Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

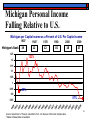

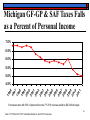

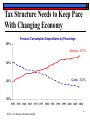

Michigan Economic and Budget Outlook IMA Conference Michigan State University East Lansing, MI October 25, 2010 Mark P. Haas Chief Deputy Treasurer Treasury Responsibilities Tax Administration / Tax and Debt Management Financial Management / Banking Services Local Government Services Financing Higher Education Investing All State Funds Casino Gambling / Lottery Housing Development for Low/Moderate Income 2 Treasury Customers Colleges and Universities Hospitals Public Schools Local Government Units Public Retirees Higher Ed Students Michigan Taxpayers 3 Treasury’s Commitment ● Maintain the State’s financial integrity. ● Fair and consistent administration of tax laws. ● Provide efficient and effective professional services. ● Provide access to financial resources for higher education, K-12, local government, and hospitals. 4 2011 Treasury Budget All Funds $1,975.4 General Fund (GF) $201.4 ($s in millions) Operations Funding A ut hor i t i e s & Ot he r 22. 57% R e v e n u e Sh a r i n g D e b t Se r v i c e 6 . 8 3 % 52. 25% Gr a nt s 6 . 5 0 % Ope r a t i ons 1 1 . 2 0 % Revenue Generation Student Financial Investments Local Government State Banking Revenue Forecasting Bond Finance $139.8 $ 36.9 $ 17.1 $ 15.8 $ 8.6 $ 1.7 $ 1.3 P I LT 0 . 6 6 % $221.3 Authorities, Funds & Commissions Pass Through Funds Revenue Sharing Grants Debt Service Payments in Lieu of Taxes $1,032.1 $ 128.4 $ 134.9 $ 13.0 $1,308.4 Lottery Gaming MSHDA MSF LBFTA $ 26.2 $ 25.3 $ 223.7 $ 168.7 $ 1.9 $445.8 5 Overview ● U.S. and Michigan Economic Outlook ● State and Local Budget Situation ● Federal Fiscal Situation ● What Michigan Needs to Do 6 How Bad was the Recession? 7 2008-2009 Recession Longest Since Great Depression Number of Months from Peak to Trough U.S. Recessions 16 8 10 11 6 8 8 10 A 1 19 945 48 -1 94 19 9 53 -1 95 19 4 57 -1 95 19 8 60 -1 19 961 69 -1 97 19 0 73 -1 97 5 19 37 -1 93 8 8 10 2 vg 20 . P 001 07 os Th tW ru Ju ar ne 09 11 1 19 980 81 -1 98 19 2 90 -1 99 1 13 18 16 Source: NBER 8 2008-2009 Recession GDP Decline Steepest on Record Percent Change, Economy Peak to Trough 0.7% -0.5% -0.2% -1.4% -1.6% -2.2% -2.5% -3.1% -1.7% -2.6% -3.2% -3.7% 1948- 1953- 1957- 1960- 1969- 1973- 1980 1949 1954 1958 1961 1970 1975 1981- 1990- 2001 1982 1991 Source: Bureau of Economic Analysis, U.S. Department of Commerce. Data not avail for 1937-38 and 1945 recessions. Avg. Post War 2007 To 09Q2 9 One for the Record Books Calendar 2009 Estimate and Actual April 2008 2009 Actual Forecast Level Light Vehicle Sales (millions) 15.2 10.4 Housing Starts (million units) 1.131 0.55 US Unemployment Rate 5.8% 9.3% US Payroll Employment (% chg) 0.4% -4.3% US Personal Income (% chg) 3.6% -1.7% Comments Lowest Since 1970 Lowest Back to 1959 Highest Since 1983 Lowest Back to 1940 Lowest Since 1938 Source: April 2008 Global Insight Forecasts and 2009 actuals compiled from various sources by Michigan Department of Treasury. 10 Is the Economy Looking Better? 11 Leading Indicators Show National Recovery Struggling Weekly Leading Index, Smoothed Annual Growth Rate 47.2% 23.6% 0.0% -23.6% 09/10/10 -9.2% 1/ 1/ 20 4/ 07 1/ 20 7/ 07 1/ 20 07 10 /1 /2 00 7 1/ 1/ 20 4/ 08 1/ 20 7/ 08 1/ 20 08 10 /1 /2 00 8 1/ 1/ 20 4/ 09 1/ 20 7/ 09 1/ 20 09 10 /1 /2 00 9 1/ 1/ 20 4/ 10 1/ 20 10 7/ 1/ 20 10 -47.2% Source: Economic Cycle Research Institute. 