Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

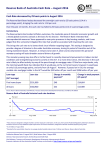

London’s Economy Today Issue 164 | April 2016 UK GDP continues to grow In this issue UK GDP continues to grow..................................1 Latest news.......................1 Economic indicators..........5 Socio-economic baseline – Old Oak and Park Royal....9 London’s Economy Today (LET) data to Datastore The LET presence on Datastore aims to create more interaction and a greater personal focus for London’s Economy Today while also allowing for the incorporation of feedback and views from the readership. http://data.london.gov.uk/ gla-economics/let/ By Gordon Douglass, Supervisory Economist, and Emma Christie, Economist New data for the UK economy published by the Office for National Statistics (ONS) in April shows that economic growth slowed in the first quarter of 2016. Thus the preliminary estimates of GDP showed that economic growth decreased to 0.4 per cent for the quarter, down from 0.6 per cent in the fourth quarter of 2015 (see Figure 1). Compared to a year ago, GDP growth remained flat at 2.1 per cent in the first quarter of 2016. The growth in GDP was driven by output increasing in services by 0.6 per cent, slowing from 0.8 per cent in the final quarter of 2015. Services contributed 0.5 percentage points to GDP growth which was offset by falls in other sectors. Business services and finance – a particularly important industry for London – grew by 0.3 per cent in Q1 2016 after growing by 0.7 per cent in the previous quarter. The ONS noted that growth in business services and finance “was the main reason behind the reduction in services growth between the 2 quarters”. UK productivity drops at the end of 2015 Despite the UK economy continuing to grow over the end of 2015 and into 2016, other measures of the UK’s economic performance were less optimistic. For example, in April the ONS published estimates that showed that “UK labour productivity as Latest news... Regional, sub-regional and local GVA estimates for London, 1997-2014 Current Issues Note 46 This note shows that in 2014, London’s total nominal GVA (as measured by GVA (I) ) was over £364 billion (up 6.8 per cent on 2013), helped by strong growth in real estate (12.8 per cent) and finance and insurance activities (11.6 per cent). Inner London accounts for 68 per cent of London’s GVA, with Inner London – West alone accounting for 42 per cent of the total. Download the full report. 8 6 2 4 2 0 -2 -4 -6 year-on-year % change 2016 Q1 2014 Q3 2013 Q1 2011 Q3 2010 Q1 2008 Q3 2007 Q1 2005 Q3 2004 Q1 2002 Q3 2001 Q1 1999 Q3 1998 Q1 1996 Q3 1995 Q1 1993 Q3 1992 Q1 1990 Q3 1989 Q1 1987 Q3 1986 Q1 1984 Q3 1983 Q1 1981 Q3 1980 Q1 1978 Q3 1977 Q1 -8 1975 Q3 % change on previous quarter measured by output per hour fell by 1.2 per cent from the third to the fourth calendar quarter of 2015 and was some 14 per cent below an extrapolation based on its pre-downturn trend”. They further observed that “in Quarter 4 2015 output per hour fell by 1.2 per cent, the largest quarter on quarter fall since Quarter 4 2008. This decline primarily reflects a sharp quarterly increase in hours worked”. This poor productivity growth may have impacts on both household incomes and government revenue with the Office for Budget Responsibility observing in their March 2016 Economic and fiscal outlook that “lower productivity growth means lower forecasts for labour income and company profits, and thus also for consumer spending and business investment. In aggregate, this reduces tax receipts significantly”. World growth forecast to slow The international economy also remains weak with the International Monetary Fund (IMF) downgrading their expectations for growth in their latest World Economic Outlook, which they published in April. They now forecast world output to increase by 3.2 per cent in 2016 and 3.5 per cent in 2017 (downgrades of 0.2 and 0.1 per cent respectively). Forecasts were downgraded for a number of countries. Thus the US is now forecast to grow by 2.4 per cent this year and 2.5 per cent next year (downgrades of 0.2 per cent on 2016 and 0.1 per cent on 2017), while the Eurozone is forecast to grow by 1.5 per cent this year and 1.6 per cent next year (likewise downgrades of 0.2 and 0.1 per cent respectively). For the UK the IMF now forecasts growth of 1.9 per cent in 2016 (a 0.3 per cent downgrade on their previous forecast) and 2.2 per cent in 2017 (unchanged on their previous forecast). The IMF also warned in April in their latest Financial Stability Report that there is a “growing concern about a mutually reinforcing dynamic of weak growth and low inflation that could produce sustained economic and financial weakness”. More widely there was further evidence of a slowdown, although continued growth, in China’s economy with data for economic growth in the first quarter of 2016 showing that the economy grew by an annualised rate of 6.7 per cent compared to growth of 6.8 per cent in the final quarter of 2015. And in the United States the minutes from the Federal Reserve’s Federal Open Market Committee’s meeting in March showed that the key factor in their decision not London’s Economy Today | Issue 164 Source: ONS % 1974 Q1 Figure 1: UK GDP Growth Last data point is Q1 2016 to raise US interest rates was the state of the global economy. The minutes thus observed that some members “judged that the headwinds restraining growth and holding down the neutral rate of interest were likely to subside only slowly”. Elsewhere there were signs that the problems in the Eurozone have yet to be fully tackled. It was announced in April that, in order to address concerns about the stability of Italy’s banking system, Italy’s strongest banks, insurers and asset managers had agreed a €5 billion bailout fund, called Atlante, to support weaker lenders should they need it. 3 UK growth forecast downgraded as surveys show success and challenges for London In the UK the economic picture remains mixed. UK car sales hit almost 519,000 in March, their highest monthly figure since 1999 according to Society of Motor Manufacturers and Traders data. While UK consumer price index (CPI) inflation reached 0.5 per cent in March, still well below the Bank of England’s central symmetrical target of 2 per cent but higher than the 0.3 per cent seen in February and its highest level since December 2014 (see Figure 2). 5 4 3 2 1 0 Jul-15 Jul-14 Jan-15 Jul-13 Jan-14 Jul-12 Jan-13 Jul-11 Jan-12 Jul-10 Jan-11 Jul-09 Jan-10 Jul-08 Jan-09 Jul-07 Jan-08 Jul-06 Jan-07 Jul-05 Jan-06 Jul-04 Jan-05 Jul-03 Jan-04 Jul-02 Jan-03 Jul-01 Jan-02 Jul-00 Jan-01 Jul-99 Jan-00 Jul-98 Jan-99 Jul-97 -1 Jan-98 CPI However, the April 2016 update to the Bank of England’s Agents’ summary of business conditions found that “annual output growth had been unchanged on the month. Investment growth intentions had weakened a little, mostly reflecting increased uncertainty”. And on the property market they noted that “housing market activity had risen due to increased purchases of properties by buy-to-let investors ahead of April’s stamp duty changes. In contrast, investor demand for commercial real estate had slowed, particularly in London”. Worries also persist for the growth prospects of the UK economy with not only the IMF reducing their economic forecast recently. Thus the British Chamber of Commerce published their latest forecast for UK economic growth in April in which they now expect growth of 2.2 per cent in 2016 and 2.3 per cent in 2017, compared to a previous forecast of growth of 2.5 per cent in both 2016 and 2017. They observed that “the downgrading of our forecast is due to weaker than previously expected growth across all areas of the economy: manufacturing, services, net exports & household consumption”. Evidence of the continuing pressure on public finances also came to light in April with the ONS publishing London’s Economy Today | Issue 164 Source: ONS 6 % Jan-97 Figure 2: UK annual CPI inflation rate Last data point is March 2016 public sector net borrowing data for 2015/16 showing that annual borrowing stood at £74 billion, £1.8 billion higher than forecast at the time of the March Budget. Also the continuing pressures on the high street were highlighted by BHS going into administration on 25 April threatening their 164 stores in the UK (16 of which are in London) and 11,000 employee jobs. Austin Reed which has four retail outlets in London also went into administration in April. 