Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Ragnar Nurkse's balanced growth theory wikipedia , lookup

Exchange rate wikipedia , lookup

Monetary policy wikipedia , lookup

Business cycle wikipedia , lookup

Great Recession in Russia wikipedia , lookup

Long Depression wikipedia , lookup

Resource curse wikipedia , lookup

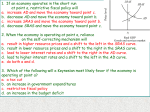

Ch 10 Analyze the impact of unanticipated changes in aggregate demand and short run aggregate supply Evaluate the economy’s self-correcting mechanism Anticipated change – foreseen in time to make adjustments Unanticipated change – not foreseen, appropriate adjustments were not made A change in the price level represents a movement along the curve Price Level P2 P1 AD Y2 Y1 Output Price Level Changes in things besides the price level shift the curve and (AD1) increase or (AD2) decrease aggregate demand AD1 AD2 AD0 Output 1. Increases in real wealth shift AD right ◦ a. Stock market ◦ b. Housing prices ◦ Example: The 1990s “new economy” 2. When the interest rate falls, AD shifts right because borrowing (for consumption and investment) becomes cheaper 3. When people are optimistic about the future, AD shifts right ◦ Consumer sentiment index ◦ “Animal Spirits” – Keynes ◦ “Irrational Exuberance” – Greenspan 4. When expected inflation is high, AD shifts right ◦ Less incentive to save, spend now 5. If other countries’ incomes are rising, AD shifts right ◦ Demand for U.S. exports increases as other countries prosper ◦ The larger the trade sector, the bigger the shift 6. When the dollar depreciates, AD shifts right ◦ Imports become more expensive ◦ Exports become cheaper ◦ So, NX will rise Increase in AD (shift right) Decrease in AD (shift left) ↑ in real wealth, stock mkt, housing ↓ in real wealth, stock mkt, housing ↓ in real interest rate ↑ in real interest rate Optimism about the future Pessimism about the future ↑ in expected inflation ↓ expected inflation ↑ real incomes abroad ↓ real incomes abroad ↓ ↑ value of nation’s currency prices value of nation’s currency prices Permanent change in production conditions ◦ Shift LRAS ◦ Shift SRAS Temporary change in production conditions ◦ Shift SRAS Price Level An increase in the economy’s production capacity will shift LRAS right LRAS1 LRAS2 Output (real GDP) Improvements in resource base Ch 16 Sources of Economic Growth ◦ Physical capital investment ◦ Human capital investment Improvements in technology Institutional and government policy changes ◦ Easy to conduct business ◦ Enforce contracts fairly ◦ Protect private property rights Increase in LRAS (shift right) Decrease in LRAS (shift left) ↑ in supply of resources ↓ in supply of resources Technology and productivity improvements Technology and productivity deteriorations Institutional changes that improve efficiency of resource use Institutional changes that reduce efficiency of resource use Note: Rightward shifts are much more common in the U.S. than leftward shifts, thank goodness! Price Level Increase in price level will increase quantity supplied in the short run SRAS P2 P1 Output Y1 Y2 Price Level Changes in things besides the price level shift the curve and (SRAS1) increase or (SRAS2) decrease short run aggregate supply SRAS2 SRAS0 SRAS1 Output (real GDP) 1. When resource prices fall, SRAS shifts right ◦ If the change is long-term, LRAS will shift also 2. When expected inflation is low, SRAS shifts right ◦ No benefit from holding onto goods to sell at a later date 3. Favorable supply shocks shift SRAS right ◦ Supply shock – unexpected event that temporarily increases or decreases aggregate supply ◦ Examples: OPEC increases output, favorable growing conditions Increase in SRAS (shift right) Decrease in SRAS (shift left) ↓ in resource prices (production ↑ ↓ in expected inflation ↑ in expected inflation Favorable supply shocks like good weather or lower prices of oil Unfavorable supply shocks like bad weather or higher prices of oil costs) in resource prices (production costs) Holding fiscal and monetary policy constant Ceteris Paribus (one change at a time) Do not cause equilibrium disruptions Decision makers plan for change No booms and busts Graph long run, steady economic growth: ◦ Long run equilibrium is the same as short run equilibrium (no disequilibrium) Higher output Lower price level Price Level LRAS1 LRAS2 SRAS1 SRAS2 P1 E1 P2 E2 AD Output YF1 YF2 Cause equilibrium disruptions, disequilibrium ◦ ◦ ◦ ◦ Increase in AD Decrease in AD Increase in SRAS Decrease