12 GDP Growth Observed Four Quarters in a Row Real GDP Growth 3.0% Growth 3.5% 2.7% 3.2% 2.1% 2.0% 1.4% 6.9% 5.4% 4.1% 3.6% 3.5% 3.0% 2.9% 2.9% 2.1% 1.6% 1.4% 0.9% 0.1% 0.1% 3.7% 3.0% 3.2% 2.9% 2.3% 3.1% 1.7% 1.6% 5.0% 0.6% -0.7% -0.7% -1.3% -1.1% 3.6% 2.7% 2.3% 1.9% 2.2% 1.6% 1.3% -4.0% 2010Q2 -4.9% -6.8% 2001 Q1 2002 Q1 2003 Q1 2004 Q1 2005 Q1 2006 Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 Figures are annualized percent change from preceding quarter in 2005 chained dollars. Source: Bureau of Economic Analysis. Forecast quarters in red are the September 2010 Global Insight forecast. 13 U.S. Has Gained Over 600,000 Jobs Since December 2009 432 313 208 128 70 64 (10) (33) (50) (149) 14 39 (57) (95) (175) (109) (193) (231) (210) (334) (211) (224) (225) (347) (344) (458) (554) (504) (582) (673) (726) (728) (779) (753) v No 07 n Ja 08 ar M 08 ay M 08 l Ju 08 p Se 08 v No 08 n Ja 09 ar M 09 ay M 09 l Ju Source: U.S. Bureau of Labor Statistics, U.S. Department of Labor 09 p Se 09 v No 09 n Ja 0 -1 ar M 0 -1 0 -1 ay M l Ju 0 -1 10 pe S 14 Stock Market Moving Sideways S&P 500 Closing Level 1565 10/09/07 1600 1400 1125 09/16/10 1200 1000 800 677 03/09/09 Source: freelunch.com, reuters.com 20 10 1/ 1/ 20 09 1/ 1/ 20 08 1/ 1/ 20 07 1/ 1/ 20 06 1/ 1/ 20 05 1/ 1/ 20 04 1/ 1/ 20 03 1/ 1/ 20 02 1/ 1/ 20 01 1/ 1/ 20 00 1/ 1/ 19 99 1/ 1/ 1/ 1/ 19 98 600 15 Federal Outlays and Receipts (last obs. June 2010) Outlays are far outpacing receipts. 3500 Outlay s $ billions, 12-month sum 3000 2500 2000 1500 Receipts 1000 500 Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10 16 Source: US Treasury; Encima Global. Federal Government Debt as % of GDP Government Latest CBO Estimate 90% (last obs. 2009, forecast 2010 to 2019) 80 OMB forecast of President's FY2010 budget 70 % of GDP 60 50 40 CBO baseline 30 20 1950 1960 1970 1980 1990 2000 2010 2020 17 Source: OMB; CBO; Encima Global Federal Spending Increases Outpaces Income Growth 18 Source: Heritage Foundation, 2009 Federal Revenue and Spending Book of Charts, WSJ. Implications of Federal Deficits ● Growing deficits will require: ● Higher federal taxes ● Federal budget cuts ● More federal borrowing ● Tax hikes and budget cuts will slow economy. ● Federal borrowing will squeeze out private borrowing. ● Deficits could adversely affect currency, exchange rates, and inflation. 19 What about Michigan? 20 Michigan Employment Never Recovered in Past Expansion Difference from Peak (%) Note: Peak is calculated from Michigan’s June 2000 Peak. 8% 4% 0% U.S. -4% Indiana -8% Ohio -12% -16% Michigan -20% Jun 00 Jun 01 Jun 02 Jun 03 Jun 04 Jun 05 Jun 06 Jun 07 Jun 08 Jun 09 Jun 10 21 Source: U.S. Bureau of Labor Statistics and Michigan Department of Treasury. Michigan Loses Nearly 850,000 Jobs Michigan Wage and Salary Employment Year-Over-Year Change (In Thousands) 88.0 53.6 4.9 -16.9 -76.8 -71.1 -112.7 -9.3 -34.7 -63.3 -58.7 -105.7 -285.6 9100 Avg. 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Note: Bureau of Labor Statistics. 2009-2011 estimates are Treasury Forecast. Treasury Forecast 22 Michigan Personal Income Falling Relative to U.S. Michigan per Capita Income as a Percent of U.S. Per Capita Income 1933* Michigan’s Rank 19 1.25 1945* 12 1970 1980 2000 2009 12 15 18 37 122% 1.2 1.15 1.1 1.05 1 0.95 93% 0.9 87% 19 29 19 33 19 37 19 41 19 45 19 49 19 53 19 57 19 61 19 65 19 69 19 73 19 77 19 81 19 85 19 89 19 93 19 97 20 01 20 05 20 09 0.85 Source: Department of Treasury calculations from U.S. Bureau of Economic Analysis data. *Alaska & Hawaii data not available. 