Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Session #1

Statistical Concepts and Market

Returns

Dr. Himanshu Joshi

Summarizing Data using Frequency

Distribution

• A Frequency distribution is a tabular display of

data summarized into a relatively small

number of intervals.

• Frequency distribution help in the analysis of

large amount of statistical data, and they work

with all types of measurement scales.

Frequency Distribution

• Rates of returns are the fundamental units

that analyst and portfolio managers use for

making investment decisions, and we can use

frequency distribution to summarize rate of

return.

Holding Period Return

Rt = (Pt – Pt-1 + Dt)/Pt-1

Where:

Pt = price per share at the end of period t.

Pt-1 = price per share at the end of time t-1, the time immediately preceding time period t

Dt = cash distribution received during time period t.

Holding Period Return

Equation for holding period return can be

used to define the holding period return on

any asset for a day, week, month, or year

simply by changing the interpretation of the

time interval between successive values of

the time index, t.

Common Stock: the distribution is a dividend.

Bonds: the distribution is a coupon payment.

Holding Period Return: Two Important

Characteristics

Element of Time: Holding period return

has an element of time attached to it. For

example: if a monthly time interval is used

between successive observations for price,

then the rate of return is monthly figure.

No Currency Unit Attached: It has no

currency unit attached to it. The return will

hold regardless of the currency in which

prices are denominated.

Continuously Compounded Returns

• Rt = 100% x ln (Pt/Pt-1)

Construction of Frequency Distribution

Sort the Data in ascending Order.

Calculate the range of the data, defined as Range = Maximum Value – Minimum Value.

Decide on the number of intervals in the frequency distribution, k.

Determine interval width as Range/k

Determine the interval by successively adding the interval width to the minimum value, to determine

the ending point of intervals, stopping after reaching an interval that include maximum value.

Count the number of observations falling in each interval.

Construct a table of intervals listed from smallest to largest that show the number of observations

falling in each interval.

Construction of a Frequency

Distribution

• The actual number of observations in a given

interval is called the absolute frequency, or

simply frequency. The frequency distribution

is the list of intervals together with the

corresponding measure of frequency.

Construction of a Frequency

Distribution: An Example

• Suppose we have 12 observations sorted in

ascending order: -4.57, -4.04,-1.64, 0.28, 1.34,

2.35, 2.38, 4.28, 4.42, 4.468, 7.16, and 11.43.

• Range = Maximum – Minimum = 11.43 – (4.57) = 16

• If we decide number of intervals to be 4.

• Then interval width = range/k = 16/4 =4

Construction of a Frequency

Distribution

• Table 1. Endpoints of Intervals

-4.57+4 =

-0.57

-0.57+4 =

3.43

3.43 + 4=

7.43

7.43 +4=

11.43

• Table 2. Frequency Distribution

Interval

Absolute

Frequency

A

-4.57<=Observation < -0.57

3

B

-0.57<=Observation<3.43

4

C

3.43<=Observation<7.43

4

D

7.43<=Observation<11.43

1

S&P 500, 1926-2002, Total Annual

Return

Frequncy

8

7

6

5

4

3

2

1

0

Frequncy

(-30%) to (-28%)

(-28%) to (-26%)

(-26%) to (-24%)

(-24%) to (-22%)

(-22%) to (-20%)

(-20%) to (-18%)

(-18%) to (-16%)

(-16%) to (-14%)

(-14%) to (-12%)

(-12%) to (-10%)

(-10%) to (-8%)

(-8%) to (-6%)

(-6%) to (-4%)

(-4%) to (-2%)

(-2%) to (0%)

0% to 2%

2% t0 4%

4% to 6%

6% to 8%

8% to 10%

10% to 12%

12% to 14%

14% to 16%

16% to 18%

18% to 20%

20% to 22%

22% to 24%

24% to 26%

26% to 28%

28% to 30%

30% to 32%

32% to 34%

34% to 36%

36% to 38%

38 % to 40%

40% to 42%

42% to 44%

S&P 500, 1926-2002, Total Monthly

Returns

Absolute Frequency

200

180

160

140

120

100

80

60

Absolute Frequency

40

20

0

Interpretation of Frequency

Distribution

Exercise on Construction of Frequency

Distribution

Relative Frequency

• The relative frequency is the absolute

frequency of each interval divided by the total

number of observations.

