Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

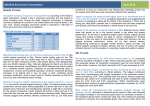

Monthly Economic Commentary: Global growth downgraded April 2016 Global Trends Global economic growth forecast for 2016 is downgraded to 3.2% by the IMF. This is 0.2 percentage points lower than the IMF’s forecast in January, and suggests that growth this year will be virtually the same as in 2015. It is the second time this year that the IMF has downgraded its 2016 forecast. The IMF cites the slowdown and rebalancing in China; a further decline in commodity prices, especially for oil, affecting commodity producing countries; a related slowdown in global investment and trade; and declining capital flows to emerging market and developing economies as factors weighing down on the global outlook. In addition, the IMF highlights a number of noneconomic factors (such as geopolitical conflicts, political discord, terrorism and refugee flows) that are affecting confidence. The recovery is projected to strengthen in 2017. IMF GDP Growth Forecasts (%) 2015 Global 3.1 United States 2.4 Euro Area 1.6 China 6.9 Japan 0.5 United Kingdom 2.2 2016 3.2 2.4 1.5 6.5 0.5 1.9 2017 3.5 2.5 1.6 6.2 -0.1 2.2 Source: IMF World Economic Outlook, April 2016 International trade is forecast to grow by just 2.8% this year. The World Trade Organisation (WTO) expects the volume of international trade to be the same as in 2015, the fifth consecutive year of trade growth below 3%, and below the average of 5.0% since 1990. Weakness in emerging market imports has been a key factor in holding back world trade growth over the last year. Downside risks to the forecast include increasing financial market volatility and a sharper than expected slowdown in the Chinese economy, although the WTO highlights that trade levels could increase if the European Central Bank succeeds in generating faster growth in the euro area. Minutes of the US Federal Reserve's March meeting re-ignited concerns about global growth, resulting in stock market falls and sliding oil prices. Fed members feared a slowdown could make it difficult to achieve employment and inflation targets, so left interest rates unchanged. Economic data for the US (the world’s largest economy) are fairly muted. The economy is still creating jobs (employment increased by 215,000 in March), but the unemployment rate rose unexpectedly to 5% from 4.9% the previous month. Business survey data for March show growth remained subdued in manufacturing, although new export orders stabilised following a slight fall in February. Service sector output also increased after a slight decline the previous month. Generally, domestic activity is upbeat, although restrained by weak global growth and a strong dollar affecting exports. The US is one of Scotland’s main export markets and the strong dollar and relative weakness of sterling will make our exports more competitive. China’s economy (the world’s second largest) grew by 6.7% (annualised) in the first quarter of the year, its slowest rate since 2009, but above the government’s 6.5% target. Imports fell by 14.2% in 2015 according to figures from the WTO, contributing to low growth in the volume of world trade. Trade figures for March show exports beat expectations (up 18.7% on the same period last year) but imports declined by 1.7% compared to last year. Latest business survey results show that activity in the manufacturing sector expanded in March for the first time in nine months. Over the quarter, however, the index was the lowest recorded since early 2013. In Japan, manufacturing activity contracted at the fastest pace in more than three years in March. Business survey results show that new export orders shrank sharply, adding to fears the world’s third-largest economy is sliding back into recession. Despite the introduction of negative interest rates by the central bank to boost lending and investment and to keep the value of yen low to boost exports, the currency has surged, due to the yen’s traditional position as a safe haven when there are concerns about the global economy. Japan is the world’s only advanced economy that the IMF is forecasting will shrink in 2017, mainly as a consequence of the impact of a planned consumption tax increase The strength of domestic spending in the eurozone is driving demand for imports. This is good news as the zone is Scotland’s biggest overseas market. Business survey results show the rate of expansion improved for the first time in three months in March. The growth rate was higher in manufacturing, despite new export growth slowing to a 14-month low, than in services so it is likely the bloc’s economy will have continued slow growth in the first quarter of 2016 given the dominance of services in GDP. Monthly Economic Commentary: Global growth downgraded April 2016 UK Trends Growth in the UK economy may have slowed further in the first quarter of 2016. The Index of Production is one of the earliest indicators of growth, and both production and manufacturing (the main component of production) indices have been generally declining since October 2015. The British Chambers of Commerce expect slower economic growth in Q1. Results from their Quarterly Economic Survey, showed that most key survey indicators (such as sales, orders, business confidence and investment intentions) were either static or decreasing over the first three months of the year. Overall, the figures for both services and manufacturing indicate continued growth, but domestic sales and orders reached their lowest level for over three years in the service sector and domestic sales declined again in manufacturing. Confidence in turnover and profitability is still historically low in both sectors. The Purchasing Manager Index (PMI) business survey tells a similar story. Growth in manufacturing remained subdued in March (unchanged from February’s seven-month low). Output of consumer products increased following a decline in February, but investment goods output continued to slow and levels of export business fell for the third consecutive month due to softer global demand. Overall, Q1 registered one of its weakest manufacturing growth performances over the past three years. In services, output growth was the weakest since Q1 2013, although activity increased at a faster rate in March than the previous month. The surveys suggest growth of 0.4% for the UK economy as a whole in Q1, lower than the 0.6% achieved in Q4 2015. Consumer prices inflation (CPI) reached 0.5% in the 12 months to March, up from 0.3% in February, a bigger increase than analysts had expected. The jump was mainly due to rises in air fares, influenced by an early Easter, and clothing and footwear prices. Although the increase strengthened the value of sterling, CPI is still well below the Bank of England 2% inflation target, making interest rates rises unlikely this year. Productivity performance in the UK has been poor since the recession and the latest statistics show the worst decline in output per hour since the financial crisis. The Office for National Statistics estimates productivity is currently 14% below pre-crisis trends after falling by 1.2% between the third and fourth quarters of 2015. Output increased by only 0.6% while hours worked increased by 1.7%. There was some improvement in service sector productivity, which increased by 1.1% over the quarter; however, it declined by 3.4% in manufacturing. The UK employment rate for the three months to January was 74.1%, the joint highest since comparable records began in 1971. 