Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

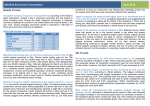

Monthly Economic Commentary: vote for Brexit increases uncertainty Global Trends Brexit has created significant uncertainty, and the IMF believes this is likely to dampen growth in the near-term, particularly in the UK, but also in Europe and the rest of the global economy. Prolonged periods of uncertainty and associated declines in consumer and business confidence could mean lower growth and the IMF will assess the impact of this in its World Economic Outlook Update later this month. The US, the world’s largest economy, faces a period of uncertainty according to the US Federal Reserve Bank (the Fed). A UK exit from the EU is unlikely to send the US economy into recession, but could result in a "flight to safety" by investors that could push up the value of the dollar, affecting the competitiveness of exports. Business investment and industrial production have already been constrained by global headwinds and depressed oil and gas activity. Although US manufacturers reported a rise in production in June, growth was still relatively subdued, which contributed to cautious job hiring and reductions in inventories. Exports and new orders increased but manufacturers are struggling with a strong dollar and decline in the energy sector. The US is one of Scotland’s main export markets so a strong dollar will make our exports more competitive. Manufacturing output in China, the world’s second largest economy, fell at the fastest rate in four months in June. The latest business survey results attributed this to poor market conditions and a drop in orders for new work. Weaker demand and a fall in new export sales (for the seventh month in a row) led manufacturers to cut output. With drivers of growth such as exports and investment subdued, policymakers are relying on continued stimulus to achieve their growth targets. Authorities injected $1 trillion of new credit into the economy in Q1 but there are calls for even more stimulus. A strong yen and a sluggish economy are likely to lead to further monetary easing in Japan, the world’s third largest economy. Survey results show that business conditions for Japanese manufacturers worsened at the end of Q2 2016. Production declined for the fourth month running, led by a drop in new orders. A key driver was a marked drop in export demand. Evidence suggests that appreciation of the yen against the dollar reduced Japan’s global competitiveness, leading to a decline in trade volumes. July 2016 The UK’s exit from the EU could curb growth in the eurozone by between 0.3% and 0.5% over the next three years according to the European Central Bank (ECB). The latest business survey results suggest Q2 growth is at the lowest level since the final quarter of 2014. Faster growth in manufacturing was offset by a slowdown in the service sector in June, where growth was the weakest for 18 months. Going forward, uncertainty caused by the prospect of Brexit may affect business and consumer spending, dampening growth in the short term. As the EU is Scotland’s biggest export market a fall in demand would be bad news for our exporters, although this may be partially offset by the weakness of the sterling, which makes our exports more competitive. The IMF is reporting medium-term growth prospects for the eurozone as mediocre, with crisis legacies of high unemployment, elevated public and private debt, and deep-rooted structural weaknesses weighing on the outlook. It has cut its economic growth forecasts for the bloc in the wake of the UK's vote to leave the EU to 1.6% this year and 1.4% in 2017. Before the referendum the IMF had predicted growth of 1.7% for both years. Growth five-years ahead is expected to be about 1.5%. UK Trends The Bank of England (BoE) highlights subdued growth in the global economy, including the euro area, which could be exacerbated by a prolonged period of heightened uncertainty following the referendum as a near-term risk to the UK economy. It eased capital requirements for banks to increase their capacity to lend to UK households and businesses. This change will last until at least June 2017 and could help liquidity if uncertainty from the leave vote causes the economy to slow down and banks to be more cautious. The BoE expects some market volatility during the period of uncertainty and adjustment following the result of the referendum. This has been evident in financial markets where prices have moved sharply. Between 23 June and 1 July, the sterling exchange rate index fell by 9%. However, the weaker currency should give exports a boost in the coming months. Total production output is estimated to have increased by 1.6% over the year to April 2016, according to official statistics. The biggest contribution came from manufacturing (the largest component of the production sector), which increased by 0.8%. The remaining three sub sectors of mining & Monthly Economic Commentary: vote for Brexit increases uncertainty quarrying, electricity, gas, steam & air conditioning and water & waste management also grew (by 0.3%, 6.2% and 5.5% respectively). Within manufacturing, pharmaceuticals increased by 12.5%, the largest rise since April 2009. More recent UK manufacturing data also suggests growing activity. Business survey results show that new orders in June increased at the fastest pace since last October, reflecting the ongoing strength of the domestic market and a marginal increase in export business. Growth in overseas orders were linked to the US, Europe, Russia and East Asia. Whether recent growth can be sustained will depend on whether any negative impact from uncertainty can be partly offset by a boost to exports resulting from a fall in the value of the pound. Uncertainty linked with the referendum was reported to have weighed on service sector activity, and growth over the second quarter was the weakest since the first quarter of 2013. Business confidence fell to the lowest level in 4-and-a-half years in June according to the Lloyds Business Barometer survey. The survey was conducted in the week after the referendum and one month’s results should be interpreted with care, but the results could indicate weakening in the near-term economic outlook. While confidence and margins declined overall, they held up well in the industrial sector, possibly due to the recent fall in the value of the pound. Small business confidence fell in Q2 2016 according to the latest Federation of Small Business Index. Confidence has been on a downward trend since Q2 2015 and the latest year-on-year decline is the largest on record. Although credit conditions have continued to improve, investment intentions have fallen sharply. Small businesses are reducing headcount and there has been a significant increase in the proportion citing labour costs as a main cause of rising business costs, with the National Living Wage and ongoing roll-out of auto-enrolment both contributing to higher employment costs. The UK unemployment rate fell to 5% in the three months to April, the lowest since October 2005, according to the latest official figures. The employment rate remains at a record high of 74.2% and youth unemployment (16 