Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

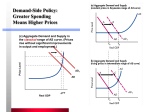

CHAPTER NINE NOTES-AP I. WHAT DETERMINES GDP? A. THE NEXT TWO CHAPTERS FOCUS ON THE AGGREGATE EXPENDITURES MODEL. DEFINITIONS AND FACTS FROM PREVIOUS CHAPTERS ARE USED TO SHIFT OUR STUDY TO THE ANALYSIS OF ECONOMIC PERFORMANCE. THE AE MODEL IS ONE TOOL USED IN THE ANALYSIS. B. THE MODEL ORIGINATED WITH JOHN MAYNARD KEYNES. THUS IT IS ALSO CALLED THE KEYNESIAN MODEL. C. THE FOCUS IS ON THE RELATIOSHIP BETWEEN INCOME CONSUMPTION AND SAVINGS. D. INVESTMENT SPENDING, AN IMPORTANT PART OF AGGREGATE EXPENDITURES, IS ALSO EXAMINED. E. FINALLY, THESE SPENDING CATEGORIES ARE COMBINED TO EXPLAIN EQUILIBRIUM LEVELS OUTPUT AND EMPLOYMENT IN A PRIVATE (NO GOVERNMENT), DOMESTIC (NO FOREIGN TRADE). THEREFORE, GDP=NI=PI=DI IN THIS VERY SIMPLE MODEL. II. SIMPLIFYING ASSUMPTIONS FOR THIS CHAPTER. A. A “CLOSED ECONOMY” WITH NO FOREIGN TRADE. B. GOVERNMENT IS IGNORED, FOCUS IS ON PRIVATE SECTOR. C. ALTHOUGH BOTH HOUSEHOLDS AND BUSINESSES SAVE, WE ASSUME THAT ALL SAVINGS IS PERSONAL. D. DEPRECIATION AND NET FOREIGN INCOME ARE ASSUMED TO BE ZERO FOR SIMPLICITY. E. WITH NO GOVERNMENT AND FOREIGN TRADE THE EQUATION IN IE IS CORRECT. III. TOOLS OF AGGREGATE EXPENDITURES THEORY A. THE THEORY ASSUMES THAT THE LEVEL OF OUTPUT AND EMPLOYMENT DEPEND DIRECTLY ON THE LEVEL OF AGGREGATE EXPENDITURES. CHANGES IN OUTPUT REFLECT CHANGES IN AGGREGATE SPENDING. B. CONSUMPTION AND SAVINGS: SINCE CONSUMPTION IS THE LARGEST COMPONENT OF AGGREGATE SPENDING, WE ANALYZE ITS DETERMINANTS. 1. DISPOSABLE INCOME IS THE MOST IMPORTANT DETERMINANT OF CONSUMER SPENDING a. WHAT IS NOT SPENT IS CALLED SAVING b. THEREFORE: DI – C = S OR C +I = DI 2. SEE FIGURE BELOW: 45 0 LINE C C 0 DI FORTY FIVE DEGREE LINE REPRESENTS ALL POINTS AT WHICH CONSUMER SPENDING IS EQUAL TO DISPOSABLE INCOME. OTHER POINTS REPRESENT ACTUAL C, DI RELATIONSHIPS. 3. THE GRAPH ILLUSTRATES THAT AS DISPOSABLE INCOME INCREASES SO DO CONSUMPTION AND SAVING. 4. SOME CONCLUSIONS a. HOUSEHOLDS CONSUME A LARGER PORTION OF THEIR INCOME. b. BOTH CONSUMPTION AND SAVING ARE DIRECTLY RELATED RELATED TO THE LEVEL OF INCOME C. AVERAGE AND MARGINAL PROPENSITIES TO CONSUME AND SAVE APC = C/I APS= S/I MPC = CHANGE IN C / CHANGE IN I MPS = CHANGE IN S / CHANGE IN I D. NONINCOME DETERMINANTS OF CONSUMPTION AND SAVING 1. WEALTH – INCREASE IN WEALTH SHIFTS C UP AND S DOWN 2. EXPECTATIONS – CHANGES IN EXPECTED INFLATION CAN AFFECT CONSUMPTION TODAY 3. HOUSEHOLD DEBT – INCREASE SHIFTS C DOWN AND UP; DECREASE SHIFTS C UP AND S DOWN 4. TAXES – DECREASE SHIFTS BOTH UP AND INCREASE SHIFTS BOTH DOWN E. SHIFTS AND STABILITY 1. MOVEMENT FROM ONE POINT ON CURVE TO ANOTHER IS CALLED CHANGE IN AMOUNT CONSUMED. A SHIFT IN SCHEDULE IS CALLED A CHANGE IN C SCHEDULE 2. SCHEDULE SHIFTS-C AND S SCHEDULES WILL ALWAYS SHIFT IN OPPOSITE DIRECTIONS UNLESS CAUSED BY A CHANGE IN TAXES. 3. STABILITY-ECONOMISTS BELIEVE THAT C AND S ARE GENERALLY STABLE UNLESS DELIBERATELY CHANGED BY A GOVERNMENT ACTION IV. INVESTMENT A INVESTMENT CONSISTS OF BUILDING NEW PLANTS, CAPITAL EQUIPMENT, MACHINERY, INVENTORIES, CONSTRUCTION, ETC. 1. THE INVESTMENT DECISION WEIGHS MARGINAL COSTS AND MARGINAL BENEFITS 2. THE EXPECTED RATE OF RETURN IS THE MARGINAL BENEFIT AND THE INTEREST RATE IS THE MARGINAL COST. B.EXPECTED RATE OF RETURN IS FOUND BY COMPARING THE EXPECTED ECONOMIC PROFIT (TOTAL REVENUE MINUS TOTAL COST) TO COST OF INVESTMENT TO GET RATE OF RETURN (SEE TEXT EXAMPLE) C. THE REAL INTEREST RATE, i, IS THE COST OF OF INVESTMENT 1. INTEREST RATE IS EITHER THE COST OF BORROWED FUNDS OR THE COST OF INVESTING YOUR OWN FUNDS (INCOME FOREGONE) 2. IF INTEREST RATE EXCEEDS THE EXPECTED RATE OF RETURN, THE INVESTMENT SHOULD NOT BE MADE. D. INVESTMENT DEMAND SCHEDULE SHOWS AN INVERSE RELATIONSHIP BETWEEN THE INTEREST RATE AND AMOUNT OF INVESTMENT (SEE GRAPH) E. SHIFTS IN INVESTMENT SCHEDULE-SHIFTS IN INVESTMENT DEMAND OCCUR WHEN ANY DETERMINANT APART FROM INTEREST RATE CHANGES 1. GREATER EXPECTED RATE OF RETURNS CREATE MORE INVESTMENT DEMAND (SHIFT CURVE TO THE RIGHT) a. ACQUISITION, MAINTENANCE, AND OPERATING COSTS MAY CHANGE b. BUSINESS TAXES MAY CHANGE c. TECHNOLOGY MAY CHANGE d. STOCK OF CAPITAL GOODS ON HAND WILL AFFECT NEW INVESTMENT e. EXPECTATIONS CAN CHANGE THE VIEW OF EXPECTED PROFITS F. INVESTMENT IS A VERY UNSTABLE TYPE OF SPENDING, IT IS MORE VOLATILE THAN GDP 1. CAPITAL GOODS ARE DURABLE GOODS SO SPENDING CAN BE POSTPONED OR NOT 2. INNOVATION OCCURS IRREGULARY 3. PROFITS VARY CONSIDERABLY 4. EXPECTATIONS CAN BE EASILY CHANGED G. EQUILIBRIUM GDP AND GDP GAPS C DI Leakages-injections approach Injections: investment, exports, government spending, consumption Leakages: savings, taxes, imports,