Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

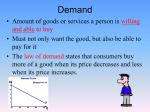

DEMAND, SUPPLY, AND PRICE CHAPTER 3- ECONOMICS DEMAND • Demand is the desire to purchase a particular item at a specified price and time, accompanied by the ability and willingness to pay IN LIFE… AND ECONOMICS… SOMETIMES YOU HAVE TO GET IN THERE… … and just BLOW IT UP!!! Did You Just Say Blow It Up Coach Newman?!?!?!? DEMAND • Demand is the desire to purchase a particular item at a specified price and time, accompanied by the ability and willingness to pay DEMAND • Demand is the desire to purchase a particular item at a specified price and time, accompanied by the ability and willingness to pay DEMAND • Demand is the desire to purchase a particular item at a specified price and time, accompanied by the ability and willingness to pay DEMAND ( BLOWN UP!!!) • Demand is: • the desire to purchase a particular item… • …at a specified price • … and time, • …accompanied by the ability… • …And willingness to pay... THANK YOU CLAY MATTHEWS!!! Your welcome! Ok… um look… we need to get our Demand notes done… Please… go… OH GOD!!! WE’VE ANGERED HIM!!! I THINK HE’S GONE… OK WELL, LETS GET DEMAND SCHEDULE IN QUICK!!! • Demand varies with the price of an item • For an example what would the demand of pizza be like at certain prices? At a Price of Number of Slices students would buy $2.75 1 $2.50 2 $2.25 6 $2.00 12 $1.75 23 $1.50 45 The Chart Above is Our Demand Schedule • This is where we insert demand data into a table and we can see what people would buy at various price levels DEMAND CURVE Oh God… Clay Matthews is stalking us like a lion... Ok well… With the demand schedule shown in a table, now we can plot a demand curve… $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 At a Price of $2.75 $2.50 $2.25 $2.00 $1.75 $1.50 Number of Slices students would buy 1 2 6 12 23 45 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 LAW OF DEMAND • The Law of Demand Tells us that buyers will buy more of an item at a lower price and less at a higher price REASONS WHY THE LAW OF DEMAND WORKS The reason for why the law of demand works is because at a lower price: 1. People can afford to buy the product 2. People tend to buy larger quantities of a product 3. People tend to substitute the product for similar items that are either more expensive or less desirable EXAMPLES: BUTTTTTT… AS PRICE GOES UP Similarly , the law of demand changes as price goes up: 1. Fewer people can afford to buy the product 2. Buyers tend to purchase smaller quantities 3. People tend to substitute products for that product The Law of Demand works here because as the price went up, people bought less pizza slices because they didn’t want to pay the price for those pizza slices, they bought a smaller amount of pizza slices, or found another lunch item to buy instead of pizza $3.00 $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 DEMAND CURVE PRINCIPLE OF DIMINISHING MARGINAL UTILITIES • Economists have devised the concept of marginal utility to help explain the spending patterns of consumers • Marginal utility is the degree of satisfaction or usefulness a consumer gets for each additional purchase of good or service ( Marginal meaning 1) • The Principle of Diminishing Marginal Utility is a phenomenon where each additional purchase of a product or service by a given consumer will be less satisfying than the previous product PRINCIPLE OF DIMINISHING MARGINAL UTILITY CONTINUED… • This applies to almost any product, after you’ve had one of something, buying another will have less utility • What if you bought 4 or 5 of these? ELASTICITY OF DEMAND Some products, regardless of price, will ALWAYS BE DEMANDED Products that are always in high demand: “milk ,gasoline, oil, etc”, are known to have: INELASTIC DEMAND… this means that even when price rises or falls, the demand for these products stays them same, but with a lower price comes HAPPIER CUSTOMERS!!! ELASTIC DEMAND – is when there is a rise or drop in price, the demand for that product can go from unaffordable or not worth buying to buying many just because you can with the cheaper price REASONS FOR A PRODUCT TO BE ELASTIC? 1. The Item is considered a luxury Luxuries are goods or services that consumers regard as something they can live without. If the price is too high, people will live without it. 2. The price represents a large portion of the family income and therefore alternatives are found Buying a car, or home (the biggest investment in most families’ lives), could be diminished if prices go up. REASONS FOR A PRODUCT TO BE ELASTIC? 3. Other products can easily be substituted for it Some products like steak or food can be easily subbed out. Others like steel or gasoline cannot without expensive alternatives. 4. The items are durable or quality Furniture, appliances, and automobiles are relatively long lasting. Many consumers will buy more/ replace existing ones if the price is right. If not, they will make due with the ones they already have SUPPLY Economists use the word “supply” to describe the amount of goods and services offered for sale at a particular price SUPPLY SCHEDULE • Supply varies with the price of an item • For an example why would the supply of pizza increase at higher prices? At a Price of Number of Slices sellers make $2.75 $2.50 $2.25 $2.00 55 45 33 21 $1.75 $1.50 14 2 The Chart Above is Our Supply Schedule -This is where we insert supplied data into a table and we can see what suppliers would sell at various price levels $3.00 SUPPLY CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 LAW OF SUPPLY • The Law of Supply States: • The Quantity of a good or service supplied varies directly with price. • That is, the number of units something offered for sale increases as the price increases, and decreases as the price decreases… • This makes Nintendo go from a playing card company to a video game giant • This makes Apple go from a personal computer giant to the worlds largest seller of music… $3.00 SUPPLY CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 The Law of Supply works here because as the price went up, suppliers want to make more pizza slices because they