to 24 year olds) was 13.6%, down from 16.0% a year earlier and at its lowest rate since 2005. Over the year, there were 304,000 more people in full-time and 157,000 more in part-time employment. July 2016 Scottish Trends The Fraser of Allander Institute revised its growth forecasts for Scotland down for 2016, 2017 and 2018, to 1.4%, 1.9% and 2% respectively; significant downward revisions to 2016 and 2017 compared to the Institute’s March 2016 forecasts. Output and jobs growth have both weakened since the last forecast; labour market data show a large deterioration as job losses associated with both the falling oil price and deteriorating export performance impact on companies. Growth is increasingly dependent on weakened domestic demand; overseas demand for Scottish goods and services is faltering. Scotland’s economic growth in 2016 is predicted to be the slowest since 2012. The Ernst & Young Scottish ITEM Club has downgraded its GDP growth forecast for 2016 to 1.2% (0.6 percentage points lower than they forecast six months ago). Scotland now faces a third consecutive year of slowing GDP growth, partly as a consequence of the oil price slump but also underperformance in the service sector, with many areas of services performing poorly compared to the UK. However, the negative impact of the oil-price fall on growth is expected to fade in 2017 when the Club’s growth forecast is 2%. The Scottish private sector returned to growth in June following two months of stagnation according to the latest Bank of Scotland PMI report. This was driven by a slight rise in new business, which was broad-based across both manufacturers and service providers. Output in services was broadly unchanged compared to May; manufacturing output increased at the fastest rate in almost a year driven by the domestic market as new export orders declined for the 17th consecutive month. Input prices also rose further, reflecting unfavourable exchange rate movements according to anecdotal evidence, but competitive pressures resulted in some companies reducing their output prices. Optimism is returning to Scottish businesses and the slowdown seems to be coming to an end according to the results of the latest Royal Bank of Scotland Business Monitor, which was released just before the referendum. Modest growth is predicted for the remainder of 2016. Although the total volume of business fell during the last quarter (31% reported volumes fell and 30% reported an increase) the -1% difference compares to -18% in Q1 2016 (when 39% reported a fall and 21% an increase). However, there is still some cause for concern in some areas: regions with strong oil & gas and agriculture sectors struggled and exports have been challenging for all businesses. The export balance has now been negative for five consecutive quarters. Monthly Economic Commentary: vote for Brexit increases uncertainty In small businesses on the other hand, confidence declined further in Scotland in Q2 2016 according to the Federation of Small Businesses latest index. Confidence has now been low for the past year, reflecting slow Scottish economic growth. The results suggest that small businesses in Scotland expect conditions to deteriorate further over the next quarter. In addition to the difficulties being experienced in the manufacturing and oil & gas sectors, higher rates of unemployment than in the rest of the UK are weighing on household spending power and domestic demand for goods and services. Unemployment in Scotland fell by 11,000 in the three months to April, resulting in a 0.3 percentage point drop in the unemployment rate to 5.8% (compared to 5% in the UK). However, employment also fell (by 48,000 in total of which 35,000 were men and 13,000 were women) and the employment rate is now 73.2% (below the UK average of 74.2%). The number of working age economically inactive people (not in work and neither seeking nor available to work) increased by 54,000 over the quarter (26,000 men (+9.3%) and 28,000 women (+6.5%)). In the year to December 2015, the group with biggest increase in the number of economically inactive was 25-49 year old men (up by 13,000). Potential impacts on the economy of Brexit Channels through which financial market volatility and heightened economic uncertainty may feed through to the wider economy have been highlighted in the Scottish Government Monthly Economic Brief for June: Uncertainty over the economic outlook can reduce consumer confidence and in turn lead to consumers deferring spending Businesses may delay investment and recruitment decisions if there is uncertainty about the future economic and regulatory landscape. Likewise, if banks react to uncertainty by reassessing their risk exposure, this can reduce companies’ access to finance A fall in the value of Sterling, if sustained, can increase the cost of imports, and may reduce households’ real incomes and companies’ profitability. A fall in Sterling may also have some positive impacts as it will make UK exports more competitive If the above channels fed through to a slowdown in economic activity, this can have a detrimental impact on Public Finances July 2016 Summary of Headline Indicators Indicator Scotland Change on year UK GDP growth (Q4 2015) 0.9% 2.1% Manufactured Export growth (Q4 2015) 0.6% 5.2% Employment rate (Feb – April 2016) 73.2% 74.2% Unemployment rate (Feb – April 2016) 5.8% = Change on year 5.0% International Activity and Performance of SE Account Managed Companies The majority of Scottish Enterprise Account Managed (AM) companies (65%) are exporters. Over the October 2015 to March 2016 period, 50% of exporting companies reported that export levels had increased over the previous six months and 17% reported a decline. 85% of exporters are actively exporting to Europe, and 60% to North America. Almost half are selling to markets in Asia. 60% of exporters stated their most important overseas market was Europe, followed by North America (25%). Monthly Economic Commentary: vote for Brexit increases uncertainty Implications for Scottish Enterprise Scotland’s economic growth was already slowing before the referendum result, buffeted by external factors such as the weak oil price and challenging global trade environment. The impact of these effects could be exacerbated by market volatility and uncertainty in the near-term following the Brexit vote. Weaker Sterling may help to offset current slow growth rates in key export areas but will push up the cost of imported inputs. Falling business optimism and confidence indicate that ongoing trading conditions will remain challenging for Scottish businesses. Improving competitiveness, particularly through increased productivity levels, will be a key factor for Scottish firms to compete at home and overseas through a focus on innovation, investment, entering new markets and developing higher workforce skills. Strategy & Sectors July 2016 _______________________________________________________ This commentary reflects our understanding of issues at the time of writing and should not be taken as Scottish Enterprise policy. If you have any comments or suggestions for improvement, please email Jennifer Turnbull ([email protected]) or phone 01786 452010. July 2016