Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

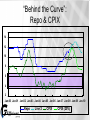

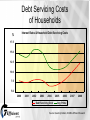

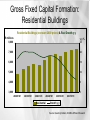

The South African Economy & Property Market Presented by: Dawie Roodt 19 June 2008 In This Presentation: 1. 2. 3. 4. 5. 6. The US Subprime Crisis SA: Economic Overview Monetary Policy Eskom Property Trends Asset Allocation Subprime, Say Wha’ ?? • Subprime definition: – A loan that is offered at a rate above prime (0.1% - 0.6% higher) to individuals who do not qualify for prime rate loans. • • • • A.k.a “NINJA” loans Improved Borrowing Power Decline in Lending Standards Large-scale lending and borrowing U.S. Borrowing Power -39.4% Source: T2 Partners LLC, March 2008 Decline in Lending Standards Since 2001: Between 1995 and 2006 – Combined Loan to Value increased from Total 79.8% toValue 89.1%of Subprime Loans Increased – 100% Financing more than Tripled 15 times!! ($40 bn to $600bn) – “Liar’s Loans” almost Doubled Source: T2 Partners LLC, March 2008 Fed Funds Rate – A Matter of Interest Federal Funds Rate 6.5 5.5 4.5 3.5 2.5 Subprime Lending 1.5 0.5 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Federal Funds Rate Jan-06 Jan-07 “Poppo Strikes The Fan” • Dec 2004: interest rates hiked 125% from 1% to 2.25% • • • • Continuously hiked till 5.25% (Jun 06 to Aug 07) Borrowers start to default.. Banks and Securities firms report losses Total losses are estimated +/- $900bn losses (est) – – Nearly FOUR times the SA’s economy!! Fed Funds Rate – A matter of Interest Federal Funds Rate 6.5 5.5 4.5 3.5 2.5 Subprime Lending 1.5 0.5 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Federal Funds Rate Jan-06 Jan-07 Jan-08 Fed’s Rescue Plans • Dramatic cuts in interest rates: 5.25% (Sept 07) to 2.25% (Mar 08) • $200bn Securities for Mortgage Loans • $168bn Fiscal Injection • Lender of Last Resort • Orchestrate buy-out of Bear Sterns by JP Morgan Chase • Major Regulation Overhaul: Fed gains more oversight responsibility Consequences….. • • • • Weaker Dollar Inflation concerns Slower U.S. growth Rush to Commodities Next Bubble…. Commodities..?? South Africa Economic Overview 2006 2007 2008 M3 (average) 23.1% 23.7% 20.7% PSCE (adj. average) 27.6% 22.2% 18.4% CPIX (average) 4.6% 6.5% 10.7% Prime (end of year) 12.5% 14.5% 16.0% Current Account: Nom -R111.0bn -R138.2bn -R160.0bn Current Account: GDP -6.4% -7.3% -6.9% R/$ (end of year) R7.04 R6.84 R7.50 GDP (full year) 5.4% 5.1% 3.0% (0.3%) 0.7% 1.0% Budget Surplus/(Deficit): GDP Monetary Policy Inflation CPI and CPIX 15 CPIX Ave 2008: 10.7% 12 9 6 3 0 Jan-01 Jan-03 Jan-05 CPIX EstmX Jan-07 CPI Jan-09 Jan-11 Estm Source: StatsSA and own calculations “Behind the Curve”: Repo & CPIX 14 12 10 8 6 4 2 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Repo Line 2 CPIX CPIX (20%) Inflation…The Real Villain • Price = Purchasing Power of $ • Thus, if wage increases don’t equal price increases – WE are WORSE off • AND… – The poor spends more of their money on living expenses than the rich – Thus, inflation is almost a “tax on the poor” “The Good, the Bad & the Ugly” • The Good – Economy still likely to grow • The Bad – C/A Deficit Credit demand remains strong End of Inflation targets? • The Ugly Eskom Toothless SARB GDP GDP at Market Prices % GDP market prices, q:q seasonal 8 7 Construction 3.5% of GDP Best Performing Sector 