479,000 more people had jobs than the same period last year: nearly two thirds of these were fulltime. The number of unemployed people fell over the quarter leading to an unemployment rate of 5.1%. Scottish Trends The Scottish economy grew by 0.2% during the final quarter of 2015 (compared to growth of 0.6% in the UK). The service sector grew by 0.3%, production fell by 0.1% (driven by declines in mining, quarrying and utilities), and the construction sector grew by 0.1%. GDP growth for 2015 was +1.9%, lower than the UK rate of +2.3%. Scottish growth almost stalled in the second and fourth quarters of 2015, and was negative in the third quarter. More recent business survey data suggest the Scottish economy slowed further during the first quarter of 2016. The latest Bank of Scotland PMI survey reported deteriorating business conditions in Scotland’s private sector in March as the headline activity figure fell into negative territory. The volume of new business fell for the second successive month, driven by the sustained downturn in the oil & gas industry. Manufacturing fared worse than services, where the decline in business activity was more muted. The Royal Bank of Scotland Business Monitor also reported slowing growth in the first quarter of this year. In the three months ending February 2016, sales, business activity, new business volumes and investment all weakened. According to the research, firms across Scotland are reporting falling exports: only one in six reported an increase in export activity. The main cause of slowing growth seems to be the weakening oil price since businesses surveyed in the North East reported weaker performance. More positively, firms expect a rebound in growth in the next six months. Monthly Economic Commentary: Global growth downgraded Business conditions are still subdued with little change from 2015 according to Scottish Engineering’s Quarterly Review for Q1 2016. Order intakes and output volumes are still negative (i.e. more firms are reporting a decline than are reporting an increase) and optimism throughout the industry is still not improving. Economic indicators from the Scottish Chamber of Commerce quarterly report show business performance varied by sector in the first quarter of 2016. Construction performed strongly for new contracts, sales revenue and profitability, and expectations for the future are positive; while manufacturing declined, but expects to recover over the next few months. Financial & business services has been performing poorly since the second quarter of last year, but oil and gas businesses within the financial & business services sector are continuing to report weak performance while non-oil and gas businesses are reporting positive trends. Scottish export volumes fell 1.5% during the fourth quarter of 2015. The biggest contributions to the decline were Food & Drink (-4.9%) and Engineering (-1.8%) - which together account for almost 62% of international manufactured exports from Scotland. On an annual basis (comparing the most recent four quarters to the previous four) exports grew by 0.6%. Manufactured export volumes are now around 3.0% below their pre-recession peak in 2007, although 17% above their trough in 2009. The number of people in employment in Scotland went up by 17,000 in the three months to January. Over the quarter the employment rate increased by 0.1 percentage points to 74.5% (compared to 74.1% in the UK). The number of people out of work, however, also rose (+16,000) pushing the unemployment rate up by 0.5 percentage points to 6.1% (compared to a UK rate of 5.1%). Youth unemployment went up by 5,000 compared to the same period last year and the youth unemployment rate increased by 0.4 percentage points to 15.7% (compared to a 2.4 percentage point fall to 13.7% in the UK). April 2016 Summary of Headline Indicators Indicator Scotland Change on year UK GDP growth (Q4 2015) 0.9% 2.1% Manufactured Export growth (Q4 2015) 0.6% 5.2% Employment rate (Nov – Jan 2016) 74.5% 74.1% Unemployment rate (Nov – Jan 2016) 6.1% 5.1% Change on year Performance of SE Account Managed Companies Scottish Enterprise regularly seeks feedback from account managed companies on business performance and surveyed 360 companies between January and March 2016. Feedback was generally positive with the majority of companies reporting increases in turnover, profitability, employment and exports over the previous six months. Almost 60% of companies reported an increase in turnover, and 50% of exporting firms reported an increase in overseas sales. Monthly Economic Commentary: Global growth downgraded April 2016 and unemployment higher in Scotland, despite a slightly higher employment rate. The Scottish economy faces a number of headwinds, especially the negative effects from the ongoing low oil prices and knock-on effects on employment and investment in the oil & gas sector and its supply chain, and a weaker outlook for exporters with slowing global growth and an increase in economic uncertainty. Ongoing trading conditions will, therefore, remain challenging for Scottish businesses. Improving competitiveness, particularly through increased productivity levels, will be a key factor for Scottish firms to compete at home and overseas through a focus on innovation, investment, entering new markets and developing higher workforce skills. Looking ahead to the next six months companies are optimistic. Around three quarters of firms expect to increase turnover and profitability. Strategy & Sectors April 2016 _______________________________________________________ This commentary reflects our understanding of issues at the time of writing and should not be taken as Scottish Enterprise policy. If you have any comments or suggestions for improvement, please email Jennifer Turnbull ([email protected]) or phone 01786 452010. Implications for Scottish Enterprise The latest data show that growth in the Scottish economy weakened in 2015 and could continue to slow in 2016. The slowdown in Scotland is consistent with the UK as a whole but seems to be more pronounced as GDP growth is slower