Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

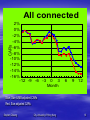

What price connection? Expropriation of minority shareholders in the HK stock market * by Stephen Yan-leung Cheung Department of Economics and Finance City University of Hong Kong *The paper is co-authored by Cheung, Ran and Stouraitis “...China Logistics Group (00217) to confess that millions of dollars has gone missing from its coffers.... The bulk of the cash is suspected to have vanished across the border.... A HK$ 200 million deposit paid out for the acquisition of Shanghai Pudong CNCC Logistics Development was missing... while the money left China logistics, it was allegedly never received by the vendor.” South China Morning Post, 18 September 2002. Stephen Cheung City University of Hong Kong 2 Introduction Companies with concentrated ownership: extract case by selling assets, goods, or services obtain loans on preferential terms assets transfer dilute the minority shareholders’ interests Stephen Cheung City University of Hong Kong 3 Introduction A connected transaction is a) any transaction between a listed issuer or any of its subsidiaries and a connected person, whether or not it also falls within any of the other categories in 14.02; and b) an acquisition or realisation by a listed issuer or any of its subsidiaries of an interest in a company, a substantial shareholder of the listed acquiring or realising issuer or any of its subsidiaries of the listed issuer or any of its subsidiaries Stephen Cheung City University of Hong Kong 4 Objectives 1) What are the valuation effects of different types of connected transactions? 2) What are the characteristics of firms more likely to expropriate? 3) Does the market anticipate the expropriation by firms? Stephen Cheung City University of Hong Kong 5 Types of connected transactions 1) Asset acquisition 2) Asset sales 3) Equity sales 4) Trading relationships 5) Cash payments 6) Cash receipts 7) Subsidiary relationships 8) Takeover & joint-ventures 9) J V stake acquisition 10) Jo V stake sales Stephen Cheung City University of Hong Kong 6 Observations 1) 2 times more assets acquisition than asset sales; cash from listed companies to its controlling owners 2) 3.5 times more in providing cash assistance to third parties as opposed to receiving assistance 3) Terms are unfavorable (acquiring at a premium or selling at a discount) for most deals when information are available Stephen Cheung City University of Hong Kong 7 Results Short-term, Average of -3.4% during a period of 10 days after announcement Sales of equity stake Sales of assets Acquiring of assets Trading relationships Selling JV Cash payment Stephen Cheung City University of Hong Kong -11.8% -6.4% -7.5% -7.5% -6.1% -2.5% 8 Long term, Average of -12.6% during a period of 12 months after announcements Sales of assets -21.9% Trading relationships -21.8% Cash payment -18.7% Takeover & JV -29.8% Selling JV -17.2% Stephen Cheung City University of Hong Kong 9 All connected CARs 2% 0% -2% -4% -6% -8% -10% -12% -14% -16% -12 -9 -6 -3 0 3 Month 6 9 12 Blue: Size & MB adjusted CARs Red: Size adjusted CARs Stephen Cheung City University of Hong Kong 10 Returns are negatively related to percentage ownerships by the main shareholders negatively related to proxies for information disclosure * value of transaction * independent financial advisor * Big 5 as auditing firm Stephen Cheung City University of Hong Kong 11 likelihood of undertaking connected transactions is higher * ultimate owners can be traced to mainland China likelihood of not disclosing the value of the deal and likelihood of violating the listing rules are higher for * Mainland China ownership * Concentrated ownership Stephen Cheung City University of Hong Kong 12 Variable of Corporate governance do not have any impact * audit committee * number of independent non-executive directors * CEO duality Stephen Cheung City University of Hong Kong 13 Discussion The quality of independent non-executive directors Information disclosure Regulatory framework Stephen Cheung City University of Hong Kong 14 ~END~ Stephen Cheung City University of Hong Kong 15