Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

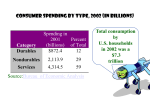

South African Savings Institute 31 July 2007 How to get SA to save Jac Laubscher Group Economist: Sanlam Long-term trends • Declining savings ratio Gross domestic savings (% of GDP) Long-term trends • Declining savings ratio • Rising investment ratio Saving vs. investment (% of GDP) Long-term trends • • • • • Declining savings ratio Rising investment ratio Increasing dependence on foreign savings Deteriorating sovereign balance sheet Not sustainable in the long run Economic growth vs. investment ratio Economic growth vs. savings rate Who are the savers? • Corporates • Households • Government Savings rates (% of GDP) How has government been doing? Government dissaving has been eliminated Reasons for poor government savings • Government savings = Current income minus current • expenditure Current expenditure too high Military expenditure Salaries and wages Social grants • Capital expenditure too low Lack of long-term vision Priority of consolidation Capacity constraints What to do about government savings • Contain current expenditure: wage bill, transfer payments • Increase capital expenditure: address capacity • Continue with budget surpluses How has households been doing? Household savings rate (% of GDP) Household saving (% of disposable income) Reasons for poor household savings • Savings = f (income, propensity to save) • Low disposable income growth Low economic/ employment growth Rising tax burden Growth in real personal disposable income Economic growth Personal income tax (% of disposable income) Reasons for poor household savings • Savings = f (income, propensity to save) • Low disposable income growth Low economic/ employment growth Rising tax burden • Low propensity to save Lack of confidence in the future High inflation: “buy before prices rise” Financial deregulation plus asset price inflation Household debt (% of disposable income) Reasons for poor household savings ● Savings = f (income, propensity to save) ● Low disposable income growth Low economic/ employment growth Rising tax burden ● Low propensity to save Lack of confidence in the future High inflation: “buy before prices rise” Financial deregulation plus asset price inflation Instant gratification rather than sacrifice: “I want it all and I want it now” Redistribution policies What to do about household savings • • • • Faster growth in disposable income Temper redistribution policies Reduce income taxes, increase consumption taxes Create a savings culture Discipline Sacrifice Financial independence Taking a long-term view How has corporates been doing? Corporate saving (% of GDP) Reasons for poor corporate savings ● Corporates save to reinvest: balance sheet optimisation Corporate saving vs. private investment Reasons for poor corporate savings • Corporates save to reinvest: balance sheet optimisation • Require profitable investment opportunities Relatively high cost of capital Labour market inflexibility Relatively high corporate taxes Corporate tax (% of profit) 2005 1 Ireland 12,5 6 Chile 17,0 17 Brazil 25,0 17 Korea 25,0 27 Malaysia 28,0 31 Mexico 29,0 31 South Africa 29,0 36 Australia 30,0 41 China 33,0 (25,0) 45 India 33,66 Corporate tax (% of GDP) 2005 1 Estonia 1,4 2 Germany 1,8 11 Brazil 2,3 22 China 2,9 25 India 3,2 28 Ireland 3,4 37 South Korea 4,1 43 Australia 5,3 44 Malaysia 5,3 50 South Africa 6,4 Reasons for poor corporate savings • • Corporates save to reinvest: balance sheet optimisation Require profitable investment opportunities Relatively high cost of capital Labour market inflexibility Relatively high corporate taxes Low economic growth High existing market shares Lack of export opportunities Lack of entrepreneurial vision? Lack of confidence in the future? Short-termerism: share buy-backs, special dividends? Business confidence vs. private investment What to do about corporate savings • • • • • • • Create profitable business opportunities Reduce cost of doing business Create positive business environment, e.g. regulation Encourage competition Reduce corporate taxes Provide well designed incentives Temper BEE policies Conclusion To save or to perish: that is the choice!