4 In London the London Chamber of Commerce and Industry Q1 2016 Capital 500 survey found that “domestic demand continued to improve during Q1 2016. On balance, 11 per cent of London businesses reported increased sales, up 2 points on last quarter”. However, “after stabilising the previous quarter, business confidence levels dipped by 7 points, as only 17 per cent of companies, on balance, expected their firm’s performance to improve over the next 12 months - an all-time Capital 500 low, compared to a high of 32 per cent in Q2 2014”. Surveyed firms put the economic outlook at its “lowest recorded level for two years, [as] expectations for the UK and London economy continued to decline”. Still the latest Z/Yen Global Financial Centres Index found that “London remains just ahead of New York to retain the number one position”, adding that along with Singapore and Hong Kong they “remain the four leading global financial centres”. London’s Economy Today | Issue 164 A slowing global economy and increased uncertainty provides challenges to London. Nevertheless, despite these challenges the economic fundamentals in London and indicators of current activity provide room for optimism for London’s economic prospects for the time ahead. Economic indicators Increase in average number of passenger journey The most recent 28-day period covered 7 February 2016 – 5 March 2016. Adjusted for odd days, London’s Underground and buses had 285.4 million passenger journeys; 176.1 million by bus and 109.3 million by Underground. The 12-month moving average of passengers increased to 282.5 million, from 282.2 million in the previous period. The moving average for buses was 179.0 million. The moving average for the Underground was 103.5 million. The methodology used to calculate the number of bus passenger journeys was changed by TfL from 1 April 2007. For a detailed explanation please see LET issue 58 (June 2007). Passenger numbers journeys (millions) adjusted for odd days millions 220 5 200 180 160 140 120 100 80 60 2015/16 2014/15 2013/14 2012/13 2011/12 2010/11 2009/10 2008/09 2007/08 2006/07 2005/06 2004/05 2003/04 2002/03 2001/02 2000/01 1999/00 1998/99 1997/98 1996/97 1995/96 1994/95 1993/94 1992/93 40 London Underground Bus (pre 1 April '07 method) Bus (new method) London Underground moving average Bus moving average (pre 1 April '07 method) Bus moving average (new method) Latest release: April 2016 Next release: May 2016 Source: Transport for London No change in the average annual growth rate of passengers Annual % change in passengers using London Underground and buses adjusted for odd days % 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -6 -8 -10 -12 London Underground Buses Underground plus bus London Underground moving average Buses moving average 2015/16 2014/15 2013/14 2012/13 2011/12 2010/11 2009/10 2008/09 2007/08 2006/07 2005/06 2004/05 2003/04 2002/03 2001/02 2000/01 1999/00 1998/99 1997/98 1996/97 1994/95 Latest release: April 2016 Next release: May 2016 1995/96 The moving average annual rate of growth in passenger journeys remained at -0.3 per cent. The moving average annual rate of growth in bus passenger journey numbers increased to -2.5 per cent from -2.9 per cent in the previous period. The moving average annual rate of growth in Underground passenger journeys decreased to 4.0 per cent from 4.6 per cent in the previous period. LU and buses moving average Source: Transport for London ILO unemployment increases in London ILO unemployment rate all aged 16+, seasonally adjusted % Latest release: April 2016 Next release: May 2016 UK Mar-May 2015 Mar-May 2014 Mar-May 2013 Mar-May 2012 Mar-May 2011 Mar-May 2010 Mar-May 2009 Mar-May 2008 Mar-May 2007 Mar-May 2006 Mar-May 2005 Mar-May 2004 Mar-May 2003 Mar-May 2002 Mar-May 2001 Mar-May 2000 Mar-May 1999 Mar-May 1998 Mar-May 1997 Mar-May 1996 Mar-May 1995 Mar-May 1994 Mar-May 1993 Mar-May 1992 London London’s Economy Today | Issue 164 16 The ILO unemployment rate in London stood at 6.3 14 per cent in the quarter to February 2016, compared 12 to 6.2 per cent in the quarter to November. In the UK, 10 the unemployment rate was 5.1 per cent in the quarter to February 2016, showing no change on the previous 8 quarter. 