Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

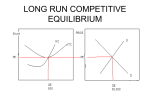

ECN 112 Chapter 15 Lecture Notes 15.1 What is Monopolistic Competition? Monopolistic competition is characterized by four factors: a large number of firms, product differentiation, competition on price, product quality, and marketing, and firms are free to enter and exit. A. A Large Number of Firms The large number of firms implies 1. A small market share for each firm. 2. No market dominance by a single firm, so no one’s firm’s actions directly affect the actions of other firms. 3. Collusion is impossible because there are so many firms. B. Product Differentiation Product differentiation is making a product that is slightly different from the products of competing firms. As a result there are no perfect substitutes and so the firm in monopolistic competition faces a downward-sloping demand curve. C. Competing on Quality, Price, and Marketing A firm in monopolistic competition will compete on: 1. Quality A firm promotes the idea that its product has better attributes than its competitors’ products. These attributes include design, reliability, the service provided to the buyer, and the buyer’s ease of access to the product. 2. Price A firm in monopolistic competition faces a downward-sloping demand curve so the firm can set both its price and its output. 3. Marketing A firm uses advertising and packaging to publicize its product’s uniqueness. D. Entry and Exit If firms in monopolistic competition earn an economic profit in the short run, new firms enter the market. This increase in supply decreases each firm’s demand and lowers the price until only a normal profit is earned. If firms incur economic losses in the short run, some firms exit the industry. The price rises until a normal profit is earned by the remaining firms. E. Identifying Monopolistic Competition. 1. The Four-Firm Concentration Ratio The four-firm concentration ratio is the percentage of the value of sales accounted for by the four largest firms in an industry. A four-firm concentration ratio that exceeds 60 percent is regarded as an indication of a market that is highly concentrated and dominated by a few firms in an oligopoly. A ratio of less than 40 percent is regarded as an indication of a competitive market—monopolistic competition. 2. Herfindahl-Hirschman Index The Herfindahl-Hirschman Index (HHI) is the square of the percentage market share of each firm summed over the 50 largest firms (or summed over all the firms if there are fewer than 50) in a market. If the HHI is greater than 1,800, the market is regarded as being uncompetitive. This measure is used as a guideline by the Justice Department for decisions regarding whether to challenge a merger. 3. Limitations of Concentration Ratios a. Geographic Scope of the Market Concentration ratios take a national view of the market but some goods are sold in regional markets (in which case the extent of competition might be overstated) and others in global markets (in which case the extent of competition might be understated). b. Barriers to Entry and Firm Turnover Concentration ratios don’t take account of the absence or presence of barriers to entry. 15.2 Output and Price Decisions A. The Firm’s Profit-Maximizing Decision 1. Facing a downward-sloping demand curve, a firm in monopolistic competition chooses its profit-maximizing price and quantity as does a monopoly. 2. The firm produces at the quantity that sets marginal revenue equal to marginal cost. The firm charges the price that buyers are willing to pay for this quantity, which is determined by the demand curve. 3. Economic profit in the short run is possible and equals quantity (price average total cost). B. Profit Maximizing Might Be Loss Minimizing If price is less than average total cost, a firm in monopolistic competition incurs an economic loss. C. Long Run: Zero Economic Profit 1. There is no restriction on entry in monopolistic competition, so if firms in monopolistic competition are earning an economic profit, other firms to enter the industry. As new firms enter, an individual firm’s demand and marginal revenue decrease. New firms enter until economic profit disappears and the remaining firms earn normal profit. 2. If firms in monopolistic competition are incurring an economic loss, some firms leave the industry. As firms exit, a remaining firm’s demand and marginal revenue increase. Firms exit until economic loss disappears and the remaining firms earn normal profit. D. Monopolistic Competition and Perfect Competition 1. Excess Capacity Excess capacity occurs when the quantity that a firm produces is less than the quantity at which average total cost is a minimum. A firm with excess capacity produces below its efficient scale, which is the quantity at which average total cost is a minimum. 2. Markup Markup is the amount by which price exceeds marginal cost. A firm in monopolistic competition has a markup because price exceeds marginal cost but a firm in perfect competition has no markup. E. Monopolistic Competition and Efficiency 1. Making the Relevant Comparison A firm in monopolistic competition chooses a profit-maximizing quantity where the markup is positive (price is greater than marginal cost), which means that marginal benefit exceeds marginal cost. This choice implies that the firm inefficiently uses resources. (Efficiency requires that price = marginal benefit = marginal cost). But a benefit of monopolistic competition is that it creates product variety. 2. The Bottom Line Compared to the alternative—complete product uniformity—monopolistic competition is efficient. 15.3 Product Development and Marketing A. Innovation and Product Development A firm in monopolistic competition will continuously develop new products so that it can continue to earn an economic profit. If the firm does not innovate, new firms will enter the market and capture the existing firm’s economic profit. 1. Cost Versus Benefit of Product Innovation To decide the degree to which it will innovate, a firm compares the marginal cost of innovation to the marginal benefit of innovation. 2. Efficiency and Product Innovation On one hand, product innovation brings to market many improved products that have great benefits to consumers. On the other hand, many so-called improvements amount to little more than packaging changes. B. Advertising A firm uses advertising and packaging to convince consumers that its product differs from and is better than other products. These differences can be real or perceived. 1. Advertising Expenditures The cost of selling a good can represent a large portion of the price that consumers pay for a product. 2. Selling Costs and Total Costs Selling costs, such as advertising expenditures are fixed costs and increase total costs. These expenditures shift the average total cost curve upward. If advertising expenditures increase sales enough, the average total cost of the amount produced might decrease. 3. Selling Costs and Demand Advertising might increase demand for a firm’s product (by taking away other firms’ customers) or might decrease demand (as new firms enter the market trying to earn an economic profit). C. Using Advertising to Signal Quality A signal is an action taken by an informed person (or firm) to send a message to uninformed people. A firm uses advertising to signal consumers that its product differs from and is better than other products. D. Brand Names Brand names provide information to consumers about the quality of a product and provide an incentive to producers to keep the quality high and consistent. E. Efficiency of Advertising and Brand Names Whether advertising and brand names lead to efficiency is ambiguous. We must compare the benefits of the information provided by these means with the opportunity cost of the additional information.