Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

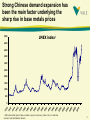

Chinese economic growth and the demand for metals China and the world economy Roberto Castello Branco EPGE, March 2011 1 Agenda Growth skepticism Chinese role in the global metals markets Are commodity exporters doomed to poverty? 2 Growth skepticism 3 The Asian growth path showed a sharp contrast with the experience of developed nations Real per capita GDP growth – developed economies 550 500 450 index 400 350 300 250 200 150 100 50 1820 1830 1840 1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 Source: Angus Maddison, “Countours of the world economy, 1-2030 AD”, Oxford University Press, 2007 4 Since the second half of the 20th century Asian economies have experienced unprecedented growth rates Real per capita GDP 1,100 China 1,000 Korea 900 800 Taiwan index 700 Japan 600 500 400 300 200 100 0 t t+5 t + 10 t + 15 t + 20 t + 25 t + 30 years after the start of growth acceleration Sources: Vale and Penn World Tables 5 Expansion multiples of GDP China¹ 12.5 Korea² 8.2 Taiwan² 7.8 Japan³ 6.9 Hong Kong² 6.7 Singapore² 6.6 Developed economies4 5.3 1 1978-2007 1965-1994 3 1950-1979 4 1820-1950 Sources: Vale and Penn World Tables 2 6 Gross enrollment rates in China Primary school Secondary school Tertiary school 1980 113 46 2 2006 111 76 19¹ ¹ 2005 Sources: US NCES and UNESCO 7 Sources of China’s growth % Output Contribution of total factor productivity 1978-2004 9.3 3.8 1978-1993 8.9 3.6 1993-2004 9.7 4.0 Source: “Accounting for growth: comparing China and India”, B. Bosworth and S. Collins, NBER working paper 12943, February 2007. 8 Chinese role in the global metals markets 9 Vale is one of the largest companies in the world Vale position in the FT 500 ranking¹ 500 400 300 200 100 1 18 February 28, 2011 2010 2009 2008 ¹ Ranking of the 500 largest companies in the world by market cap – 2007 Financial Times, position on 31 March of each year 20 42 25 74 2006 117 2002 446 2003 334 2004 275 2005 153 10 A global company, with offices and operations on all continents… Vale in 2011 11 ... and a global base of world-class assets Asset base by geography Asset portfolio Iron ore & pellets Asia 10% Australasia 10% Other 1% Manganese & ferroalloys Nickel, cobalt & PGMs North America 25% Potash & phosphates Coal Brazil 54% Copper Logistics 12 A large exposure to Asia: major operations and offices in the Asia Pacific 13 Supporting Asian growth Revenues 2002 US$ 4.3 billion 2010 US$ 46.5 billion China 7.7% China 33.1% Asia 26.6% Asia 53.3% 14 We are the only company in the Americas listed on a major Asian stock exchange New York 2000 Paris 2008 Hong Kong 2010 São Paulo 1943 ¹ with the listing in Hong Kong. 15 China’s steel consumption intensity has been much higher than the US peak level not only due to accelerated growth but also due to structural characteristics Steel consumption intensity ton / US$ 1,000 of real GDP 70 60 50 40 30 20 10 US China 2008 2001 1994 1987 1980 1973 1966 1959 1952 1945 1938 1931 1924 1917 1910 1903 0 Source: World Steel Association, IMF, USGS and Vale 16 China’s consumption intensity of base metals has surpassed developed economies Copper consumption intensity Nickel consumption intensity kilos / US$ 1,000 of real GDP kilos / US$ 1,000 of real GDP 900 70 800 60 700 50 600 40 500 400 30 300 20 Developed economies 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 0 1999 2009 2007 2005 2003 2001 1999 1997 1995 0 Source: World Steel Association, WBMS, IMF and Vale China 10 1998 Developed economies 1997 100 1996 China 1995 200 17 As a consequence, China has become the number one consumer of industrial metals in the world Share of China in global consumption of metals % 70 60 Iron Ore 50 Steel Nickel 40 Copper 30 20 10 Source: World Steel Association, WBMS, IMF and Vale 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 0 18 Strong Chinese demand expansion has been the main factor underlying the sharp rise in base metals prices 5,000 LMEX index¹ 4,500 4,000 3,500 3,000 2,500 2,000 1,500 1,000 500 19 70 19 72 19 74 19 76 19 78 19 80 19 82 19 84 19 86 19 88 19 90 19 92 19 94 19 96 19 98 20 00 20 02 20 04 20 06 20 08 20 10 0 ¹ LME base metals prices index, includes: copper, aluminum, nickel, zinc, tin and lead Sources: Vale and Reuters Ecowin 19 The increase in relative scarcity is driving the upward long-term trend for iron ore prices 1900 - 2009 5.0 Real iron ore prices Long-term trend log scale, real US$/ton¹ 4.5 4.0 3.5 3.0 1909 1919 1929 1939 ¹ prices in 2009 US$/ton, deflated by the CPI. Sources: USGS and Vale 1949 1959 1969 1979 1989 1999 2009 20 Despite Chinese efforts to boost iron ore output, it is increasingly dependent on imports Chinese dependency on imported iron ore Share in global iron ore seaborne trade 70% 0.7 0.6 0.62 60% 0.5 50% 0.4 40% 0.3 30% 0.2 20% 0.1 10% 0 1985 1990 1995 Source: World Steel and Vale 2000 2005 2010 0% 1990 Japan 1995 Germany 2000 China 2005 2010 21 In the past, in a less liquid world, Japan played the dual role of being the demand driver and financier of mining Japanese trading companies acquired stakes in mining assets across the globe. Japanese official financial institutions provided funding for project development. Apparently, the Chinese are willing to replicate the Japanese experience to guarantee a steady supply of raw materials. 22 Lessons from the Japanese experience In the past there was no financial globalization. Different models: private sector versus state-owned companies. The Japanese investment was not sufficient to change the long-term trend. 23 Africa is the new mining frontier World nonferrous exploration budget Rest of world 17% Canada 16% Latin America 26% Africa 15% Southeast Asia 6% Source: Metals Economics Group, 2010. USA 7% Australia 13% 24 Are commodity exporters doomed to poverty? 25 The strong global demand growth for commodities caused significant gains in terms of trade for Brazil 180 170 index, 1990 = 100 160 150 140 130 120 110 100 90 2011 2008 2005 2002 1999 1996 1993 1990 80 Source: Funcex 26 Commodity exporters can be rich Commodities and economic development US Australia Canada (A) Commodity exports¹ - US$ billion New Zealand Norway Chile Brazil 308.2 128.2 175.9 17.6 93.1 34.1 83.0 1,068.5 195.5 324.2 24.8 120.1 53.8 153.0 14,119.1 994.3 1,336.1 117.8 (A) / (B) - % 28.8 65.6 54.3 71.0 77.5 63.4 54.2 (A) / (C) - % 2.2 12.9 13.2 15.0 24.6 21.1 5.3 100.0 87.1 85.7 60.2 118.4 47.3 22.1 (B) Total exports ¹ - US$ billion (C) GDP¹ - US$ billion Real per capita GDP relative to the US, 2007 - % ¹ 2009 Sources: IMF, Haver Analytics, PennWorld tables, MIDC-SECEX, StatCan, Statistics Norway. 378.6 161.7 1,574.0 27 Natural resources and economic growth Investment in human capital and infrastructure. Quality of institutions. Policies stimulative of private sector investment. Flexible exchange rate regime. Countercyclical fiscal policies. 28 www.vale.com [email protected] Vale: a global leader 29