2007, 2008Q1 (real 14.9% y:y) 6 5 4 Average: 3% 3 2 1 0 2002 2003 2004 2005 2006 2007 2008 Source: StatsSA and own calculations A Quick Eish’kom Calculation Vision: "Together building the powerbase for sustainable growth and development." Load Shedding: The 3 Hour Effect Average GDP per day: • • • GDP, 2007 (current): R1,973.4bn Workdays: 240 GDP per day: R8.3bn Average GDP per sector: • Allocate equal weights to GDP sectors: (3 out of 24) – Loss per day: R1.1bn (13.3%) Average GDP loss per sector: • Allocate weights to GDP sectors: – Finance, real estate and business services (3 out of 8) – Mining and quarrying (3 out of 24),etc. – Loss per day: R1.9bn (22.8%) Potential Job Losses Case Study: +/- 500 000 employees in Mining Sector Mining production at 95% electricity – Lose 10% - 15% 1% loss in production = 1% reduction in workforce Thus, potential reduction in mining workforce: 50 000 – 75 000 jobs lost Source: Thousands face job chop at GFI, 31 Jan 2008, Fin24 GDP Loss: Base Case Scenario Adjusted Growth Estimate: 4.6% na 3.0% Loss in Real Terms: R19.76 bn Potential Loss in Tax Revenue: R5.9 bn Debt Levels Household debt to disposable income % Household debt to disposable income of households 80 Q108: 78.2% 75 70 59.4% 65 56.9% 60 55 50 50.2% 44.5% 45 40 1970 1975 1980 1985 1990 1995 2000 2005 Source: SARB and own calculations Savings to disposable income of households Ratio of saving by households to disposable income of households % 12 9.2% 10 8 5.4% 6 4 2.6% 2 0.5% 0 -2 1970 1975 1980 1985 1990 1995 2000 2005 Source: SARB and own calculations Debt Servicing Costs of Households Interest Rates & Household Debt Servicing Costs % 17.5 15.0 12.5 10.0 7.5 5.0 2000 2001 2002 2003 2004 Debt Servicing Cost 2005 2006 2007 2008 Avg Prime Source: Quarterly Bulletin, SARB & Efficient Research Final Consumption Expenditure by Households Final Consumption Expenditure by Households (Q:Q change) % 10 9 8 7 6 5 4 3 2 1 0 Q1 02 Q1 03 Q1 04 Q1 05 Q1 06 Q1 07 Q1 08 Source: SARB and Efficient Research forecast Property Trends Housing Trends % Real house prices vs Real interest rates 30 25 20 15 10 5 0 -5 -10 -15 -20 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 Source: Absa House Price Index, StatsSA and own calculation Gross Fixed Capital Formation: Residential Buildings Residential Buildings (constant 2000 prices) & Real Growth y:y R millions 8,000 y:y % 25 7,000 20 6,000 15 5,000 10 4,000 5 3,000 0 2005/01/01 2005/07/01 2006/01/01 2006/07/01 Residential 2007/01/01 2007/07/01 Growth y:y Source: Quarterly Bulletin, SARB & Efficient Research Gross Fixed Capital Formation: Non-Residential Buildings R millions Non-Residential (constant 2000 prices) & Real Growth y:y 6,500 y:y % 16 5,500 12 4,500 3,500 8 2,500 4 1,500 500 0 2005/01/01 2005/07/01 2006/01/01 2006/07/01 Non-Residential 2007/01/01 2007/07/01 Real y:y Source: Quarterly Bulletin, SARB & Efficient Research Value of Buildings Completed Change in Value of Buildings Completed % y:y 3m ave 70 60 50 40 30 20 10 0 -10 -20 -30 Q1 2000 2001 Jan-00 01-Jan-06 2002 Jan-01 01-Jan-07 2003 2004 Jan-02 01-Jan-08 2005 Jan-03 2006 Jan-04 2007 2008 Jan-05 Source: StatsSA Value of Buildings Completed Change in Value of Buildings Completed % y:y 3m ave 70 60 50 40 30 20 10 0 -10 -20 -30 Q1 2000 2001 2002 2003 Total value of buildings 2004 2005 2006 2007 2008 Non-residential Source: StatsSA Value of