Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

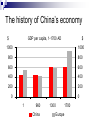

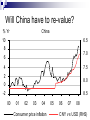

How emerging markets are shaping the world A brief analysis John Birchall As the US fades other are growing Global grow th contributions 2.0% 2.0% 1.5% 1.5% 1.0% 1.0% 0.5% 0.5% 0.0% 0.0% 95 96 97 98 99 00 01 02 03 04 05 06 US Emerging Other What is driving this? The collapsing price of technology Cost of transport and communications 120 The political openness generated 100 by, first, the adoption of outward looking policies by the Chinese 80 under Deng Xiaoping in the early 1980s and, second, by the fall of 60 the Berlin Wall in 1989 40 These are massive shocks that 20 have rocked the competitive equilibrium of the world economy 0 through both labour and capital flows The fall in real communications prices 120 100 80 60 40 20 0 1920 1930 1940 1950 1969 1970 1980 1990 Ocean Freight Transatlantic phone Air Satellite The history of China’s economy $ GDP per capita, 1-1700 AD $ 1000 1000 800 800 600 600 400 400 200 200 0 0 1 960 China 1300 1700 Europe Now it’s edging into the lead China's Geopolitical standing, 1820-2003 90 75 60 6 5 4 45 30 15 0 3 2 1 0 1820 1890 1913 1952 1978 2003 Per capita GDP % of World Av erage (LHS) Share of World Ex ports % (RHS) The US would have fallen faster if the merging markets had not been hungry for US goods % Yr US % Yr 20 20 10 10 0 0 -10 -10 -20 -20 90 92 94 Ex ports 96 98 00 02 04 06 08 Residential inv estment Who drives US export growth? % Pts Contributions to 2007 US export growth % Pts 2.0 2.0 1.5 1.5 1.0 1.0 0.5 0.5 0.0 0.0 da a n Ca na m any i h C Ger Ind ia zil a r B UK an rance w i F Ta an rabia rl and ussia p a e J A R z i t i d u w S Sa The Eurozone is increasingly influenced by China and Eastern Europe % Pts Contributions to 2007 Eurozone export growth % Pts De Ja Tu No rla n Sw e Ch Sw itz e Cz ec hR Ru Po la US 0.0 pa n 0.0 nm ark 0.2 rke y 0.2 rwa y 0.4 d 0.4 de n 0.6 ina 0.6 ep ub lic 0.8 ss i a 0.8 UK 1.0 nd 1.0 Japan id also increasing its dependence on emerging markets % Pts Contributions to 2007 Japanese export growth % Pts 3.0 3.0 2.5 2.5 2.0 2.0 1.5 1.5 1.0 1.0 0.5 0.5 0.0 0.0 na i h C e Kor a h Net ds n a l er s Rus ia g re nd ny n bia o a a o l a i p r K a a m r A g g Th di Ge Sin u Hon a S E UA M s alay ia lia a r t Aus The emerging markets influence on capital markets USDbn Total foreign ex change reserv e holdings USDbn 5000 5000 4000 4000 3000 3000 2000 2000 1000 1000 0 0 00 01 02 03 04 Dev eloping Countries 05 06 07 08 Dev eloped Countries This is driving demand for asset back securities USDbn USDbn 500 400 300 200 100 0 -100 500 400 300 200 100 0 -100 95 96 97 98 99 00 01 02 03 04 05 06 07 08 Official purchases Corporate equity Corporate bonds FDI But personal debt is also increasing % GDP US outstanding debt % GDP 100 100 80 80 60 60 40 40 20 20 90 93 96 99 02 Non-financial corporate business 05 Households Might loose monetary discipline in emerging markets be partly responsible for commodity price increases? Index 2000 = 100 USD/BBL 350 300 250 200 150 100 50 120 100 80 60 40 20 0 00 01 02 03 04 05 06 07 Economist food prices (LHS) Economist metal prices (LHS) Brent oil prices (RHS) 08 Have US consumers finally run out of steam? % Peak to Peak - US Consumption % 4.5 4.5 4 4 3.5 3.5 3 3 2.5 2.5 2 2 1.5 1.5 1 1 0.5 0.5 Q2 1953 - Q3 1957 - Q2 1960 - Q4 1969 - Q4 1973 - Q1 1980 - Q3 1981 - Q3 1990 - Q1 2001 - Q3 1957 Q2 1960 Q1 1980 Q1 2001 Q4 1969 Q4 1973 Q3 1981 Q3 1990 Q3 2007 And their spending on capital items is slowing % Peak to Peak - US total investment % 8.0 8.0 6.0 6.0 4.0 4.0 2.0 2.0 0.0 0.0 -2.0 -2.0 Q2 1953 - Q3 1957 - Q2 1960 - Q4 1969 - Q4 1973 - Q1 1980 - Q3 1981 - Q3 1990 - Q1 2001 Q3 1957 Q2 1960 Q4 1969 Q4 1973 Q1 1980 Q3 1981 Q3 1990 Q1 2001 Q3 2007 Will China have to re-value? % Yr China 10 6.5 8 7.0 6 4 7.5 2 8.0 0 -2 8.5 00 01 02 03 04 Consumer price inflation 05 06 07 08 CNY v s USD (RHS) Could Brazil (BRIC country) be the new leader? Index 2000=100 1.5 110 100 90 80 70 60 50 2.0 2.5 3.0 3.5 4.0 00 01 02 03 04 05 06 07 08 BRL v s USD Brazil nominal effectiv e ex change rate (RHS) The food price problem Cent/Bushel Wheat No.2, Hard (Kansas) Cent/Bushel 1500 1500 1250 1250 1000 1000 750 750 500 500 250 250 0 0 90 92 94 96 98 00 02 04 06 08 It’s across all markets $/MT Thai Rice prices (B Grade) $/MT 1200 1200 1000 1000 800 800 600 600 400 400 200 200 0 0 90 92 94 96 98 00 02 04 06 08 Stocks are low Mln tons Rice - ending stocks Mln tons 160 160 140 140 120 120 100 100 80 80 60 60 40 40 1978/79 1984/85 1990/91 1996/97 2002/03 Wheat also Mln tons Wheat - ending stocks Mln tons 220 220 200 200 180 180 160 160 140 140 120 120 100 100 1978/79 1984/85 1990/91 1996/97 2002/03 Problems of the developing world Food and energy price uncertainty makes inflation targeting more difficult… …and requires tough decisions on interest rates… …when the rise in global inflationary pressures is someone else’s fault