Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

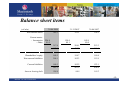

MACINTOSH RETAIL GROUP NV Half-Year Figures 2008 “Difficult retail market causes lower results” Should different interpretations arise between the Dutch and English version of this presentation, the Dutch version prevails Analyst- and Press conference Augustus 28, 2008 Frank De Moor (CEO) Profile Macintosh Retail Group Market developments H1 2008 Developments per sector/shop formats Theo Strijbos (CFO) Income statement Balance sheet items Cash flow/capex Frank De Moor Outlook 2008 -2- Profile Retail is our business - - Available non-food retail knowledge makes for satisfied customers; - Excellent store locations; - High quality back-office facilities and systems lead to cost leadership; - Direct sourcing/purchasing in East Asia through Macintosh Hong Kong; - Competence Centers. Non-food retailer in NL, B and Fr and UK; Living, Fashion, Automotive & Telecom; 1,300 shops; retail floor space of 710,000 m²; Store formats with leading market positions in NL targeting a broad range of consumers; - 200 million visitors annually; - Consumer sales: € 1.4 billion (70% NL); - Strong balance sheet. Objectives / Strategy - Growth, maintaining and increasing of existing activities; - ROCE > 12%; - Well balanced mix of activities with growth potential and cash flow generators; - Substantial acquisitions of structurally profitable, price-based formats in home decoration and shoe sectors. Sound basis for growth of earnings per share and dividend -3- Market developments 25 • 15 Index 5 -5 -15 -25 -35 jan-07 jul-07 Consumer confidence NL • • Willingness to buy NL jan-08 Consumer confidence B Consumer confidence Fr jul-08 Consumer confidence UK Economic developments resulted in a significant fall in consumer confidence and willingness to buy. Non-food retail market NL: + 0.9%. Negative development in several markets relevant to Macintosh: - NL home decoration: + 0.9% (CBS). CBW: entire living market: – 2.5%. - shoes NL: + 2.8% (GfK); - 6.4% (VGS). - post-paid telecom: - 3% in numbers and - 13% in value (GfK). -4- Living Profile • Kwantum: Largest home decoration discounter in Bnlx. • GP Décors: Home decoration specialist in Fr. m2 Number of shops Kwantum NL 93 (+3) 215,700 Kwantum B 8 (=) 8,300 GP Décors Fr 46 (-5) 42,900 x € mln Living H1 2008 • Higher turnover thanks to Kwantum. • Increase EBIT by more than 30%. Turnover EBIT EBIT-margin 2008 2007 132.7 9.2 6.9% 130.9 7.0 5.4% -5- Living H1 2008 Market • NL home decoration market: + 0.9% (CBS). CBW: total living market: - 2.5%. Kwantum • Higher turnover in NL due to organic growth and expansion with 3 shops. Increase of market share. In B, Kwantum recorded a rise in turnover with the same number of shops. • Higher gross margin in % of turnover results in substantially higher EBIT. • New 1,000 m² format in B offers potential, also in NL. GP Décors • Lower turnover also because of 5 closures. • EBIT lower. -6- Fashion Profile • Brantano: largest shoe retailer in B and largest out of town shoe retailer in UK. • Hoogenbosch: largest shoe retailer in NL in mid and upper segments. • Scapino: largest shoe discounter in NL. m2 Number of shops Number of shops m2 Brantano B/L Brantano UK 132 148 (+3) (+2) 95,300 79,200 Dolcis NL Manfield NL 98 66 (+1) (+3) 13,700 7,300 Scapino NL/G Scapino B 192 31 (+2) (=) 156,100 24,400 Invito NL Pro Sport NL 41 30 (+2) (+2) 3,500 2,100 Fashion H1 2008 • Rise in turnover due to acquisition Brantano. • Lower EBIT, mainly due to negative EBIT Brantano (effects of reorganisation / integration) and decrease at Scapino. x € mln Turnover EBIT EBIT-margin 2008 2007 288.7 4.0 1.4% 162.1 13.3 8.2% -7- Fashion