Using Pivot Table/Grouping to Create

Frequency Distribution

Step#1. Select/activate any cell in the data base, and

insert a pivot table.

Step#2. Drag and Drop Return field in Row Labels and

Value Boxes.

Step#3. Select any return in the row area of the pivot

table and open the Grouping Dialog box by right clicking

on the cell.

Step#4. Excel has already entered the lowest and highest

values in the Return field in the starting and ending at

boxes. It has also suggested a step increment in the box

next to By. Select the Interval Gap and Click OK.

Frequency Distribution Using Excel

Pivot Tables

Count of Return 2007 (%)

-8.33--6.33

1

-2.33--0.33

4

-0.33-1.67

7

1.67-3.67

11

3.67-5.67

6

5.67-7.67

7

7.67-9.67

4

9.67-11.67

6

11.67-13.67

7

13.67-15.67

3

15.67-17.67

8

17.67-19.67

2

19.67-21.67

8

21.67-23.67

5

25.67-27.67

1

27.67-29.67

1

31.67-33.67

2

37.67-39.67

1

39.67-41.67

1

43.67-45.67

1

Grand Total

86

Total

12

10

8

6

Total

4

2

0

-8.33--6.33

-2.33--0.33

-0.33-1.67

1.67-3.67

3.67-5.67

5.67-7.67

7.67-9.67

9.67-11.67

11.67-13.67

13.67-15.67

15.67-17.67

17.67-19.67

19.67-21.67

21.67-23.67

25.67-27.67

27.67-29.67

31.67-33.67

37.67-39.67

39.67-41.67

43.67-45.67

Row Labels

Measures of Central Tendency

1. Arithmetic Mean: Analysts and portfolio

managers often want one number that

describes a representative possible outcome

of an investment decision. The arithmetic

mean is by far the most frequently used

measure of the middle or centre of data.

Definition: Sum of Observations/Number of

Observations.

Arithmetic Mean

• Population Mean

μ = ∑i=1N Xi / N

N= Number of observations in population.

• Sample Mean

X- = ∑i=1n Xi /n

n= Number of observations in sample.

Cross Sectional vs. Time Series Mean

• Cross Sectional Mean: Sample might be the

2013 return on equity (ROE) for 30 companies

in the BSE Sensex. In this case we calculate

mean ROE in 2013 as an average across 30

largest market cap firms in BSE.

• When we examine the characteristics of some

units at a specific point in time, we are

examining Cross-Sectional-Data.

Cross Sectional vs. Time Series Mean

• If our sample consists of historical monthly

returns on BSE Sensex for the past five years,

then we have a time series data.

• Panel Data: Mix of Cross-Sectional Data and

Time Series Data.

Properties of Arithmetic Mean

• Arithmetic mean can be linked to the centre of

gravity of an object.

• Deviations from the arithmetic mean forms the

foundation for more complex concepts of risks

like: variance, skewness, kurtosis, and

heteroscedasticity.

• Advantage of Arithmetic Mean: it uses all

information about size and magnitude of the

observation.

• Limitation: Sensitivity to extreme values, e.g.,

Returns = 2%, 3%, 6%, and -80%.

The Geometric Mean (G.M)..

• The geometric mean is most frequently used

to average rates of change over time to

compute the growth rate of a variable.

• In Investment and valuation, we frequently

use the G.M to average a time series of rates

of return on an asset or a portfolio or to

compute growth rate of financial variables

such as earning or sales.

The Geometric Mean..

