Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

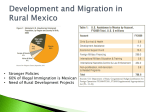

Drivers of Telecom in India Ashok Jhunjhunwala, TeNeT Group, IIT Madras, [email protected] Pan-IIT Conference - March 03 India’s Imperatives India has 1000 million people – – Upbeat Mood as Indian Telecom Poised for Growth – – 180 million households 40 million fixed line telephones, 12 million mobile and four million Internet connections 100 million lines by 2005 200 million lines by 2010 Customers Start to benefit – long distance cost tumbles from Rs 30 to Rs 5 per minute Primary Bottleneck Affordability – Telephone infrastructure cost (Capex) about Rs30K per line a few years back Finance Charge : 15% Depreciation : 12% Operation and Maintenance : 13% License fees, WPC charges, service tax: 10% 50 % of Rs 30,000 required as yearly revenue to break even – revenue of Rs 1200 per month What percentage of Indian Households can afford this? Urban Household Affordability Vs Monthly Telecom Spend* 40 70% 36 61% 35 60% Affordable HHs (In mn) Affordable HHs ( In %) 30 50% 22 40% 38% HHs In % HHs In Millions 25 20 30% 15 11 10 20% 19% 6 10% 5 10% 3 5% 1 0 2% 0% 220 330 440 630 940 Monthly Telecom Spend (in Rs) * For year 2002-03 at 25% unreported income & 3% income spend on telecom 1560 Rural Household Affordability Vs Monthly Telecom Spend* 35 25% 31 24% 30 Affordable HHs (In mn) 15% 20 15 11% 15 10% 10 6 5% 5 5% 3.0 2% 1% 1.4 0.50% 0 0% 130 190 260 360 550 910 Monthly Telecom Spend (in Rs) * For year 2002-03 at 25% unreported income & 1.75 % income spend on telecom HHs In % Affordable HHs ( In %) 25 HHs In Millions 20% India Requires Telecom Infrastructure at a Capital Expenditure (CAPEX) of under Rs 10,000 per line – – In doing so and serving the large potential market of India and other Developing Countries – Not a problem of the West, as affordability there is much higher a task of scientists of Developing Countries we can be amongst the world leaders in telecom technology CAPEX cost has fallen to about Rs 16000 per line – can get to Rs 10,000 per line in a few years Telecom Network Technology Contribution to CAPEX from Network Elements for emerging market – Backbone Network (contributes to 10% of CAPEX) – Fibre, WDM Networks, SDH Networks – Backbone Switches and Routers (contr. 5-10% of CAPEX) – Access Network (contributes to 60 to 65% of CAPEX) – – Mobile, Fixed Wireless and Fibre Access Service Platforms (contributes to 10 to 15% of CAPEX) – OMC, Customer Care & Billing, NMS, IN Services and ISP platforms Backbone Network BSNL has fibre going to most taluka (county) headquarters Reliance, Bharati and Tata laying fibre feverishly Technology – WDM Network – mostly obtained from Lucent, Alcatel, Nortel, Sycamore etc. SDH Network Hwawei, UTStarcom, ZTE, Tejas Network dominate Chinese and Indian cost-effective technologies India has a fibre 10 km from almost any village in 85% area Access Network Contributes to 60 to 65 % of per line CAPEX – Mobile Cellular : GSM/GPRS and IS-95/3G-1X costs have significantly come down : rapid expansion likely technologies dominated by Ericcson, Nokia, Siemens, Lucent, Qualcom etc. – – Korean companies enter via IS-95/3G-1X Fixed Wireless : providing fixed telephone and Internet to homes and offices – Fibre Access Network : dominate urban centers Fixed Wireless: dominated by corDECT WiLL To PSTN To Internet 35 kbps Internet (premium rate of 70 kbps) plus simultaneous telephone at Rs 8K per line Fibre Access Network Emerging as best option to connect dense urban areas – For Residential Areas Fibre to the street corner with POTS, DSL or Ethernet on Copper for 500 m combined with 802.11 wireless tomorrow may replace coaxial based cable TV tomorrow . – For Commercial Areas – Fibre to the Building with Ethernet in Building Technologies dominated by Indian and Chinese companies Huawei, ZTE, UTStarcom, Midas Rural Opportunity India has 600,000+ villages – 650 million people, Rs 600,000 Crores Rural annual GDP Can we double the Rural GDP in the next ten years…. Connecting Rural India – BSNL’s Contribution: on the average one fibre connected rural exchange for every 150 sq km a wireless system with 10 km range at existing fibre connected exchange would cover 80 - 85% of villages in India – India need a communications company which would focus and operate only in Rural Areas looks at rural areas as large potential business and provides wireless Internet connectivity in villages thinks and acts rural Innovative Technologies & Business Models N-Logue : A Rural Service Provider – aggregate demand into a kiosk using – corDECT Wireless in Local Loop ISP in a box : Minnow Reliable power back-up Rs 50,000 (including taxes) per Kiosk providing telephone, Internet, multimedia PC with web-camera, printer and 4 hour power back-up for PC – plus Indian language software set up by a village entrepreneur on the line of STD PCOs needs Rs 3000 per month to break even n-Logue Deployment Strategy Telephone Backbone Application & Content Providers Internet Backbone • • • • • Scope: 1 –3 Talukas 25 Km radius, 2000 sq km 4 – 5 lakh population 2 - 5 towns 300 -400 villages 500 + Connections (at least 1 in each village) ACCESS CENTRE Connections: • Individuals • Government — schools and PHCs • Kiosks LSP Banks KIOSK OPERATOR Rs. 50,000 / Kiosk Banks Micro Finance Organisations What is the monthly income? STD PCO Children learn typing – Kiosk is a photography shop – Rs 300 Rs 300 voice mail and video mail Rs 500+ e-governance access – also a video parlour on weekend evenings Rs 500+ email and browsing – all kinds of on-line and off-line education Rs 500+ connect to taluka Government office for services Rs 200 and much more Word-processor in Indian Languages Multi-lingual Office Package IITM Chennai Kavigal Mailclient in Tamil Mundi . . . . A 60 year old from a village near Melur – – Palaniamma had lost vision in both eyes since 2 years through the Aravind process Doctors confirmed that vision can be restored in at least one eye IITM trying to develop Remote Diagnostic tools – – Blood Pressure, Sugar & Iron, ECG Monitor, stethescope at total cost of Rs 10,000 Crop Consultancy Top: Ladies Finger Diseased with yellow mosaic Below : Post treatment Saving of Rs 140,000 for the farmers Cost of information Rs 20 Can Kiosks become Micro-banks? TeNeT and n-Logue working with ICICI – – – – – Remote Bill Payment Rural ATM Micro-finance Remittance better credit assessment Credit and Product Marketing is one of the biggest requirement of Rural India Do we have a model for sparser areas? Fibre not available in 15% of areas Only about 50 to 100 villages in 20 Km radius – – less population per village less available money Technology Intervention Business Intervention – finance and buying/selling may make even larger sense For inaccessible Rural Areas ISRO-IITM 3.8 m antenna 2.4 m antenna 15 -20 Kms with 100 connections PSTN Internet • 8-10 voice channels + 64/128 kbps Internet satellite backhaul • Each hub supports 16 to 20 remote sites with 2 Mbps downlaod • Rs 10,000 corDECT + Rs 10,000 backhaul cost per connection To Sum Up Telecom will take off in a major way in India in coming years – – most regulatory hurdles crossed focus on reduction on CAPEX Can Telecom help in Doubling India’s Rural GDP – – will change India Internet is Power can we have a micro-bank in every village in the next five years