23 Industry Restructuring 25-Year Cycle 1960 New England Textile Industry 1980 Pittsburgh Steel Industry 2000 Michigan Auto Industry 24 How does the State Budget Look? 25 Total State Spending FY 2011 Total Spending: $47.1 Billion Human Services 15% Security 6% General Government 13% Health 30% Natural Environment 2% Jobs & the Economy 3% Education 31% Over 75% of total budget devoted to health, human services and education spending. Source: OBDGG, CM, 3/10/10 26 Michigan GF-GP Revenues Turning Corner GF-GP Revenues Year-Over-Year Percent Change 12.5% 7.5% 6.6% 3.3% 3.0% 1.0% 0.6% -0.5% -8.2% -6.3% -5.6% -9.6% -21.3% 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Source: May 2010 Consensus Conference. 27 General Fund Budget Outlook FY 2010 FY 2011 FY 2012 Beginning Balance Ongoing Revenue 1) Other Revenue Total Revenue $177.2 $6,654.9 $939.9 $7,772.0 $1.9 $7,096.7 $1,154.1 $8,252.7 $10.9 $7,130.1 $897.0 $8,038.0 Expenditures 2) $7,770.1 $8,241.8 $9,684.8 $1.9 $10.9 Balance ($1,646.8) 1) Ongoing Revenue equals consensus estimate for FY10 and FY11. 2) Expenditure increase in FY12 due to loss of restricted ARRA funds and increase in cost to maintain services. Source: State Budget Office, FY10 & FY11; Michigan Department of Treasury, FY12. 28 Michigan School Aid Fund Revenues to Stabilize SAF Revenues Year-Over-Year Pct. Change 5.8% 6.2% 5.7% 3.2% 2.8% 1.6% 1.1% 1.4% 0.8% 0.6% -0.9% -1.6% -5.1% 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 29 Source: May 2010 Consensus Conference. Cons. Forecast School Aid Fund Budget Outlook (dollars in millions) Beginning Balance Ongoing Revenue * ARRA Fed Aid & Other Total Revenue FY 2010 $238.2 $10,749.9 $450.0 $1,641.1 $13,079.2 FY 2011 $163.3 $10,832.9 $184.3 $2,047.0 $13,227.5 FY 2012 $93.3 $11,200.9 $0.0 $1,693.7 $12,987.9 Expenditures ** $12,915.9 $13,134.2 $13,370.6 $163.3 $93.3 Balance * Ongoing Revenue equals consensus estimate for FY10 & FY11. ** Expenditures in FY12 are increased from FY11 by inflation. Source: Michigan Department of Treasury. ($382.8) 30 Major Components of FY 2011 Budget Agreement ● ● ● ● ● ● Tax Amnesty: GF $68.1 million, SAF $26.1 million. Unclaimed Property: GF $168.0 million. Liquor Reforms: GF $9.1 million. State Pension Reforms: GF $60 million. Debt Refinancing: GF $77.3 million, SAF $40.0 million. Reduce spending about $270 million from the Governor’s adjusted original recommendation. 31 How do Local Budgets Look? 32 State To Local Revenue Sharing Cut 33% Last Eight Years Fiscal Year 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 proj. (Millions) Constitutional Statutory $642.8 $649.3 $660.3 $653.1 $668.7 $680.1 $666.0 $688.2 $649.1 $629.1 $633.5 $912.7 $868.0 $791.1 $651.6 $443.3 $422.4 $404.9 $388.0 $391.0 $309.7 $307.1 Total $1,555.5 $1,517.3 $1,451.4 $1,304.7 $1,112.1 $1,102.5 $1,070.9 $1,076.2 $1,040.0 $938.8 $940.5 33 Source: Office of Revenue and Tax Analysis, Michigan Department of Treasury. Most Local Own Source Revenue From Property Taxes FY 2008 Own Source Revenue Plus State and Federal - $25.3 Billion State Revenue Sharing 6% Federal 4% Local Property Taxes 47% Current Charges & Misc. Revenue 39% Other Local Taxes 4% 34 Year-over-Year Pct Change Home Prices Fell Sharply Beginning to Turn Around 30.00% U.S. Prices Fall After Sharp Run Up 20.00% U.S. 10 City June 10 5.0% 10.00% 0.00% -10.00% June 