• G = n√X1. X2. X3……..Xn

with Xi >= 0 for i= 1,2,3,….n

The above equation has a solution, and geometric

mean exists, only if the product under the radical

sign is non-negative.

Q. Is that O.K for Stock returns?

Q. What can be most negative value of Stock

Return?

Geometric Mean Return Formula

• RG = [∏t=1T (1+Rt)1/T] – 1

Example.. GM and AM..

Q. As a mutual fund analyst, you are examining,

as of early 2016, the most recent five years to

total returns for two U.S large-cap value

equity mutual funds:

Year

SLAX

PRFDX

2002

16.2%

9.2%

2013

20.3%

3.8%

2014

9.3%

13.1%

2015

-11.1%

1.6%

2016

-17.0%

-13.0%

GM and AM

Fund

Arithmetic

Mean

Geometric Mean

Difference (BPS)

SLASX

3.54%

2.43%

111

PRFDX

2.94%

2.53%

41

•Geometric Mean Return is less than the Arithmetic Mean Return. In fact GM is

always less than the AM.

•The only time AM and GM are equal when there is no variability in the

observations- that is when all the observations in the series are same.

•In general, the difference between AM and GM increases with the variability in

the period by period observations.

•Returns of SLASX are more variable than the PRFDX, and consequently the

spread between AM and GM is larger for SLASX.

•Although SLASX has higher AM return, PRFDX has the higher GM return.

How the Analyst should interpret this

result?

•

AM vs. GM Example..

• A hypothetical investment in a single stock

costs $100. one year later, the stock is trading

at $200. at the end of the second year, the

stock price falls back to the original purchase

price of $100. No dividends are paid during

the period of past two years.

• The arithmetic mean return reflects the

average of the one-year returns, while

geometric return is compound rate of return.

Solve for AM and GM

Quartile (1/4), Quintile (1/5), Deciles

(1/10) and Percentiles (1/100)

• Let y be the value at or below which y percent

of the distribution lies, or the yth percentile.

• For example, P18 is the point below which 18

percent of the observations lie; 100-18 =82%

are greater than P18.)

• The formula for the position of a percentile in

an array with n entries sorted in ascending

order is: Ly = (n+1) * (y/100)

Quartile and Percentile

• Calculate the 10th and 90th percentiles.

• Calculate 1st, 2nd, and 3rd quartiles.

• What is the median?

Quintiles in Investment Practice

• Investment analysts use quintiles every day to rank

performance-performance of portfolios and stocks.

• We can illustrate the use of quintiles, in particular

quartiles, in investment research using the example of

Bauman, Conover, and Miller (1998).

• That study compared the performance of international

growth stocks to value stocks.

• Typically growth stocks are defined as those for which

the market price (MPS) is relatively low in relation to

EPS, BPS, and DPS.

• Growth stocks on the other hand, have comparatively

high prices in relation to those same measures.

Quintiles in Investment Practice

• The Bauman et al. classification criteria were

following valuation measures: price to earnings,

price to cash flow, price of book value, dividend

yield (D/P).

• They assigned one fourth of the of the total

sample with the lowest P/E to quartile 1, and the

1/4th with the highest P/E to Quartile to Q4. The

stocks with the second highest P/E formed Q3

and stocks with second lowest P/E formed Q2.

Interpretation..

• Small company portfolio had a median market cap of $46.6

million AND the large company portfolio had a median

value of $2472.3 million.

• Large companies were 50 times larger than small

companies, yet their mean returns were less than the half

those of small companies.

• Overall, Bauman et al. found two effects. First, international

value stocks outperformed international growth stocks.

Second, international small stocks outperformed

international large stocks.

• Next step for analysis: how value and growth stocks

performed while controlling for size?

• This involved constructing 16 different value/growth and

size portfolios (4x4), they found that value stocks

outperformed growth stocks except when market

capitalization was very small.