in SRAS No economic growth is occurring ◦ Booms and busts ◦ LRAS will not shift Graphing ◦ What is the short run equilibrium? ◦ How do we return to long run equilibrium? Causes: unanticipated ◦ ◦ ◦ ◦ ◦ increase in real wealth fall of the interest rate optimism about the future rising incomes abroad, or depreciation of domestic currency Bull Market Short run ◦ ◦ ◦ ◦ Output higher than potential Price level rises unexpectedly Resource prices and interest rates fixed Producer profits are higher than normal Long run ◦ ◦ ◦ ◦ Resource prices, interest rates rise SRAS shifts left Return to full employment, normal profits Price level permanently higher Too Fast Price Level LRAS SRAS1 e2 P105 P100 E1 AD2 AD1 Output (real GDP) YF Y2 Price Level LRAS SRAS2 P110 P105 P100 E2 E1 SRAS1 e2 AD2 AD1 Output (real GDP) YF Y2 Causes: unanticipated ◦ ◦ ◦ ◦ ◦ decrease in real wealth rise of the interest rate pessimism about the future falling incomes abroad, or appreciation of domestic currency Bear Market Short run ◦ ◦ ◦ ◦ Output lower than potential Price level falls unexpectedly Resource prices and interest rates fixed Producer profits are lower than normal Long run ◦ ◦ ◦ ◦ Resource prices, interest rates fall SRAS shifts right Return to full employment, normal profits Price level permanently lower Resource prices are “downward sticky” ◦ Long term contracts ◦ Workers hesitant to accept lower wages ◦ Unions Can make adjustment process slow Too Slow Price Level LRAS SRAS1 P100 P95 E1 e2 Y2 YF AD1 AD2 Output (real GDP) Price Level LRAS SRAS1 SRAS2 P100 P95 P90 E1 e2 E2 Y2 YF AD1 AD2 Output (real GDP) Causes: unanticipated, temporary ◦ Favorable supply shock Good weather Cheap oil Best Party Ever! Price Level LRAS SRAS1 P100 SRAS2 E1 P95 e2 AD1 Output (real GDP) YF Y2 Well, all good things must come to an end. We had fun! Price Level LRAS SRAS1 P100 SRAS2 E1 P95 e2 AD1 Output (real GDP) YF Y2 Short run ◦ ◦ ◦ ◦ Output higher than potential Price level falls unexpectedly Resource prices and interest rates fixed Producer profits are higher than normal Long run ◦ ◦ ◦ ◦ Favorable conditions come to an end SRAS shifts left and returns to original position Return to full employment, normal profits No changes in prices or output in the long run Causes: unanticipated, temporary unfavorable supply shock Short run ◦ ◦ ◦ ◦ Output lower than potential Price level rises unexpectedly Resource prices and interest rates fixed Producer profits are lower than normal Long run ◦ ◦ ◦ ◦ Unfavorable conditions come to an end SRAS shifts right and returns to original position Return to full employment, normal profits No changes in prices or output in the long run Ugh, this sucks! Price Level LRAS SRAS2 SRAS1 P105 e2 P100 E1 AD1 Output (real GDP) Y2 YF Whew! Glad that’s over. Back to normal Price Level LRAS SRAS2 SRAS1 P105 e2 P100 E1 AD1 Output (real GDP) Y2 YF When AD shifts unexpectedly, the long run impacts are seen only in the price level When SRAS shifts unexpectedly, there are no long run impacts because the change was temporary When markets are allowed to adjust, we will always return to full employment and output Unanticipated changes in AD or SRAS can disrupt the economy But changes in ◦ Resource prices ◦ Interest rates Return the economy to long run equilibrium Recession (GDP less than YF) ◦ Weak demand for resources causes unemployment ◦ Resource prices then fall ◦ Return to full output Boom (GDP greater than YF) ◦ Strong demand for resources causes greater than normal profits ◦ Resource price then rise ◦ Return to full output Recession (GDP less than YF) ◦ Weak demand for borrowing ◦ Interest rates then fall ◦ Return to full output Boom (GDP more than YF) ◦ Strong demand for borrowing ◦ Drives up interest rates ◦ Return to full output Keynesian Economists: too long! New Classical Economists: not too long at all! Period of Expansion Length (in Months) Period of Recession Length (in Months) Oct ‘49 to Jul ’53 44 Jul ‘53 to May ’54 10 May ‘54 to Aug ’57 39 Aug ‘57 to Apr ’58 9 Apr ‘58 to Apr ’60 24 Apr ‘60 to Feb ’61 10 Feb ‘61 to Dec ’69 105 Dec ‘69 to Nov ’70 10 Nov ‘70 to Nov ‘73 36 Nov ‘73 to Mar ’75 16 Mar ‘75 to Jan ’80 58 Jan ‘80 to Jul ’80 6 Jul ‘80 to Jul ’81 12 Jul ‘81 to Nov ’82 16 Nov ‘82 to Jul ’90 92 Jul ‘90 Mar ’91 9 Mar ‘91 to Mar ’01 120 Mar ‘01 to Nov ’01 8 Nov ‘01 to Nov ’07 73 Dec ‘07 to June ‘09 18 Analyze the impact of unanticipated changes in aggregate demand and short run aggregate supply Evaluate the economy’s self-correcting mechanism