10 0.8% -20.00% Detroit Area -30.00% Jan-92 Jan-94 Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 35 Source: Case Shiller 10-Metro Area Home Price Index. Michigan Home Building Fell Precipitously New Private Housing Units Authorized in Michigan Year Detroit PMSA Ann Arbor Grand Rapids Lansing Total 2004 22,990 2,708 6,886 2,206 54,721 2005 17,326 1,676 5,826 2,121 45,328 2006 9,592 775 4,278 1,231 29,191 2007 4,325 565 1,866 768 17,767 2008 2,590 347 1,064 383 10,911 2009 1,346 209 810 246 6,884 2010YTD 1,539 180 560 304 4,978 Change 2004-2009 Note: 2010 YTD through July Source: U.S. Department of Commerce. -87.42% 36 Overall Michigan Taxable Property Value Growth Slowing Yearly Percent Change 8.0% 6.0% 7.1% 6.1% 6.0% 5.7% 5.5% 6.7% 4.8% 5.7% 5.6% 5.8% 5.2% 4.0% 1.4% 2.0% 0.0% -0.8% -2.0% -4.0% -4.3% -6.0% -6.6% -8.0% 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 est 37 Source: State Tax Commission and May 2010 Consensus Conference. What does Michigan Need to do? 38 Michigan State Government Already Has Fewer Employees Fiscal Year Governor 1973 1978 1989 2000 2009 Milliken Milliken Blanchard Engler Granholm Number Non-Corrections State State Employees Employees % Change 1978-2009 % Change 2000-2009 Source: Michigan Department of Treasury. Corrections Employees 52,673 64,456 64,560 61,493 51,699 50,316 59,990 52,038 43,841 35,937 2,357 4,466 12,522 17,652 15,762 -20% -16% -40% -18% 253% -11% 39 Government Smaller Compared to Other States State State and Local Govt. Employees Per 10,000 of Population Rank Indiana Ohio Minnesota Illinois Wisconsin Michigan 554 538 536 504 504 475 27 32 34 42 42 48 U.S. Average 549 Source: U.S. Bureau of the Census, 2008 State and Local Government Employment Survey. 40 State Government Average Annual Salaries – 2008 State Avg. State Gov't Employee Pay 2008 California Connecticut Minnesota Illinois Wisconsin Michigan Ohio Indiana 10 Most Populous States 10 Least Populous States $70,950 $65,763 $60,843 $58,968 $57,364 $56,955 $55,617 $48,871 $53,960 $49,479 US Average $53,344 Source: Bureau of the Census Rank 1 3 5 7 11 13 15 27 41 What Does Michigan Need to Do? Consolidate government services at both the state and local level. Reform the state’s tax structure so that it will grow with the State’s economy and not discourage economic growth. Slow the growth of government healthcare and tax expenditures. Maintain or increase the investment in education. Reform local government pensions. 42 Too Many Units of Government Local Governments 83 Counties 275 Cities 258 Villages 1,240 Townships K-12 Schools 551 Local School Districts 230 Charter Schools 57 Intermediate School Districts Colleges and Universities 15 Public Universities 29 Community Colleges 43 Ingham County School Districts School District Students Fall 2009 East Lansing Lansing Dansville Haslett Holt Leslie Mason Okemos Stockbridge Waverly Webberville Williamston 3,445 14,148 904 2,722 5,902 1,380 3,030 4,016 1,668 2,992 668 1,906 Total 42,782 Source: Michigan Department of Education. 