Measures of Risk

1. Mean Absolute Deviation (MAD) =

∑i=1n |Xi – X-|/n

2. Population Variance and Standard Deviation

3. Sample Variance and Standard Deviation.

Note: Standard Deviation is dispersion from the

arithmetic mean, and not the geometric

mean.

Semi-variance & Semi-deviation

• Variance or standard deviation of returns take account of

returns above and below mean, but investors are

concerned only with the downside risk, for example,

returns below the mean.

• Semi-variance Computation:

1. Calculate sample mean

2. Identify observations that are smaller than mean

(discarding observations equal to or greater than mean);

suppose n* are smaller than the mean.

3. Compute the sum of squared negative deviations from

mean (using n* observations that are smaller than mean)

4. Divide the sum of squared negative deviations by n* -1.

∑for all Xi<X- (Xi – X-)2/(n2 – 1)

Coefficient of Variation

• We may sometimes find it difficult to interpret

what Std. Deviation means in terms of the

relative degree of variability of different set of

data, however, either because the data sets

have markedly different means or because the

datasets have different units of measurement.

• The coefficient of Variation is useful in such

situations:

• CV = s/X- or CV = SD/Mean

CV

The Sharpe Ratio

• Sh= (RP- - RF)/Sp

• Where RP = Return on Portfolio, RF = Risk Free

Return, Sp = S.D of the portfolio

• Although CV was designed as a measure of

relative dispersion, its inverse reveals

something about return per unit of risk

because the standard deviation of returns is

commonly used as measure of investment

risk.

Sharpe Ratio

• Finance theory tells us that in the long run,

investors should be compensated with

additional mean return above risk free rate for

bearing additional risk, at least if the risky

portfolio is well diversified.

Sharpe Ratio

Moments and Central Moments

• The shape of a probability distribution can be

described by the “moments” of the

distribution.

• Raw moments are measured relative to an

expected value raised to the appropriate

power.

• The first moment is the mean of the

distribution, which is expected value of

returns: E(Rk) = ∑ni=1 pi x Rik

Moments and Central Moments

• Central moments are measured relative to the

mean (i.e., central around the mean). The kth

central moment is defined as:

• E(R- μ)k = 𝒏𝒊=𝟏 𝑷𝒊 𝑹𝒊 − 𝝁 𝒌

• Since central moments are measured relative

to the mean, the first central moment equals

zero and is, therefore, not typically used.

The Second Central Moment

(Variance)

• The second central moment is the variance of

the distribution, which measures the

dispersion of data.

• Variance = σ2 = E[(R – μ)2]

• Since the moments higher than the second

central moment can be difficult to interpret,

they are typically standardized by dividing the

central moment by σk.

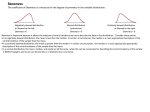

The Third Central Moment (Skew)

• The third moment measures the departure from

symmetry in the distribution. This moment will

be equal to zero for a symmetric distribution

(such as normal distribution).

• Third central moment = E [ (R – μ)3]

• The skewness statistics is the standardized third

central moment. Skewness refers to the extent to

which the distribution of data is not symmetric

around its mean.

• Skewness = E [(R – μ)3]/σ3

The Fourth Central Moment

• The fourth central moment measures the

degree of clustering in the distribution.

• Fourth central moment = E[(R - μ)4]

• The kurtosis statistics is the standardized

fourth central moment of the distribution.

Kurtosis refers to the degree of peakedness or

clustering in the data distribution and is

calculated as:

• Kurtosis = E[(R - μ)4]/σ4

The Fourth Central Moment (Kurtosis)

• Kurtosis for the normal distribution equals

roughly 3. therefore, the excess kurtosis for

any distribution equals:

• Excess Kurtosis = Kurtosis - 3

Symmetry and Skewness in Returns

Distribution

• Mean and Variance may not adequately describe

an investment’s distribution of returns.

• In calculation of variance, for example, the

deviations around the mean are squared, so do

not know whether large deviations are likely to

be positive and negative.