6 There were 291,000 seasonally adjusted unemployed in 4 London in the quarter to February 2016, an increase of 2 3,000 from the quarter to November 2015. There were 0 1,696,000 seasonally adjusted unemployed in the UK in the quarter to February 2016, an increase of 21,000 from the quarter to November 2015. From LET Issue 154 (June 2015), GLA Economics now Source: Labour Force Survey - Office for National Statistics reports on the ILO unemployment rate. Annual output growth increases in London in Q3 2015 Real GVA growth in London and the rest of the UK year-on-year change % 12 11 London’s annual growth in output increased to 3.1% in Q3 2015 from 2.4% in Q2 2015. Annual output growth in the rest of the UK decreased to 1.7% in Q3 2015 from 2.2% in Q2 2015. In Q3 2015, London’s annual output growth was higher than in the rest of the UK. 9 8 7 6 5 4 6 3 2 1 0 -1 -2 -3 -4 -5 -6 -7 -8 London 2015 q1 2014 q1 2013 q1 2012 q1 2011 q1 2010 q1 2009 q1 2008 q1 2007 q1 2006 q1 2005 q1 2004 q1 2003 q1 2002 q1 2001 q1 2000 q1 1999 q1 -9 1998 q1 Latest release: March 2016 Next release: June 2016 10 Rest of the UK Source: Experian Economics Annual employment growth slows in London in Q3 2015 Annual house price inflation in London slows in Q1 2016 House prices, as measured by Nationwide, were lower in Q1 2016 than in Q4 2015 for London, but were higher in the rest of the UK. Annual house price inflation in London was 11.5 per cent in Q1 2016, down from 12.2 per cent in Q4 2015. Annual house price inflation in the UK was 5.3 per cent in Q1 2016, up from 4.3 per cent in Q4 2015. Latest release: April 2016 Next release: May 2016 5 4 3 2 1 0 -1 -2 -3 London 2015 q1 2014 q1 2013 q1 2012 q1 2011 q1 2010 q1 2009 q1 2008 q1 2007 q1 2006 q1 2005 q1 2004 q1 2003 q1 2002 q1 2001 q1 2000 q1 1999 q1 1998 q1 -4 Rest of the UK Source: Experian Economics House prices, UK and London year-on-year growth from quarterly figures, seasonally adjusted data % 40 35 30 25 20 15 10 5 0 -5 -10 -15 -20 London UK Source: Nationwide London’s Economy Today | Issue 164 Latest release: March 2016 Next release: July 2016 % 1989 q1 1989 q3 1990 q1 1990 q3 1991 q1 1991 q3 1992 q1 1992 q3 1993 q1 1993 q3 1994 q1 1994 q3 1995 q1 1995 q3 1996 q1 1996 q3 1997 q1 1997 q3 1998 q1 1998 q3 1999 q1 1999 q3 2000 q1 2000 q3 2001 q1 2001 q3 2002 q1 2002 q3 2003 q1 2003 q3 2004 q1 2004 q3 2005 q1 2005 q3 2006 q1 2006 q3 2007 q1 2007 q3 2008 q1 2008 q3 2009 q1 2009 q3 2010 q1 2010 q3 2011 q1 2011 q3 2012 q1 2012 q3 2013 q1 2013 q3 2014 q1 2014 q3 2015 q1 2015 q3 2016 q1 London’s annual employment growth decreased to 2.0% in Q3 2015 from a downwardly revised 2.2% in Q2 2015. Annual employment growth in the rest of the UK decreased to 0.5% in Q3 2015 from a downwardly revised 0.7% in Q2 2015. In Q3 2015, London’s annual employment growth was higher than in the rest of the UK as a whole. Full-time equivalent employment in London and the rest of the UK year-on-year growth from quarterly figures London’s business activity continues to increase Business activity in London seasonally adjusted index (50 indicates no change on previous month) index 70 Firms in London increased their output of goods and services in March 2016. The Purchasing Managers’ Index (PMI) of business activity recorded 54.2 in March 2016, up from 52.2 in February 2016. An index above 50 indicates an increase in business activity from the previous month. 7 60 55 50 45 Jan-97 May-97 Sep-97 Jan-98 May-98 Sep-98 Jan-99 May-99 Sep-99 Jan-00 May-00 Sep-00 Jan-01 May-01 Sep-01 Jan-02 May-02 Sep-02 Jan-03 May-03 Sep-03 Jan-04 May-04 Sep-04 Jan-05 May-05 Sep-05 Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 Latest release: April 2016 Next release: May 2016 65 40 London Source: Markit Economics New orders in London seasonally adjusted index (50 indicates no change on previous month) index New orders in London rising 70 March 2016 saw an increase in new orders for London firms. The PMI for new orders recorded 53.8 in March 2016 compared to 54.7 in February 2016. An index above 50 indicates an increase in new orders from the previous month. 65 60 55 50 45 40 35 Jan-97 May-97 Sep-97 Jan-98 May-98 Sep-98 Jan-99 May-99 Sep-99 Jan-00 May-00 Sep-00 Jan-01 May-01 Sep-01 Jan-02 May-02 Sep-02 Jan-03 May-03 Sep-03 Jan-04 May-04 Sep-04 Jan-05 May-05 Sep-05 Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 Latest release: April 2016 Next release: May 2016 London Source: Markit Economics Level of employment in London seasonally adjusted index (50 indicates no change on previous month) index The PMI shows that the level of employment in London firms increased in March 2016. The PMI for the level of employment was 54.6 in March 2016, up from 54.4 in February 2016. An index above 50 indicates an increase in the level of employment from the previous month. 