44 Local Colleges and Universities School Students Fall 2009 Michigan State University 45,520 Lansing Community College 20,394 45 Source: Stateuniversity.com Maryland School Districts Are Large School District Students Montgomery County Public Schools 141,777 Prince George's County Public Schools 129,723 Anne Arundel County Public Schools 74,200 Howard County Public Schools 49,748 Note: Montgomery County Public Schools is 16th largest in the US Source: Maryland County Public Schools, various websites 46 Michigan’s Tax System Needs to be Restructured 47 175% -25% Wyoming Alaska Nevada North Dakota New Mexico Louisiana Montana Hawaii West Virginia Massachuset South Dakota North Tennessee New Jersey Texas New York Mississippi New Indiana Connecticut Maryland Arkansas Nebraska Delaware Virginia Kansas Idaho Rhode Island Ohio Minnesota Oklahoma Utah Kentucky Alabama Florida Iowa Washington Pennsylvania Vermont Georgia Oregon Maine Illinois California Arizona South Wisconsin Colorado Missouri Michigan General Fund Revenue by State Michigan Only State with a Decline Percent Change Between 2000 and 2009 125% 75% 25% 48 Source: Michigan Department of Treasury Inflation Adjusted GF-GP Revenue Down 50.4% Since 2000 $15,000 Millions $10,000 $9,788 $8,990 $9,788 $8,668 $9,359 $8,427 $7,989 $7,959 $7,245 $8,042 $8,309 $8,266 $8,319 Current Dollars $7,366 $7,097 $6,655 $7,077 $6,888 $5,000 $6,475 $6,224 $6,598 $5,187 $4,623 $4,851 Inflation Adjusted $0 2000 2001 2002 2003 2004 2005 2006 2007 Note: FY 2010 and 2011 are May 2010 Consensus Estimates Source: Office of Revenue and Tax Analysis, Michigan Department of Treasury. 2008 2009 2010 2011 49 Inflation Adjusted SAF Revenue Down 25% Since 2000 $15,000 Current Dollars Millions $10,000 $9,889 $9,994 $10,134 $10,715 $10,615 9,889.30 9,636.90 9,607.30 9,753.50 9,342.40 $10,910 $11,082 $11,153 $11,513 9,044.00 8,680.70 8,344.50 8,115.80 $5,000 $10,922 $10,750 $10,833 7,692.00 7,467.40 7,405.30 Inflation Adjusted $0 2000 2001 2002 2003 2004 2005 2006 2007 Note: FY 2010 & 2011 are May 2010 Consensus Estimates Source: Office of Revenue and Tax Analysis, Michigan Department of Treasury. 2008 2009 2010 2011 50 Real State GDP Declines 3.3% since 2000 $350,000 $345,000 Millions $340,000 $337,235 $341,109 $335,000 $336,862 Inflation Adjusted $339,872 $337,851 $334,843 $330,000 $331,036 $326,869 $325,000 $326,123 $320,000 2000 Source: House Fiscal Agency 2001 2002 2003 2004 2005 2006 2007 2008 51 Michigan GF-GP & SAF Taxes Falls as a Percent of Personal Income 7.0% 6.5% 6.0% 5.5% 5.0% 19 96 19 97 19 98 19 99 20 00 20 01 20 02 20 03 20 04 20 05 20 06 20 07 20 08 20 09 20 10 20 11 4.5% If revenues were still 6.8% of personal income, FY 2011 revenue would be $6.3 billion larger. 52 Note: FY 2010 and FY 2011 estimates based on Jan 2010 Consensus. Tax Structure Needs to Keep Pace With Changing Economy Personal Consumption Expenditures by Percentage 80% Services - 67.7% 60% 40% Goods - 32.3% 20% 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 53 Source: U.S. Bureau of Economic Analysis. Tax Breaks / Tax Expenditures Larger Than Tax Collections Tax Breaks Tax Collections 54 Source: House Fiscal Agency. Recent Tax Changes Reduce Future Revenue Generous film production credits enacted to encourage production in Michigan. Battery Credits enacted to encourage production of batteries for hybrid cars in Michigan. Earned Income Tax Credit provides $325 million in 2010 and $338 million in 2011. 