Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

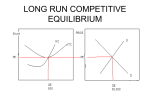

Chapter 9: Monopolistic Competition and Oligopoly McGraw-Hill/Irwin Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved Characteristics of Monopolistic Competition Large number of sellers: Small market shares No collusion Independent action Differentiated products: Firms have some control over prices. Products may differ in attributes services location brand name and packaging Examples: • furniture, • jewelry, • leather goods, • grocery stores, • gas stations, • restaurants, • clothing stores, • medical care. Easy entry and exit LO: 9-1 9-2 Pricing and Output in Monopolistic Competition Monopolistically competitive firms engage in non-price competition (such as advertising) in order to differentiate their products. Because products are differentiated, the demand curve of a monopolistically competitive firm is not perfectly elastic (although it is more elastic than pure monopolist’s demand). The price elasticity of firm’s demand is higher The larger the number of rival firms The weaker the product differentiation LO: 9-2 9-3 Profits and Losses in Monopolistic Competition Short run Long run The monopolistically competitive firm uses the MC=MR Rule to maximize profit or minimize loss in the short run. It produces a quantity Q at which MR = MC and charges a price P based on its demand curve. When P > ATC, the firm earns an economic profit. When P < ATC, the firm incurs a loss. Because entry and exit are easy, Economic profits attract new firms, which lowers profits of existing firms, until P=ATC. Economic losses make firms exit until P=ATC. As a result, monopolistic competitors will earn only a normal profit in the long run. LO: 9-2 9-4 Short-Run Profits in Monopolistic Competition Price and Costs MC ATC P ATC Economic Profit D in SR MR = MC MR 0 Q Quantity LO: 9-2 9-5 Long-Run Profits in Monopolistic Competition Price and Costs MC ATC P ATC P= ATC Economic Profit MR = MC D in SR D in LR MR 0 Q Quantity LO: 9-2 9-6 Monopolistic Competition vs. Pure Competition Price and Costs MC ATC PMC PPC Price is Higher D3 MR = MC Excess Capacity at Minimum ATC 0 MR QMC QPC Quantity LO: 9-2 Monopolistic competition is not efficient 9-7 Characteristics of Oligopoly A few large producers: Firms are price makers Firms engage in strategic behavior Firms’ profits depend on action of other firms Homogeneous or differentiated products: If products are differentiated, firms engage in advertising Examples: • tires, • beer, • cigarettes, • copper, • greeting cards, • automobiles, • breakfast cereals, • airlines. Blocked entry LO: 9-3 9-8 Oligopoly and Game Theory Behavior of firms in the oligopoly can be analyzed using game theory. Consider an example of two firms (a duopoly) which decide whether to set their price high or low. A payoff matrix can be constructed to show payoffs (profit) to each firm that result from each combination of strategies. Game theory is the study of how people or firms behave in strategic situations. LO: 9-4 9-9 Oligopoly and Game Theory: Example RareAir’s Price Strategy • 2 competitors • 2 price strategies • Each strategy has a payoff matrix • Greatest combined profit • Independent actions stimulate a response Uptown’s Price Strategy High A $12 Low B $15 High $12 C $6 $6 D $8 Low $15 $8 LO: 9-4 9-10 Oligopoly and Game Theory: Example RareAir’s Price Strategy • Independently lowered prices in expectation of greater profit leads to the worst combined outcome • Eventually low outcomes make firms return to higher prices • There is a gain from collusion Uptown’s Price Strategy High A $12 Low B $15 High $12 C $6 $6 D $8 Low $15 $8 LO: 9-4 9-11 Kinked-Demand Model of Oligopoly In the kinked-demand model, oligopolists face a demand curve based on the assumption that rivals will ignore a price increase and follow a price decrease. An oligopolist’s rivals will ignore a price increase above the going price but follow a price decrease below the going price. The demand curve is kinked at this price and the marginalrevenue curve has a vertical gap. Price and output are optimized at the kink. This model helps explain why prices are generally stable in noncollusive oligopolistic industries. LO: 9-5 9-12 Kinked-Demand Model of Oligopoly Competitor and rivals strategize versus each other Consumers effectively have 2 partial demand curves and each part has its own marginal revenue part e P0 f D2 Rivals Match g Price Decrease 0 Q0 MR1 Quantity MR2 Price and Costs Price Rivals Ignore Price Increase MC1 D2 P0 e MR2 f MC2 g D1 D1 0 Q0 MR1 Quantity LO: 9-5 9-13 Collusion Collusion, through price control, may allow oligopolists to reduce uncertainty, increase profits, and possibly block potential entry. If oligopolistic firms produce an identical product and have identical cost, demand, and marginal-revenue curves, then each firm can maximize profit using the MR=MC Rule. Firms will choose the price and quantity according to MR=MC Rule because it is the most profitable price-output combination. One form of collusion is the cartel. Cartel is a formal agreement among producers to set the price and the individual firm’s output levels of a product. One example is OPEC. LO: 9-6 9-14 Profit Maximization by a Cartel Price and Costs MC Effectively Sharing The Monopoly Profit P0 ATC A0 MR=MC Economic Profit D MR Q0 Quantity LO: 9-6 Cartel-type oligopoly is inefficient 9-15 Obstacles to Collusion Anti-trust law prevents cartels from forming Demand and costs may be different across firms There may be too many firms to coordinate There are strong incentives to cheat If rivals charge prices lower than Po, then the demand curve of the firm charging Po will shift to the left as customers turn to its rivals, and profits will fall. The firm can retaliate and cut its price, too. However, all firms’ profits would eventually fall. Recessions increase excess capacity and strengthen incentives to cheat High profits attract potential entry LO: 9-6 9-16 Oligopoly and Advertising Oligopolists have sufficient financial resources to engage in product differentiation through product development and advertising. Positive effects of advertising Negative effects of advertising Enhances competition Reduces consumers’ search time, direct costs, and indirect costs Facilitates the introduction of new products Alters consumers’ preferences in favor of the advertiser’s product Brand-loyalty promotes monopoly power LO: 9-7 9-17