60 55 50 45 40 35 Jan-97 May-97 Sep-97 Jan-98 May-98 Sep-98 Jan-99 May-99 Sep-99 Jan-00 May-00 Sep-00 Jan-01 May-01 Sep-01 Jan-02 May-02 Sep-02 Jan-03 May-03 Sep-03 Jan-04 May-04 Sep-04 Jan-05 May-05 Sep-05 Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 Latest release: April 2016 Next release: May 2016 65 London Source: Markit Economics London’s Economy Today | Issue 164 Businesses report higher employment in March Surveyors report that house prices are increasing in London RICS Housing Market Survey prices in previous three months; net balance in London and in England and Wales; seasonally adjusted data 100 The RICS Residential Market Survey showed a positive net balance of -8 for London house prices over the three months to March 2016. Surveyors reported a positive net house price balance of 42 for England and Wales over the three months to March 2016. London’s net house price balance is lower than that of England and Wales. 80 60 40 20 0 8 -20 -40 -60 -80 Jan-00 Apr-00 Jul-00 Oct-00 Jan-01 Apr-01 Jul-01 Oct-01 Jan-02 Apr-02 Jul-02 Oct-02 Jan-03 Apr-03 Jul-03 Oct-03 Jan-04 Apr-04 Jul-04 Oct-04 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 -100 Latest release: April 2016 Next release: May 2016 London England and Wales Source: Royal Institution of Chartered Surveyors Surveyors expect house prices to fall in London and to rise in England and Wales 100 80 60 40 20 0 -20 -40 -60 -80 -100 Jan-00 Apr-00 Jul-00 Oct-00 Jan-01 Apr-01 Jul-01 Oct-01 Jan-02 Apr-02 Jul-02 Oct-02 Jan-03 Apr-03 Jul-03 Oct-03 Jan-04 Apr-04 Jul-04 Oct-04 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Latest release: April 2016 Next release: May 2016 London Consumer confidence positive in London and neutral in the UK 30 20 10 0 -10 -20 -30 -40 Greater London Oct-15 Feb-16 Jun-15 Oct-14 Feb-15 Jun-14 Oct-13 Feb-14 Jun-13 Oct-12 Feb-13 Jun-12 Oct-11 Feb-12 Jun-11 Oct-10 Feb-11 Jun-10 Oct-09 Feb-10 Jun-09 Oct-08 Jun-08 Oct-07 Feb-08 Jun-07 Oct-06 Feb-07 Jun-06 Oct-05 Feb-06 Jun-05 -50 UK Source: GfK NOP on behalf of the European Commission London’s Economy Today | Issue 164 Latest release: March 2016 Next release: April 2016 Consumer confidence barometer score Feb-05 The GfK index of consumer confidence reflects people’s views on their financial position and the general economic situation over the past year, as well as their expectations for the next 12 months (including whether now is a good time to make major purchases). A score below zero signifies negative views of the economy. For Greater London, the consumer confidence score stood at 9 in March 2016, down from 18 in February 2016. For the UK, the consumer confidence score remained at 0 in March 2016, holding constant from 0 in February 2016. England and Wales Source: Royal Institution of Chartered Surveyors Feb-09 The RICS Residential Market Survey shows that surveyors expect house prices to fall over the next three months in London; and to rise in England and Wales. The net house price expectations balance in London was -38 in March 2016. For England and Wales, the net house price expectations balance was 17 in March 2016. RICS Housing Market Survey house price expectations; net balance in London, and in England and Wales; seasonally adjusted data Socio-economic baseline – Old Oak and Park Royal By Adam van Lohuizen, Economist The Old Oak and Park Royal Development Corporation (OPDC) was created on 1 April 2015. The OPDC will redevelop the Old Oak and Park Royal area west London, the location where rail infrastructure projects HS2 and Crossrail will meet. The development is expected to deliver 25,500 new homes and create 65,000 new jobs over the next 30 years. 9 GLA Economics has recently1 analysed a variety of socio-economic and demographic indicators to create a baseline against which the impacts of the Old Oak and Park Royal regeneration project can be measured over time. This baseline will be used as a reference point in future years to measure changes in these indicators to assess the impact that the regeneration project is having on the Old Oak and Park Royal area. Old Oak and Park Royal is an area of concentrated commercial activity. The development zone itself, currently has a low number of residents and largely represents business activity and infrastructure. For those that do live in the area, generally the socio-economic measures show that