55 Significant Tax Cuts Will Cut Future Revenues FY 2009 Reducing Michigan IIT Rate Alternative Energy Credits IIT Michigan EITC $0.0 ($16.0) ($140.0) FY 2010 $0.0 ($46.0) ($325.0) Eliminating MBT Surcharge MBT Battery Credits(1) MBT Film Credits & Infrastructure(2) Photovoltaic Technology - Facility & Manufacturing Polycrystalline Manufacturing Credit FASB 109 MEGA Legislative Changes MBT Gross Receipt Changes Decouple bonus depreciation/production activities Historic preservation credits Promise Zones - SET IFT Exemption for Commercial Real Land Use Tax Bad Debt Deduction Change Exempt supplies for Cobo Center Totals FY 2011 $0.0 ($47.0) ($338.0) FY 2012 ($150.0) ($42.0) ($358.3) FY 2013 ($329.0) $0.0 ($379.8) FY 2014 FY 2015 ($522.5) $0.0 ($402.6) ($728.6) $0.0 ($426.7) Eliminated in Tax Year 2017 $0.0 $0.0 $0.0 ($40.0) ($268.0) ($278.0) ($234.0) ($37.5) $0.0 $0.0 $0.0 NA ($115.8) $172.5 $0.0 ($100.0) ($0.8) $0.0 $0.0 NA ($80.5) $23.4 $0.0 ($125.0) ($9.8) $0.0 $0.0 NA ($93.4) $19.2 ($5.0) ($125.0) ($12.5) $0.0 $0.0 NA ($117.8) $45.3 ($8.6) ($125.0) ($12.5) ($25.0) $0.0 NA ($129.9) $52.3 ($9.6) ($125.0) ($12.5) ($25.0) $0.0 NA ($132.7) $60.0 ($10.6) ($125.0) ($12.5) ($25.0) ($31.3) NA ($135.6) $68.8 ($10.6) $0.0 ($2.0) $0.0 $0.0 ($1.0) ($2.0) ($25.5) $0.0 ($4.0) ($2.0) ($16.6) ($2.5) ($10.0) ($2.0) ($17.1) ($2.5) ($15.0) ($2.0) ($17.7) ($3.5) ($20.0) ($2.0) ($18.4) ($1.5) ($20.0) ($2.0) ($19.1) $0.0 ($138.8) ($557.4) ($624.1) ($840.5) ($1,264.7) ($1,490.8) ($1,701.6) 56 Why Do We Have A Revenue Problem Michigan economy declining for 10 years. Tax System does not keep up with economy. Phased-in tax cuts eroding revenue. 57 Most Revenue Losses Due to Tax Cuts School Aid Fund GF-GP Revenue Economy Tax Structure -15.7% Revenue Loss 2000 to 2009 Tax Cuts -43.4% 58 Source: Michigan Department of Treasury Key Characteristics of a Good Tax System ● Stable – Stable level revenue: ● Broad based taxes. ● Balanced group of taxes (don’t rely on just one major tax). ● Fair – Similar taxpayers pay similar taxes. ● Efficient – Simple to administer and comply with, and should not distort economic decisions. 59 Corporate Income Tax Pros & Cons PROS ● Only corporations making a profit would pay. ● Widely used, therefore multistate companies would have lower compliance costs. ● Longer legal history provides more certainty CONS ● Revenue stream is extremely volatile (federal corporate income tax revenue declined 55% in FY 2009). ● Many businesses (noncorporations) avoid the tax. ● No direct relationship between profitability and dependence on government services. 60 Local Governments Have a Pension Problem ● Pension liabilities exceed assets and costs are growing faster than assets. ● Local pensions are very generous—average multiplier 2.7%. ● Local pensions are subject to abuse, which raises future costs. ● Reform needed. 61 Balanced Approach: Hybrid Retirement Model 1/3 Social Security Defined Benefit Defined Contribution 1/3 1/3 62 Retirement Model Characteristics ● Equal contributions from employer and employee into all three plans. ● Benefits based on lifetime earnings – will greatly reduce abuses. ● Raise retirement age as people live longer. ● Investment risk shared – one-third each. ● May require changes to P.A. 312. 63 Consolidation / Shared Services ● Do for business reasons, not political. ● Important to look at all costs, as transition costs can be larger than savings. 64 Conclusion ● Recession worst in decades, but it appears U.S. economic recovery is beginning to take hold. ● Michigan has been in a recession since 2001 due to auto sector restructuring and U.S. recession. ● Michigan recovery will require U.S. recovery, stability in the auto sector, and time. ● Funding for schools, state and local government depend on economy growing and tax restructuring. ● Government changes needed to reflect new economic reality. 65 Questions www.Michigan.gov/Treasury 66