Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Marketing strategy wikipedia , lookup

Market penetration wikipedia , lookup

Dumping (pricing policy) wikipedia , lookup

Resource-based view wikipedia , lookup

Pricing strategies wikipedia , lookup

Product planning wikipedia , lookup

Perfect competition wikipedia , lookup

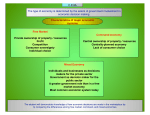

Chapter 1-Decisions and Systems Read the Focus on Real Life **Tell the difference between his wants and needs Needs & Wants Hardly a day goes by you don’t see a product or service you would like to have. You see these products on the Internet, at the mall or the grocery store Advertisements try to convince you that you need whatever is new Needs are Essential You want many things but do you really need them? Determining which is which and what is important is part of making good decisions Needs: things that are required in order to live o Basic needs are: 1. Food 2. Water 3. Clothing 4. Shelter o Other needs in today’s economy are: 1. Good education 2. Employment 3. Safety Wants Add to the Quality of Life Wants: things that add comfort and pleasure to your life You may believe you can’t live without the latest CD, latest fashion or the latest phone upgrade but you can Most of the time you can live in a small apartment but we would rather have the large house or a vacation home. Also it would be possible to use public transportation but driving a nice care with all the great options adds convenience and an image of success Needs and Wants are Unlimited Your needs and wants are never ending You are limited by your imagination and what businesses make available for sale One want will lead to another and then it just snowballs o A new video game player leads to wanting to a new set of games o A new pair of shoes may require new accessories Wants are not the same for every person Goods and Services You satisfy your needs and wants by purchasing and consuming good and services Goods: things that you can see and touch o They are the products you can purchase to meet your needs and wants Services: activities that are consumed at that same time they are produced Goods and Services for Businesses and Consumers Businesses and consumers both make purchases Some purchases are unique for business or consumer use Consumers buy furniture, televisions, smart phones and books They also eat at restaurants, go on vacation or take their car into get serviced Businesses supply the goods and services that meet the business and consumers needs and wants The U.S. Economy The United States is the largest producer of goods and services in the world. In 2013 we produced more than the next two largest producers, China & Japan combined!! Americans consume more than any other country We rank first in oil consumption In 2013 we consumed 19 million barrels per day, which was more than the combined consumption of China, Japan and India The move to an industrialized economy resulted in higher incomes and more choices of products and services for consumers Increased consumer spending results in more jobs and a higher standard of living Not all consumption is excessive and most of them purchase within their means Increased consumption also leads to challenges for a country such as; pollution, preserving natural resources and managing waste Economic Resources Most people don’t make the products and services they consume Economic resources: things available to be used to produce goods and services Economic resources are called factors of production There are three kinds of economic resources: 1. Natural resources 2. Capital resources 3. Human resources Both businesses and individuals use these resources to produce goods and services Natural Resources These are the resources supplied by nature Examples: o Oil o Minerals All products begin with one or more natural resource The supply of many natural resources are limited Increased consumption and destruction of the environment threatens many natural resources However, recycling and conservation practices as well as the design of more efficient products helps to preserve resources Human Resources These are the people who produce goods and services Examples: o Farmers raise livestock and crops o Factory workers and managers use equipment designed by engineers o Truck drivers, sales people, advertisers and employees are involved in production and availability of a product to consumers An entrepreneur is another example of a human resource. o Entrepreneurs are the risk takers who use resources in an entirely new way to create a new product o Without entrepreneurs there would be fewer choices of good and services. And also fewer employment opportunities Capital Resources The products and money used in the production of good and services are called capital resources Examples: o Building o Equipment o Supplies o Money Money is used to build the building, buy or lease vehicles, pay employees or buy other goods and services needed to complete their product People will invest money in businesses so that the business will have the capital needed to operate the business. These people expect they will make money from the profits the company makes. People also receive income from selling their knowledge and skills to a business in the form of labor Those special skills or knowledge of important business processes often command a higher income than those with more common skills or knowledge Resources are Limited All resources are limited in supply Most resources can be used to make several different products Usually the resources that are needed to make a specific product will not be available for something else Businesses and countries will compete for access to certain resources Those high demand resources or the ones that are limited with command a higher price With the limit of certain resources comes the limit of how much of the good or service that can be produced using that resource. That in turn will make the price for that product even higher **Do assessment 1-1 on page 11(questions 1-4) The Basic Economic Problem Basic Economic Problem: the mismatch of unlimited wants and needs and limited resources Examples of this problem: o Want to purchase a product but have limited money o Schools have to cut back on staff, classes or extracurricular activities because operating costs are increasing faster than annual budget o A business wants to expand but doesn’t have access to adequate land for a larger building o A country can’t provide health care to all it citizens because it doesn’t have enough doctors or hospitals The basic economic problem is because of scarcity Scarcity: not having enough resources to satisfy every need Scarcity affects everyone, but some people are affected more than others People who are on a limited or fixed income have choose very carefully the best way to spend their money to meet their needs and wants Countries with few natural resources or a poor education system may not be able to produce enough products and services for their citizens. Choices Individuals and families must decide how they want to spread their income to all the things they want and need City, State and National governments must cope with the problem of providing the services citizens demand using the tax dollars they collect In both of these cases someone has to make a difficult choice How do you decide which option is best? Usually you will choose the thing that you want most and can afford Example: o Say you earn $75/week at a part time job. If you spend the money you earned this week on a new pair of shoes you will not have enough money left to spend on eating out or going out with your friends on Saturday night. So you will have decide which want is greater, the shoes or a night out with friends. There is a logical process that you can follow to help you make these types of decisions Economic Decision-Making: the process of choosing which needs and wants will be satisfied Trade-Offs & Opportunity Costs Trade-off: when you give up something to have something else From the example earlier you would trade going out with friend for the new shoes The decisions making process will help you make the most satisfying choice Opportunity cost: the value of the next best alternative that you did not choose The benefit you get from your choice should be greater than the benefit from the next choice The Economic Decision Making Process There is a six steps to the decision making process Businesses and individuals will use this process for the best use of their limited resources o 6 steps 1. 