• One important characteristic of interest to analyst

is the degree of symmetry in return distribution.

Normal Distribution

• Its mean and median are equal.

• It is completely described by two parametersits mean and variance.

• Roughly 68.3% of its observations lie between

+/- 1 SD from mean, 95.5% of its observations

lie between +/-2 SD from mean and 99.7% of

observations lie between +/-3 SD from mean.

• A distribution not normal is called Skewed.

Normal Distribution

Skewness

• Nonsymmetrical distributions may be either

positively or negatively skewed and result

from occurrence of outliers in the data set.

• Outliers are observations with extraordinary

large values, either positive or negative.

•

A Positive Skewness

• A Positively skewed distribution is characterized by

many outliers in the upper region, or right tail.

• The mean is affected by the outliers, is a positively

skewed distribution, there are large positive

outliers which will “pull” the mean upward, or

more positive.

Exp. 100 products, 99 sold for Rs.1,00,000, and 1

sold for Rs. 10,00,000

• Mode = Rs. 1,00,000, Median = Rs.1,00,000.

• Mean

=

99,00,000+10,00,000/100=

1,09,00,000/100 = Rs. 1,09,000

Positively Skewed Distribution

A Negatively Skewed Distribution

• A negatively skewed distribution has a

disproportionately large number of outliers on

the lower side of the tail (left tail).

• For a negatively skewed, unimodal distribution,

the mean is less than the median, which is less

than the mode. In this case large, negative outlier

tend to “Pull” the mean downwards (to the left).

• Exp. 100 products, 99 sold for 1,00,000 and 1 sold

for 10,000. Mean = {99,00,000 + 10,000}/ 100 =

99,100, while mode and median = 1,00,000.

Negatively Skewed Distribution

Skewness

• Positive Skewness: A Return distribution with

positive skew has frequent small losses and a

few extreme gains. It has a long tail on its right

side. Mode< Median<Mean

• Negative Skewness: A Return distribution with

negative skew has frequent small gains and

few extreme losses. Mean<Median<Mode

Skewness of a Sample

• SK = [n/(n-1)(n-2)] x ∑i=1n (Xi – X-)3

S3

Q. Calculating Skewness for a Mutual Fund.

Skewness..

Skewness

Interpretation of Skewness..

• Based on this small sample of mutual fund,

the distribution of annual returns for the fund

appears to be approximately symmetric (very

slightly negatively skewed).

• The negative and position deviations are

equally frequent and large positive deviations

approximately offset negative deviations.

Kurtosis

• Another way in which a return distribution might differ

from a normal distribution is by having more returns

clustered closely around the mean (being more Peaked)

and more returns with large deviations from the mean

(having fatter Tails).

• Relative to normal distribution, such a distribution has a

greater percentage of small deviations from mean return

(more small surprises) and a greater percentage of

extremely large deviations from the mean return (more big

surprises).

• Most investors would perceive a greater chance of

extremely large deviations from the mean as increasing

risk.

Kurtosis

• Kurtosis is the measure that tells us when a

distribution is more or less peaked than a

normal distribution.

• A distribution that is more peaked than

normal is called leptokurtic. (more frequent

extremely large surprises)

• A distribution that is less peaked than the

normal is called platykurtic.

• Identical to normal distribution – mesokurtic.

Kurtosis

Kurtosis

Excess Kurtosis

Interpretation of Kurtosis

• The Distribution seems to be mesokurtic,

based on sample excess kurtosis close to zero.

With skewness and excess kurtosis both close

to zero, annual returns seems to have been

normally distributed.

Kurtosis- Interpretation

• Most research about the distribution of the

securities returns has shown that returns are not

normally distributed.

• Actual securities returns tend to exhibit both

skewness and kurtosis.

• Skewness and kurtosis are critical concept of risk

management because when securities returns

are modeled using an assumed normal

distribution, the predictions from the models will

not take into account the potential for extremely

large, negative outcomes.

