Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

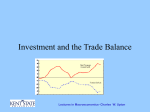

Chapter 5 Investment and Saving Equivalence of Saving and Investment • One of the key relationships in the NIPA balance is that investment must always be equal to saving on an ex post basis, even though they may be quite different on an ex ante basis. • This is not merely an accounting identity, but is at the heart of understanding how the economy functions. An ex ante rise in investment • Suppose firms decide to invest more, but consumer saving patterns are unchanged and profits have not risen. Where do firms get the extra money? • They borrow it by offering higher interest rates. When that happens, consumers save more. Also, that is likely to attract more foreign saving. The increase in investment plans boosts real GDP and increases government saving. Also, when interest rates rise, some firms decide to postpone their purchase of capital goods. • On an ex post basis, S and I balance. An ex ante rise in saving • Now suppose consumers become worried about the future, so they spend less and save more. However, these same factors also apply to businesses, which become more pessimistic and invest less. Yet on an ex post basis, the change in I and S must be equivalent. • Interest rates will probably decline in consumers decide to save more, but in a recessionary environment that may not stimulate investment. • The recession will reduce government saving, and less foreign saving will be attracted. But sometimes even these adjustments are not sufficient. • When consumers cut back on spending, income will fall and unemployment will rise. Thus while consumers plan to save more, they actually end up saving less. Reversing the Recession • When that happens, monetary and fiscal policy are likely to ease, which will reduce interest rates further, hence stimulating consumption and investment. • If that is insufficient, the recession may continue indefinitely. • Most of the time, business cycle fluctuations are caused by ex ante shifts in investment rather than saving. Determinants of Capital Stock • Firm wants to maximize its expected real rate of return on investment. • It will increase capital stock when it thinks the rate of return on that investment will be higher than the rate of return that can be earned from alternative use of those funds. • Thus investment will be negatively correlated with the cost of funds, part of which is the rate of interest. Other factors include the rate of depreciation and various tax laws. Factors Affecting the Expected Rate of Return • Firms will expect the rate of return on investment to be higher if output is likely to increase. • They are also more likely to invest if existing capital stock is fully utilized, and less likely if they already have excess capacity. • Firms are more likely to buy new equipment to replace old if technology has advanced rapidly. Availability of Credit • Large firms can always borrow funds in capital markets. But some investment is undertaken by firms that cannot borrow as much as desired. • For those firms, credit availability is also an important factor. • Also, some firms rely on equity financing, so the price/earnings ratio of the stock market is also important. Expectations • Output, capacity utilization, interest rates, availability of credit, the stock market, and tax laws are all important determinants of investment. Yet because most capital spending will remain in service for many years, expectations about the future are paramount. • Whereas unusually low interest rates and greater credit availability will almost always stimulate consumer spending, they will not boost investment if firms think the additional equipment will simply remain idle. Expectations (Slide 2) • No one has yet figured out how to measure expectations precisely, and no economist has yet figured out how to predict them. • However, the best available measure we have of business expectations is the stock market. • As a result, the stock market is an important determinant of capital spending for several reasons: cost of capital, availability of capital for firms that cannot borrow very much, and as a measure of expectations • The stock market has a much greater impact on investment than consumption. Lags in Capital Spending • Unlike consumers, who often purchase goods and services without any delay, planning for capital expenditures usually involves a substantial time delay. • Even after the goods are ordered, it may be several months or even years (large aircraft) before they are delivered. • As a result, capital spending generally lags the business cycle. Tax Policy • In the post World War II period, many attempts have been made to adjust fiscal policy to affect capital spending. • Some have been designed to increase the long-term ratio of capital spending to GDP • Some have been designed to boost investment during recessions and reduce it during periods of overfull employment. Implements of Tax Policy • The major methods used to achieve these goals have been: • Adjusting the rate of investment tax credit • Adjusting depreciation schedules by allowing faster (or slower) writeoffs. • Changing the statutory corporate income tax rate. • Reducing the tax rate on capital gains or dividends, hence boosting the stock market Do They Work? • These tools have remained controversial, not only among liberals who think businesses already receive too many tax breaks, but among business leaders themselves, many of whom claim that investment decisions are made independent of tax considerations. Do They Work (Slide 2) • Economists generally agree that any tax break to stimulate investment will be partially offset by the increase in the government deficit, which may raise interest rates or “crowd out” private sector investment. • This is far less likely to happen when the economy is in recession and there is excess liquidity. But it is precisely at those times that investment is least likely to be boosted by stimulative tax policy. Do They Work (Slide 3) • A review of the past 50 years suggests that changes in policy have had some short-term impact on capital spending, but probably have not changed the long-term ratio of capital spending to GDP very much. • In particular, the cancellation of the investment tax credit in 1986 was followed by a temporary dip in capital spending, but capital spending soared during the 1990s because of improved expectations and faster growth in technology. Other Determinants of Saving • So far we have discussed consumer saving and capital spending. Two other key determinants of the saving = investment identity are: • Foreign saving • Government saving • Foreign saving is essentially equal to the trade balance with the opposite sign. The greater our trade deficit, for example, the greater foreign saving will be. This is true for the U.S. because the world is on a de facto dollar standard; that relationship does not necessarily hold for smaller countries. The Twin Deficits • During the 1980s, economists used to talk about the “twin deficits” – the Federal budget deficit and the trade deficit. Since the trade deficit is equal to foreign saving, essentially foreign investors paid for our deficit. • Thus it was sometimes claimed that if the government deficit declined, so would the trade deficit. Yet in the late 1990s, the government budget moved back into surplus, while the trade deficit rose faster than ever. In this case, foreign investors paid for our investment boom without consumers having to save more. • In the 2001 recession, investment dropped sharply, but foreign saving did not. Instead, it shifted back to paying for the government deficit. Economic Impact of the Trade Deficit • The “twin deficit” issue is mentioned prominently to emphasize that a trade deficit is not necessarily bad for the economy. • According to the fundamental identity C + I + G + F = GDP, a decline in net exports must necessarily reduce GDP. But that is not true. If F declines, the resulting increase in foreign saving may boost I. • In addition, the net export balance is countercyclical, falling in booms and rising in recessions. That moderate recessions and also helps to keep the economy from overheating Determinants of Exports • Foreign demand • Trade-weighted average value of the dollar, usually lagged about one year • For the U.S., the Repercussion Effect. When the U.S. economy booms, our imports rise, which means exports of other countries rise – so they can buy more exports from the U.S. The usual lag for this term is also about one year. Determinants of Imports • Domestic Demand • Value of the dollar, although that is not as important for imports as for exports, because most foreign countries adjust their prices to U.S. levels. • Capacity utilization: when bottlenecks occur in domestic production, imports rise more rapidly. Government Saving • The government saving rate is highly correlated with the growth rate. • In general, every 1% change in the growth rate changes the ratio of the government budget surplus or deficit to GDP by about ½%. • Thus, for example, if real growth fell from +4% to -2% (a typical recession) and the budget had been in balance, the deficit would rise to 3% of GDP (about $300 billion) even if no changes were made in spending programs or tax rates. Deficits – Good or Bad? • The political party in opposition – no matter which one – invariably jumps on this deficit figure as a sign of fiscal mismanagement. • Yet in fact it is an important positive development. Without this massive decline in government saving, saving and investment could be balanced only at the cost of a much more severe and long-lasting recession. Deficits – Good or Bad (Slide 2) • Most economists agree that the Federal budget should be balanced over the business cycle. It should be in deficit during recessions, and in surplus during periods of full employment. • Keeping the budget in deficit during the entire cycle generally crowds out private sector investment and hence reduces the long-term growth rate.