Buildings Completed Change in Value of Buildings Completed % y:y 3m ave 70 60 50 40 30 20 10 0 -10 -20 -30 Q1 2000 2001 2002 Total value of buildings 2003 2004 2005 Residential 2006 2007 2008 Non-residential Source: StatsSA Value of Buildings Plans Passed Change in Value of Building Plans Passed % y:y 3m ave 80 70 60 50 40 30 Q1 20 10 0 -10 2000 2001 Jan-00 01-Jan-06 2002 Jan-01 01-Jan-07 2003 2004 Jan-02 01-Jan-08 2005 Jan-03 2006 Jan-04 2007 2008 Jan-05 Source: StatsSA Value of Buildings Plans Passed Change in Value of Building Plans Passed % y:y 3m ave 80 70 60 50 40 30 Q1 20 10 0 -10 2000 2001 2002 2003 Total value of buildings 2004 2005 2006 2007 2008 Non-residential Source: StatsSA Value of Buildings Plans Passed Change in Value of Building Plans Passed % y:y 3m ave 80 70 60 50 40 30 Q1 20 10 0 -10 2000 2001 2002 Total value of buildings 2003 2004 2005 Residential 2006 2007 2008 Non-residential Source: StatsSA Residential Property Trends Factors Impacting Residential Property • • • • • Higher Inflation & Interest rates Higher Debt Servicing costs Slower Economic growth Slower growth in Disposable Income Stricter Lending Standards (NCA) Affordable Housing: Real growth Q108: 3.5% y/y (2007 11.2%; 2006 9.7% y:y) Q108: R277 000 Source: Absa Housing Review, Q208 Middle-Segment Housing: Real growth Q108: -0.3% y:y (2007 7.0%; 2006 10.1%) Q108: R976 000 The first real decline since Q2 1999 (-2.3% y:y) Source: Absa Housing Review, Q208 Luxury Housing Real growth Q108: -2.9% y:y (2007 1.0%; 2006: 6.0%) Q108: R4.2m Q307: -0.6% y:y The first real decline since Q4 2002 Source: Absa Housing Review, Q208 Building Cost of Middle Segment Housing Avg cost increase Q108: 9.6% (2007 9.5%; 2006: 11.1%) Upward Pressure: Demand for Building Material Skilled Workers Downward Pressure: Softer Housing Market Source: Absa Housing Review, Q208 New vs Old Houses New House (Q108) = R1,055m (real 5.7% y/y) Existing House (Q108) = R960 000 (real -2.0% y/y) New house is 9.0% or R95 000 cheaper Source: Absa Housing Review, Q208 Housing Affordability Source: Absa Housing Review, Q208 Given these trends… Buyer’s Market Buy-to-Let Market Annual House Price Growth (Nominal) Country 2006 2007 Latest South Africa U.K. U.S. Norway 15.4 8.0 6.5 13.2 14.5 9.7 2.0 12.4 8.7 4.2 -0.3 7.3 Switzerland Sweden Ireland 3.2 12.2 11.8 2.6 10.2 -7.3 2.4 11.3 -7.3 Australia New Zealand 7.0 10.5 10.2 12.1 12.3 11.4 Source: Financial Stability Review SARB, March 2008 International Comparison: All Property Returns Total Return (% y:y) Source: IPD Annual Property Index, 2007 Performance: After-Tax Return of Different Asset Classes Source: Asset Performance Survey 2008, Credit Suisse Standard Securities Possible Investment Opportunities 2006 M3 (end of year) 23.1% Financials PSCE (adj. end of year) 27.6% - Banks Financials CPIX (average) 4.6% Retailers Positive for equity, property Prime (end of year) Negative12.5% for bonds Current Account: Nom 2007 2008 23.7% 20.7% 22.2% 18.4% 6.5% 10.8% 14.5% 16.0% -R111.0bn -R138.2bn Negative equities bonds (short term) Current Account: GDP Negative -6.4% -7.0% Positive for rand hedges Positive bonds (long term) Negative for7.04 importers R/$ (end of year) 6.84 Positive rand Negative forhedges bonds GDP (full year) 5.4% 5.1% Positive exporters Negative importers Neutral equities Negative bonds Positive bonds -R160.0bn -6.9% 7.50 3.0% www.efgroup.co.za