Skewness-Kurtosis- Interpretation

• In fact, most risk managers put very little

emphasis on the mean and standard deviation

of a distribution and focus more on the

distribution of the returns in the tails of the

distribution – that is where the risk is.

• In general, greater positive kurtosis and more

negative skew in returns distributions

indicates increased risk.

Covariance and Correlation

• Covariance (Ri, Rj) = E{[Ri – E(Ri)][Rj – E(Rj)]}

• Correlation (Ri, Rj) = Covar (Ri, Rj) /σ(Ri) σ(Rj)

Coskewness and Cokurtosis

• Previously, we identified moments and central

moments for mean and variance. In a similar

fashion, we can identify cross central

movements for the concept of covariance.

• The third central movement is called

Coskewness and fourth one is called

Cokurtosis.

Coskewness and Cokurtosis

Stock Returns

Stocks

Time

1

2

3

1

0.00%

-2.40%

-12.60%

-12.60%

-1.20%

-12.60%

2

-2.40%

-12.60%

-5.30%

-5.30%

-7.50%

-5.30%

3

-12.60%

2.40%

0.00%

-2.40%

-5.10%

-1.20%

4

-5.30%

-5.30%

-2.40%

12.60%

-5.30%

5.10%

5

2.40%

0.00%

2.40%

0.00%

1.20%

1.20%

6

5.30%

5.30%

5.30%

5.30%

5.30%

5.30%

7

12.60%

12.60%

12.60%

2.40%

12.60%

7.50%

Mean

0.00%

0.00%

0.00%

0.00%

0.00%

0.00%

Median

0.00%

0.00%

0.00%

0.00%

-1.20%

1.20%

Mode

#N/A

#N/A

#N/A

4 Portfolio A

#N/A

#N/A

Portfolio B

#N/A

Variance

0.0064

0.0064

0.0064

0.0064

0.0050

0.0050

Skewness

0.0000

0.0000

0.0000

0.0000

0.9538

-0.9538

Kurtosis

0.4931

0.4931

0.4931

0.4931

0.3141

0.3141

Covriance 1,2

0.0031

Covariance 3,4

0.0031

Coskewness and Cokurtosis

• Although returns vary over time, the mean,

variance, skewness and kurtosis of all stocks

returns are same under this scenario.

• In addition, the covariance between returns of

stock 1,2 and stock 3,4 are same.

• By combining stock 1,2 in portfolio A, and stock

3,4 in portfolio B, we find that return of portfolio

A and B have the same mean and variance.

• However, these combined returns do not have

the same skewness (i.e., the Coskewness

between stocks in the portfolio is different).

Coskewness and Cokurtosis

• The reason for this difference is that the ranking

of returns over time (e.g., from best to worst) is

different for each stock, and when combined in a

portfolio, these differences skew the portfolio

returns distributions.

• For example, the worst return for Stock 1

occurred during time period 3, but in portfolio A,

the worst return occurred during time period 2.

• Similarly, the best return for stock 4 occurred

during the time period 4, but in portfolio B, the

best return occurred during the time period 7.

Coskewness and Cokurtosis

• From a risk management point of view, it is helpful to know

that the worst outcome in Portfolio B is 1.7 times greater

than the worst outcome in Portfolio A.

• So, although the mean and variance of these portfolios are

equal, shortfall risk expectations can differ depending upon

time period.

• This is important information to know, however most risk

models choose to ignore the effects of Coskewness and

Cokurtosis. The reason being that as the number of

variables increase, the number of Coskewness and

Cokurtosis terms will increase rapidly, making data more

difficult to analyze.

• Practitioners instead opt to use more tractable risk models,

such as GARCH, which captures the essence of Coskewness

and Cokurtosis by incorporating time-varying volatility

and/or time varying correlation.

Using GM and AM

Why GM is appropriate for making investment

statements about past performance?

Why arithmetic mean is appropriate for making

investment statements in a forward looking

context?