Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

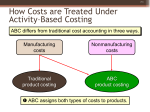

1. ________ and ________ are typically the measures of volume of activity in traditional volume-based cost systems. Practical capacity; products sold Direct labor hours; practical capacity Direct labor hours; machine hours Square footage; machine hours 2. Traditional cost systems distort product costs because: they do not know how to identify the appropriate units excess capacity costs are ignored they emphasize financial accounting requirements they use unit-level cost drivers to allocate support costs to products 3. Unit-level cost drivers in traditional cost systems distort product costs because they: assume that all support activities affect all products recognize specific activities that are required to produce a product do not consistently record costs fail to measure the correct amount of total costs for all products 4. The use of unit-related measures to assign support costs is more likely to: undercost high-volume products undercost specialty low-volume products undercost complex products Both (b) and (c) are correct. 5. Misleading product cost numbers are MOST likely the result of misallocating: direct material costs direct manufacturing labor costs support costs All of the above are correct. 6. Undercosting a particular product may result in: loss of market share for the product lower profits for the product operating inefficiencies understating total costs of all the products 7. It is important that the product costs reflect as much of the diversity and complexity of the manufacturing process so that: product costs will reflect their relative consumption of resources better information related to resource constraints can be captured and communicated there is less likelihood of cost distortions All of the above are correct. 8. Which of the following is a sign that an ABC system may be useful? There are small amounts of support costs. Products make diverse demands on resources because of differences in volume, process steps, batch size, or complexity. Products a company is less suited to produce and sell show small profits. Operations throughout the plant are fairly similar. 9. Units of production are most appropriate as a support cost assignment base when: it is a service department only one product is manufactured direct labor costs are low factories produce a complex and varied mix of products 10. Designing an activity-based cost system includes: classifying as many costs as indirect costs as is feasible creating as many cost pools as possible identifying the activities performed by the plant’s resources seeking a broader focus rather than detail 11. The following information applies to Questions 11 through 13. Merriman Company provides the following ABC costing information: Activities Total Costs Activity-cost drivers Account inquiry hours $500,000 10,000 hours Account billing lines $250,000 5,000,000 lines Account verification accounts $100,000 50,000 accounts Correspondence letters $ 50,000 5,000 letters Total costs $900,000 The above activities are used by Departments A and B as follows: Department A Department B Account inquiry hours 1,000 hours 3,000 hours Account billing lines 200,000 lines 300,000 lines Account verification accounts 10,000 accounts 8,000 accounts Correspondence letters 1,000 letters 1,500 letters How much of the account inquiry cost will be assigned to Department A? $10,000 $50,000 $150,000 $500,000 ($500,000 / 10,000) x 1,000 = $50,000 12. How much of account verification costs will be assigned to Department A? $20,000 $50,000 $80,000 $100,000 ($100,000 / 50,000) x 10,000 = $20,000 13. How much of the account billing costs will be assigned to Department B? $15,000 $25,000 $30,000 $50,000 ($250,000/5,000,000) x 300,000 = $15,000 14. The following information applies to Questions 14 through 15. Zappo Skate Corporation manufactures two models of skate boards: a standard and a deluxe model. The following activity and cost information has been compiled. Product Number of Steups Number of Components Number of total Direct Labor Hours Standard 20 10 375 Deluxe 30 15 225 Overhead costs $25,000 $35,000 Assume a traditional costing system applies the $60,000 of overhead costs based on direct labor hours. What is the total amount of overhead costs assigned to the standard model? $20,000 $22,500 $25,000 $35,250 ($60,000 / (375 + 225)) x 375 = $37,500 15. Number of setups and number of components are identified as activity-cost drivers for overhead costs. Assuming an activity-based costing system is used, what is the total amount of overhead costs assigned to the standard model? $10,000 $14,500 $24,000 $30,000 [$25,000/ (20 + 30)] x 20 = $10,000 [$35,000/ 25] x 10 = $14,000 $24,000 16. If products are alike, then for costing purposes: a simple costing system will yield accurate cost numbers an activity-based costing system should be used multiple unit-level cost rates should be used varying demands will be placed on resources 17. With traditional costing systems, products manufactured in small batches and in small annual volumes may be _____________ because batch-related and product-sustaining costs are assigned using unit-related cost drivers. overcosted undercosted fairly costed ignored 18. Under traditional costing systems, selling and administrative costs have been largely ignored because they: are hard to quantify except at exorbitant cost of measurement have been negligible in amount relative to total costs now they are growing in amount in the past they are not inventoriable for financial reporting purposes under GAAP relate to a varied mix of products 19. The focus of ABC systems is on: long-term decisions short-term decisions make-or-buy decisions special-pricing decisions 20. It ONLY makes sense to implement an ABC system when: ABC provides information to make better decisions its benefits exceed implementation costs ABC traces more costs as direct costs there is a strong cause-and-effect relationship between costs in the cost pools and their cost-allocation bases