Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

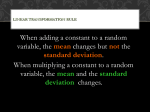

Standard deviation Upside/ Downside capture dard deviation An Upside Capture Ratio greater than 100% indicates that the fund has generally returned more than the index during periods of positive returns for the index. A Downside Capture Ratio less than 100% indicates that the fund lost less than the index during months the index had a negative return. A negative Downside Capture Ratio indicates that the fund generally has a positive return in months that the index has had a negative return. Standard deviation measures the dispersion of a data set from its mean. The further the data points are from the mean, the higher the deviation within the data set. Calculating standard deviation involves taking the square root of variance by determining quadratic variation between each data point relative to the mean. In finance, annualized standard deviation is applied to an investment’s rate of return to measure its historical volatility. 1 𝜎=√ ∑(𝑅𝑗 − 𝜇)2 𝑋 √12 𝑛−1 𝜎: 𝑎𝑛𝑛𝑢𝑎𝑙 𝑠𝑡𝑎𝑛𝑑𝑎𝑟𝑑 𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛 n: number of months in the sample 𝑅𝑗 : investment return in month j 𝜇 : average monthly return of the sample This ratio shows whether a fund has gained more or lost less than a broad index during periods of market strength and weakness, and if so, by how much. The Upside Capture Ratio is calculated by taking the fund’s monthly compounded returns annualized during months when the index has had a positive return and dividing it by the index’s monthly compounded returns annualized. The Downside Capture Ratio is calculated by taking the fund’s monthly compounded returns annualized when the index has had a negative return and dividing by the index’s monthly compounded returns annualized. Sharpe ratio The Sharpe ratio is a widely used method for calculating risk-adjusted returns. It is calculated by taking the mean portfolio return, subtracting the risk-free rate and dividing the result by the standard deviation of the returns. Generally speaking, a higher Sharpe ratio is associated with a better riskadjusted return. Caution must be used when interpreting Sharpe Ratios as the methodology is not flawless since it can be inaccurate when looking at assets that do not have a normal distribution of expected returns or for assets that have ‘fat tails.’ Furthermore, the Sharpe ratio does not distinguish between upside volatility (positive returns) and downside volatility (losses). 𝑅𝑝 − 𝑟𝑓 𝑆ℎ𝑎𝑟𝑝𝑒 𝑟𝑎𝑡𝑖𝑜 = 𝑅 −𝑟 𝑆ℎ𝑎𝑟𝑝𝑒 𝑟𝑎𝑡𝑖𝑜 = 𝑝𝜎 𝑓𝜎𝑝 𝑝 Rp: portfolio expected/mean return rf: risk free rate σp: portfolio standard deviation 12 𝑈𝑝𝑠𝑖𝑑𝑒 𝐶𝑎𝑝𝑡𝑢𝑟𝑒 𝑅𝑎𝑡𝑖𝑜 = 𝑁 ⌊∏𝑗,𝑅𝑗𝑚≥0(1 + 𝑅𝑗 )⌋ − 1 ⌊∏ (1 + 𝑗,𝑅𝑗𝑚 ≥0 ⌊∏ 𝐷𝑜𝑤𝑛𝑠𝑖𝑑𝑒 𝐶𝑎𝑝𝑡𝑢𝑟𝑒 𝑅𝑎𝑡𝑖𝑜 = 12 𝑚 𝑁 𝑅𝑗 )⌋ (1 + 𝑅𝑗 )⌋ 𝑗,𝑅𝑗𝑚 ≤0 −1 12 𝑁 12 𝑁 ⌊∏𝑗,𝑅𝑗𝑚 ≤0(1 + 𝑅𝑗𝑚 )⌋ −1 −1 𝑅𝑗 : 𝑖𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖𝑛 𝑚𝑜𝑛𝑡ℎ 𝑗 𝑅𝑗𝑚 ∶ 𝑖𝑛𝑑𝑒𝑥 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖𝑛 𝑚𝑜𝑛𝑡ℎ 𝑗 N: number of months Sortino Ratio Correlation dard deviation The Sortino ratio is a variation of the Sharpe ratio that is concerned with downside volatility as opposed to general volatility which includes positive returns. The Sortino ratio takes the fund’s return and subtracts the minimal acceptable return (zero percent for the Algonquin Debt Strategies Fund LP) and divides the result by the downside deviation. Generally speaking, the higher the Sortino ratio the better the risk-adjusted return. 𝑆𝑜𝑟𝑡𝑖𝑛𝑜 𝑟𝑎𝑡𝑖𝑜 = 𝑅𝑝 − 𝑟𝑓 𝜎 Rp: portfolio expected/mean return rf: risk free rate σ: downside deviation standard deviation Correlation is a statistic that measures the degree to which two assets move in relation to each other. Correlation is expressed by computing the correlation coefficient which has a value that falls between -1 and 1. If the correlation coefficient is 1, then the assets are perfectly positively correlated. This means the two assets always move in the same direction. If the correlation coefficient is -1, the two assets always move in different directions. 𝑟𝑋,𝑌 = 𝐶𝑜𝑣(𝑋,𝑌) 𝜎𝑋 𝜎𝑌 𝑁 1 𝐶𝑜𝑣(𝑋, 𝑌) = ∑(𝑥𝑖 − 𝑥̅ ) (𝑦𝑖 − 𝑦̅) 𝑁 𝑖=1 σ: standard deviation N: number of observations