believe the risk of making more slices with worth the sales they can make off these higher priced slices. With this said, perhaps other sellers would come into the pizza market and also sell pizza 20because 30 of their 40own profit 50 motive. Number of Slices Sold LAW OF SUPPLY • The Law of Supply tells us that sellers will sell more of an item at a higher price and less at a lower price • A key reason is a higher price could bring in more sellers to sell that good or service ELASTICITY OF SUPPLY ELASTIC SUPPLY– If a change in price causes a larger percentage change in supply, supply is said to be elastic. • For example: Most manufactured goods are subject to larger supply elasticity than natural goods. Why? • Employees can work overtime to make more of a manufactured good VERSUS • Dairy Farmers could not expect such cooperation from their herds YES!!! WORK!!! WOOOOOOOOOOOOOOOORK!!! NO!!! THERE IS NO MORE AFTER A WHILE!!! EXAMPLES OF ELASTICITY OF SUPPLY Example of ELASTIC SUPPLY- Any manufactured good due to the fact that producers can work more hours, use better technologies, new methods of production, faster transportation systems, communications, etc. Examples: iPods, cosmetics, skateboards, action figures, desks, concrete mix, hammers, metal detectors, boots, hockey sticks, books, etc etc etc etc etc etc etc EXAMPLES OF ELASTICITY OF SUPPLY Example of INELASTIC SUPPLY- Any natural product due to the limited amount that the earth has and the time it takes to grow or renew that product (if that’s possible) Examples: Oil (OBVVVVVVVVVVVVVVVVVVVVVVVI), milk, lumber, and spring water PRICE The point in which goods and services are exchanged between supply and demand As price increases, the number of items offered for sale (supply) increases…. BUT As the price increases the quantity that buyers are willing to buy (demand) decreases… $3.00 SUPPLY CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 As price increases, the number of items offered for sale (supply) increases… . $3.00 DEMAND CURVE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 As the price increases he quantity that buyers are willing to buy (demand) decreases… PRICE IS WHERE THE LINES INTERSECT Price is found where our Supply Curves and Demand Curves Meet… $3.00 PRICE $2.75 $2.50 Price of Slices $ $2.25 $2.00 $1.75 $1.50 $1.25 0 10 15 20 30 Number of Slices Sold 40 50 WHAT IFS… When looking at “Price”, “ceterus paribus” must be used to discuss the theories and terms associated with price… • This means NO WHAT IFS… right not at least… • We can have no “what if’s” if we talk about “Perfect Competition” PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 1. There are many buyers and sellers acting independently. No single buyer or seller is big enough to influence the market price… PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 2. Competing products are practically identical, so that buyers and sellers of a given product are not affected by variations in quality or design. PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 3. All buyers and sellers have full knowledge of prices being quoted all over the market PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 4. Buyers and sellers can enter and leave the market at will. That is, buyers are free to buy or not to buy, sellers are free to sell or not to sell PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 1. There are many buyers and sellers acting independently. No single buyer or seller is big enough to influence the market price… 2. Competing products are practically identical, so that buyers and sellers of a given product are not affected by variations in quality or design. 3. All buyers and sellers have full knowledge of prices being quoted all over the market 4. Buyers and sellers can enter and leave the market at will. That is, buyers are free to buy or not to buy, sellers are free to sell or not to sell EQUILIBRIUM PRICE/ MARKET PRICE The maximum number items demanded, meets the maximum items supplied, in “perfect competition” EQUILIBRIUM PRICE With our chart for pizza, the supply and demand curves show us that the “Market Price” or “Equilibrium Price” is selling 17 slices for around $1.85. However, will this price be offered? Will this market price always be the same? What might change this price with regards to supply or demand? THEREFORE… CAN EQUILIBRIUM/ MARKET PRICE EXIST? NO!!! SO… LETS MESS UP “PERFECT COMPETITION”!!! OH HELL YEAH COACH NEWMAN!!! LETS DO IT!!! PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 1. There are many buyers and sellers acting independently. No single buyer or seller is big enough to influence the market price… HOW IS THIS COUNTERED IN THE REAL WORLD? PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 2. Competing products are practically identical, so that buyers and sellers of a given product are not affected by variations in quality or design. HOW IS THIS COUNTERED IN THE REAL WORLD? PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 3. All buyers and sellers have full knowledge of prices being quoted all over the market HOW IS THIS COUNTERED IN THE REAL WORLD? PERFECT COMPETITION Perfect Competition, which cannot exist in the real world, is the best way to talk about supply, demand, and market price. Under perfect competition, the following conditions exist 4. Buyers and sellers can enter and leave the market at will. That is, buyers are free to buy or not to buy, sellers are free to sell or not to sell HOW IS THIS COUNTERED IN THE REAL WORLD? SO PERFECT COMPETITION CANNOT EXIST, AND PRICE IS CONSTANTLY FLOWING BACK AND FORTH BETWEEN BUYERS AND SELLERS THROUGH THE BUSINESS DAY, WEEK, MONTH, YEAR, DECADE, CENTURY, ETC… PRICE CEILING AND PRICE FLOOR Sometimes governments attempt to control the market by imposing ceilings and floors on prices A price ceiling sets a maximum price that sellers may charge for their products Price ceilings are set up to make sure people can afford items like bread/ food for survival A price floor guarantees sellers a minimum price for their products Price floors have been set up by the US government to help farmers by guaranteeing a minimum price on one or more of their crops.