when compared to Greater London, the area is disadvantaged across a number of different indicators. Some of this performance can be attributed, at least in part, to the population of the area being younger than the overall London population, with residents up to the age of 30 accounting for 5.3 per cent more of the population when compared to London as a whole. Since 2007, population growth in the area has generally been stronger than overall London population growth (Figure A1). The population density of the area is quite low, which can be attributed to the small amount of residential land and the prominence of commercial land in the area. Source: GLA Datasore from the ONS 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% -1.0% 2003 2004 2005 2006 2007 OPDC Area 2008 2009 OPDC Region 2010 2011 2012 2013 2014 Greater London 1 Van Lohuizen, A., March 2016, ‘Working Paper 74: Socio-economic baseline – Old Oak and Park Royal’, GLA Economics. London’s Economy Today | Issue 164 Figure A1: Population growth, 2003 – 2014 Compared to Greater London, the community within the area has a larger share of Black / African / Caribbean / Black British ethnic groups and a lower proportion of white residents. Owner occupation rates are less common than across London, with a larger share of households living in social housing relative to London. This could at least be in part due to the younger age profile of the area. The average household size is slightly larger than the London average, with households also more likely to be overcrowded, which can be attributed to the lower share of households that are owner-occupiers (where overcrowding is less common), and higher rates of overcrowding in the private rented sector (Figure A2). Source: 2011 Census 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% Owner-Occupiers Social Rented OPDC Area OPDC Region Private Rented London The housing stock has a greater share of flats and terraced houses than across London, while median house prices are currently lower than in the surrounding boroughs. New house building has been taking place within the boundaries of the Old Oak Park Royal development zone over the past year, with 161 new homes completed for the year, 85 per cent of which were for social rent or shared ownership. Household incomes in the area are lower by around one-quarter when compared to London-wide incomes despite having experienced similar growth in incomes since the economic downturn. This is consistent with lower rates of economic activity and higher rates of unemployment across most different demographic groups that live in the area. Long-term unemployment is also more common, resulting in a higher share of the population claiming benefits through Job Seekers Allowance or Universal Credit. Levels of education tend to be below London averages in terms of both results for students still in school, and the level of qualifications that have been obtained for the working-age population. The health of the community London’s Economy Today | Issue 164 Figure A2: Share of households with insufficient bedrooms, by tenure, 2011 Census 10 Figure A3: Median household income 2012/13 Source: 011 Census 11 in the area is also below London average levels, with the rates of disability or long-term illness, and childhood obesity higher than London averages. Life expectancy in the area was also lower, while the average rate of deprivation in the area places it in the most deprived 20 per cent of areas in London. GLA Economics has estimated that the area generated £2.58 billion worth of economic activity in 2012, predominantly driven by industries, such as information and communication, wholesale and retail trade, and manufacturing. There are over 52,000 people employed in this commercial area with them being employed by 2,250 different enterprises. Wholesale and retail trade and manufacturing industries were the largest in the area in terms of the number of people employed. If you would like to know more about the socio-economic characteristics of the Old Oak and Park Royal area, please download Working Paper 74 from our website. London’s Economy Today | Issue 164 There is greater access to transport in the area when compared to the average across London, which is likely due to the number of tube stations in the area, with journeys into the area on the tube or overground more common