H1 2008 Market • Shoe market negatively influenced by unfavourably mild winter and chilly spring. • NL: GfK: + 2.8%; VGS: - 6.4%. Brantano • Turnover: € 134.2 mln. Negative effect of deferred start clearance sales in B and lower exchange rate British pound. • Integration / reorganisation ahead on schedule. Annual savings of more than € 2 mln as from 2009. • Mainly because of direct and indirect costs of reorganisation/integration of some € 3 mln, EBIT in H1 negative. • Also integration costs in H2. Scapino • Lower turnover than in excellent H1 2007. • Lower EBIT due to effects on gross margin as a result of clearance sales, costs of expansion and higher running costs of shops. Hoogenbosch • Slightly lower turnover than in successful H1 2007. • Slight decrease in EBIT due to higher operation costs of shops. -8- Automotive & Telecom Profile • BelCompany: Market leader in mobile telecom in NL. Second independent telecom retailer in B. • Halfords: Largest retailer in NL for bicycles, bicycle and car accessories, car audio and navigation. Number of shops m2 BelCompany NL 172 (+9) 10,700 BelCompany B 69 (+9) 3,600 Halfords NL 150 (+2) 40,900 Halfords B 9 (=) 2,700 Automotive & Telecom H1 2008 • Lower turnover due to pressure on markets. • EBIT down because of decrease at BelCompany and Halfords. x € mln 2008 2007 Turnover 140.9 156.9 EBIT EBIT-margin 3.4 7.4 2.4% 4.7% -9- Automotive & Telecom H1 2008 Market • NL: Number of new subscription-based connections down with 3% and value down with 13% (GfK). More shops and further increase in internet sales. B: Number of phones sold down 16.5% (GfK). • NL: Navigation: - 8% in value and + 26.6% in numbers. Bicycles: - 0.8%; audio: - 4.9% (GfK). BelCompany NL • Substantially lower turnover. • Lower EBIT due to expansion costs and autonomous cost increases. BelCompany B • Lower turnover. • Adverse effect on EBIT. Halfords • Lower turnover due to levelling effects navigation market. • Lower EBIT. -10- Income statement (x € mln) 2008 2007 Turnover 562.3 449.9 Gross margin 255.2 (45.4%) 190.3 (42.3%) Costs - 240.8 (-42.8%) - 165.6 (-36.8%) EBIT 14.4 (2.6%) 24.7 (5.5%) Financial income and expense - 6.8 Taxes - 2.4 Net profit on continuing operations 5.2 17.0 Net profit discontinued operations 0 7.6 Net profit 5.2 24.6 - 2.2 (31.6%) - 5.5 (24.5%) -11- Balance sheet items (x € mln) 30.06.2008 31.12.2007 30.06.2007 345.3 195.1 196.1 Non current assets Current assets: - Inventories - Other 226.8 91.0 159.0 49.1 162.9 49.4 317.8 208.1 212.3 663.1 403.2 408.4 Shareholders' equity 184.5 198.7 169.4 Non-current liabilities 294.1 102.3 115.9 Current liabilities 184.5 102.2 123.1 663.1 403.2 408.4 293.0 90.9 118.2 Interest bearing debt -12- Cash flow / Capex (x € mln) - 2008 2007 Net profit 1. Depreciation and amortisation Cash flow 1. 5.2 15.4 20.6 17.0 10.0 27.0 EBITDA 29.8 34.7 Capex Of which in: - New/existing shops Information systems/logistics 17.1 12.4 14.4 2.0 9.7 2.0 1. on continuing operations -13- Outlook 2008 • Partly based on development of turnover at Macintosh in July / August, continuing pressure expected on consumer spending in relevant markets in H2 2008, in Fashion and Telecom in particular. • Investments will be assessed even more on direct return. • EBIT in H2 2008 may be lower than in H2 2007 (€ 42.2 mln). Therefore and given the slowdown in H1 2008, EBIT for full year 2008 will be lower than in 2007 (€ 66.9 mln). • Partly due to financing costs acquisition Brantano, net profit on continuing operations will be substantially lower than in record year 2007 (€ 47.5 mln). -14-

![H3 Turnover - [c] crabrock.net](http://s1.studyres.com/store/data/006486995_1-d3c1e811108ce44a4ea294ab9a5bd59a-150x150.png)