2. 3. 4. 5. 6. Define the problem Identify the choices Evaluate the pros and cons Choose one Act on choice-do what you chose to do Review the decision Most of the time you will go through this process in your head, however bigger decisions may be put to paper **Do assessment on page 15 (questions 1-4) The Three Economic Questions All nations of the world face the basic economic problem Each country must decide how to use available resources All nations must answer three economic questions 1. What goods and services will be produced? 2. How will the goods and services be produced? 3. What needs and wants will be satisfied with the goods and services produced? How these questions are answered indicated the type of economic system that exists in each country Types of Economic Systems Economic System: the method a country uses to answer the three economic questions The type of system is based on how involved the government is in the marketplace There are several types of economic systems operating in the world today, each is based on one of these three main types Command Economy Command economy: the resources are owned and controlled by the government The government decides how and what goods are produced and how they will be distributed and consumed They decide how much and what resources will be used to produce the goods and services for consumers such as food, schools, vehicles and houses They also decide how resources will be used by businesses and government; including machines, equipment and factories Some command economies are so strict that they may assign people to specific schools or even career paths Personal economic freedom is limited in a command economy Market Economy Market economy: the resources are owned and controlled by the people of the country The three economics questions are answered by individuals through buying and selling of goods and services in the marketplace Marketplace: anywhere that goods and services exchange hands This includes the supermarket, Internet, a business office or even a flea market The government has limited involvement in a market economy Consumers and businesses make decisions based on their own self-interests Every time you buy something in the marketplace you placing a “vote” in dollars When businesses offer products and services consumers want they are rewarded with profits Traditional Economy Before complex economic systems developed, some operated according to tradition or customs Traditional Economy: things are produced the way they have always been done This type of economy in countries that are less developed and not currently participating in the global economy How to produce things is handed down generation to generation They will use the natural resources available to them and hand tools that they have made Mixed Economies Most of world economies can be classified as mixed economies, a combination of command and market economies Various degrees of government involvement exist in these marketplaces During the past decade several Eastern European nation have moved from a command economy to a mixed economy More than 1.3 billion Chinese citizen have a communist government, however the economy of China is adopting elements of a market economy for a number of economic decisions Many traditional economies will adopt the mixed economy The U.S. Economic System The U.S. operates on a market economy Another name for a market economy is Capitalism Capitalism: private ownership of resources by individuals rather than by the government The U.S. economy is based on 4 very important principles 1. Private property: you can use, own, or dispose of things of value 2. Freedom of Choice: you make choices freely but also accept their consequences 3. Profit: why business operate Profit: the money left from sales after all costs of operations have been paid Profit is the heart of private enterprise 4. Competition: this forces businesses to keep costs low, have effective customer service and search for new ideas **Do Assessment page 22 (questions 1-3) Participating in a Market Economy In a market economy buyers and sellers use the marketplace to make purchases Consumer: a person who buys and uses goods and services Consumers have a big impact on a market economy, because they decide what to buy, who to buy from and what price they are willing to pay Producers: individuals and organizations that determine what products and services will be available for sale Producers invest resources and take risks to make a profit Producers also determine what products and services will be available Consumers set Demand Demand: the quantity of a good or service that consumers are willing and able to buy Businesses can prosper or fail depending on how they react to consumer demand Example: o A new restaurant opens and the service is slow, the food is poor and the noise levels are high people will be unlikely to come back unless changes are made Producers establish Supply Supply: the quantity of a good or service that a business is willing and able to provide If consumers are seeking a popular product and willing to pay a high price for it businesses will provide the product to meet the need On the other hand with heavy competition for a product or people are getting tired of the product the price is going to go down, Determining Price Why is the price of a hotel in Arizona higher in the winter than in the summer? Why do the prices do the prices of many of the products sold by farmers remain low? Prices are affected by the relationship between supply and demand and other factors Factors influencing Demand When consumers want (demand) a particular product, its price will tend to go up People want to vacation in Phoenix during the winter so the demand for rooms goes and then the price for the rooms goes up In the hot summer months in Phoenix there isn’t as much demand for rooms so the price for the rooms will go down. Customers are willing to switch from one product to another if the price of one is much higher than the others However, if a good substitute can’t be found customers will be willing to pay a little more, even if the price is high Factors influencing Supply Supply can also affect the price Supply of certain items is always high so the price will remain low Competitors: businesses offering very similar products to the same customers With more competitors the supply will go up, so a business will not be able to raise it prices as easily. They will have to keep an eye on what their competitors are pricing their products at If you live a community where there is only one supermarket the prices at that store will often be higher due to lack of competition If a natural disaster interrupts the supply of a product it will send the price up as well. Determining Market Price Market price: the point where supply and demand are equal **Look at the example chart on page 26 **Do assessment page 26 (questions 1-4)