than journeys leaving the area. Usual residents are less likely to have access to a vehicle, while on a per capita basis road accidents are more common than at the wider London level, but this is at least in part due to the low population density and commercial nature of the area. Over a third of land within the Old Oak Park Royal development zone is designated for manufacturing use alone. Additional information Data sources Tube and bus ridership Transport for London on 020 7222 5600 or email: [email protected] GVA growthExperian Economics on 020 7746 8260 Unemployment rates www.statistics.gov.uk 12 Glossary Acronyms BCC BRES CAA CBI CLG GDP GVA ILO British Chamber of Commerce Business Register and Employment Survey Civil Aviation Authority Confederation of British Industry Communities and Local Government Gross domestic product Gross value added International Labour Organisation IMF International Monetary Fund LCCI London Chamber of Commerce and Industry LET London’s Economy Today MPC Monetary Policy Committee ONS Office for National Statistics PMI Purchasing Managers’ Index PWCPricewaterhouseCoopers RICS Royal Institution of Chartered Surveyors London’s Economy Today | Issue 164 Civilian workforce jobs Measures jobs at the workplace rather than where workers live. This indicator captures total employment in the London economy, including commuters. Claimant count unemployment Unemployment based on the number of people claiming unemployment benefits. Employee jobs Civilian jobs, including employees paid by employers running a PAYE scheme. Government employees and people on training schemes are included if they have a contract of employment. Armed forces are excluded. Gross domestic product (GDP) A measure of the total economic activity in the economy. Gross value added (GVA) Used in the estimation of GDP. The link between GVA and GDP is that GVA plus taxes on products minus subsidies on products is equal to GDP. Tube ridership Transport for London’s measure of the number of passengers using London Underground in a given period. There are 13 periods in a year. In 2015/16 there are eleven 28-day periods, one 26-day period and one 32-day period. Period 1 started on 1 April 2015. Bus ridership Transport for London’s measure of the number of passengers using buses in London in a given period. There are 13 periods in a year. In 2015/16 there are eleven 28-day periods, one 26-day period and one 32-day period. Period 1 started on 1 April 2015. GLA Economics City Hall The Queen’s Walk London SE1 2AA Tel 020 7983 4922 Email [email protected] Fax 020 7983 4674Internet www.london.gov.uk © Greater London Authority April 2016 ISSN 1740-9136 (print) ISSN 1740-9195 (online) ISSN 1740-9144 (email) London’s Economy Today is published by email and on www.london.gov.uk towards the end of every month. It provides an overview of the current state of the London economy, and a selection of the most up-to-date data available. It tracks cyclical economic conditions to ensure they are not moving outside the parameters of the underlying assumptions of the GLA group. Subscribe Subscribe online at http://www.london.gov.uk/webform/gla-intelligence-news-email Disclaimer GLA Economics uses a wide range of information and data sourced from third party suppliers within its analysis and reports. GLA Economics cannot be held responsible for the accuracy or timeliness of this information and data. GLA Economics, Transport for London and the Greater London Authority will not be liable for any losses suffered or liabilities incurred by a party as a result of that party relying in any way on the information contained in this publication. Other formats For a summary of this document in your language, or a large print, Braille, disc, sign language video or audio tape version, please contact us at the address below: Public Liaison Unit Greater London Authority Tel 020 7983 4100 City HallMinicom 020 7983 4458 The Queen’s Walk www.london.gov.uk London SE1 2AA Please provide your name, postal address and state the publication and format you require. About GLA Economics GLA Economics provides expert advice and analysis on London’s economy and the economic issues facing the capital. Data and analysis from GLA Economics provide a sound basis for the policy and investment decisions facing the Mayor of London and the GLA group. The unit was set up in May 2002.