Case 1: Lets revisit a temporary negative productivity (Supply) shock and ASSUME that the MPk has not changed r ys r0 cd id i0 yd=cd + id) c0 y0 Investment is acting as a buffer, absorbing the bulk of the fall in output and allowing c to fall by only a small amount. i y c i y c But we haven’t yet got our acyclical interest rate Case2: ASSUME now that a temporary negative shock reduces the MPk in the future ONLY. r ys r0 cd id i0 yd=cd + id) c0 y0 Note this is a KEYNESIAN recession • We have a fall in the expected value of future capital returns Mpke • This is Keynes’ Animal Spirits • And it manifests itself primarily as a demand shift In general would expect a recession to have elements of both cases 1 & 2 r s* y cd ys r0 yd=cd + id) id id* i0 1. c0 ys shifts in, as does id y0 4. By how much does yd fall as id and cd fall? r ys* ys cd cd* r0 yd=cd + id) id id* i0 c0 y0 This is absolutely key to understanding our results If the shift in yd is smaller than the shift in ys .. r ys* ys cd cd* r0 yd=cd + id) id yd* id* i0 c0 y0 4.b But if the shift down in yd is bigger than the shift in ys r ys* ys cd cd* r0 yd=cd + id) id yd* id* i0 c0 y0 TIME FOR A BIG SUMMARY 1. 2. 3. 4. 5. Negative productivity Shock Causes ys and id to shift …... cd shifts ………... due to PIH yd shifts…... as cd and id shift in HOW MUCH DOES yd SHIFT IN TIME FOR A BIG SUMMARY 5. HOW MUCH DOES yd SHIFT IN 6. If the shift is ……... (MPk effect is ……....) 7. . 8. r ……..., y ……... 9. c ………….. 10. i …………. TIME FOR A BIG SUMMARY 5. HOW MUCH DOES yd SHIFT IN 6. If the shift is ……... (MPk effect is ……....) 7. . 8. r ……..., y ……... 9. c ………….. 10. i …………. In repeated shocks what would we see? 1. y falls 2. Sometimes r up, sometimes down (acyclical) 3. c would ………….. 4. i would …………... 5. y down, and change in r = 0 on average L(y,R) = L(-,0), Md …….., so P …... 6. Hours worked ……... if MPL effect strongest So Now We Have a Theoretical Model Capable of Explaining All the Stylised Facts So Now We Have a Theoretical Model Capable of Explaining All the Stylised Facts In fairness, some results depend on some effects being greater or less than others (e.g. hours worked, interest rates etc) It is an empirical question whether this is actually the case. So Now We Have a Theoretical Model Capable of Explaining All the Stylised Facts So we need to build a model economy like Chapters, 2, 4, 5 and 12, with realistic parameters for the production function, tastes for work and leisure, and investment function etc and check whether such an economy can replicate the observed stylised facts.