Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

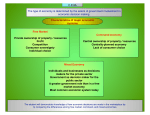

Entrepreneurship – Study guide for Unit 2 (Economics) 2.1 Needs and Wants Needs - things that are necessary for survival Wants - things you think you must have in order to be satisfied. They add comfort and pleasure to your life The role of businesses is to produce and distribute goods and services that people need and want. Maslow’s hierarchy of needs states that: People’s basic physiological needs must be satisfied before they can focus on higher level needs. Needs are different for each person and vary by situation. Wants Economic wants a desire for material goods and services are the basis of an economy 1. clothing 2. housing 3. cars Noneconomic wants nonmaterial things 1. sunshine 2. happiness Needs and wants are unlimited. They never end. One purchase often leads to another. Economic Resources (aka Factors of Production) - the means through which goods and services are produced Goods - products you can see and touch Services - activities that are consumed as they are produced Entrepreneurs use economic resources to create the goods and services consumers use. 1. natural resources - raw materials supplied by nature 2. human resources - the people who create goods and services specialization - when individual workers focus on single tasks. Each worker becomes more efficient and productive. division of labor - divides the production process into separate tasks Workers specialize in specific tasks . The group as a whole becomes more productive. 3. Capital resources - the assets used in the production of goods and services Law of Diminishing Returns - If one factor of production is increased while others stay the same, the resulting increase in output (product produced) will level off after some time and then will decline. 2.2 How economic decisions are made Economic Systems Each economy must answer three basic questions regarding goods and services: 1. What goods and services will be produced? 2. How will the goods and services be produced ? 3. Whose needs and wants will they satisfy? Command Economy Production decisions are made by the government. Few choices exist in the marketplace. Market Economy Production decisions are made by individuals and businesses. Entrepreneurship thrives in a market economy. Many choices exist in the marketplace. Traditional Economy Production occurs the way it has always occurred. Most production is consumed. Left over production is sold or traded. Mixed Economy These economies contain elements of command and market economies. The government is still involved in the marketplace. The U.S. Economic System (Capitalism) the private ownership of resources by individuals rather than by the government individual businesses and consumers make production decisions also called free enterprise The U.S. economic system of capitalism is based on four basic principles. Private Property - You may own whatever you want as long as you operate within the law. Freedom of Choice - Government intervention occurs only when individual decisions will bring harm to others. Profit - the difference between the revenues earned by a business and the costs of operating the business. The opportunity to earn a profit is at the heart of the free-enterprise system. Competition - the rivalry among businesses to sell their goods and services. Economic Choices economic decision making - the process of choosing which needs and wants, among several, you will satisfy using the resources you have scarcity - occurs when there are limited resources available to meet the unlimited needs and wants of consumers. Scarcity forces you to make decisions about tradeoffs. opportunity cost - the value of the next-best alternative make you make a tradeoff (the one you pass up). Functions of a Business 1. Production - The production function creates or obtains products or services for sale. 2. Marketing - The goal of marketing is to attract as many consumers as possible. The marketing mix includes: Product, distribution, price and promotion 3. Management - The duties of management include: setting goals deciding on responses to competition solving problems overseeing employees evaluating business activities 4. Finance - Financial duties include: determining the amount of capital needed determining how capital will be obtained managing the financial records of the business 2.3 What Affects Price? Supply - how much of a good or service a producer is willing to produce at different prices Demand - the quantity of a good or service that consumers are willing to buy at a given price Elasticity of Demand - How much the demand for a product is affected by its price elastic demand - when a change is price creates a change in demand inelastic demand - when a change in price creates very little change in demand equilibrium (aka market) price and quantity - the point at which the supply and demand curves meet Cost of Doing Business fixed costs - costs that must be paid regardless of how much of a good or service is produced. Fixed costs will be incurred regardless of the level of sales. variable costs - costs that fluctuate depending on the quantity of the good or service produced. marginal benefit - measures the advantages of producing one additional unit of a good or service marginal cost - measures the disadvantages of producing one additional unit of a good or service Economies of Scale - the cost advantages obtained due to expansion A lower average cost per unit is achieved through increased production because costs can be spread over an increased number of units.