Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

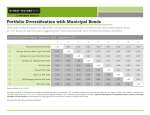

Municipal bonds: Three reasons to invest 1. Income Municipal bonds continue to represent an attractive source of income, despite much-talked-about tax reform and its potential implications. Our view: Lower individual tax rates and/or a potential cap on tax-exemption may lower the value of munis’ tax benefit, but neither change erases it. As shown below, munis still offer an after-tax yield advantage relative to other fixed income assets − even at a lower tax rate. Peter Hayes, Head of the BlackRock Municipal Bonds Group Attractive after-tax income, even at lower tax rates Yields across fixed income assets 5.0% Municipal bonds hit a postelection speed bump, but are regaining traction as investors acknowledge some of the features that continue to make tax-exempts attractive. Peter Hayes, Head of the BlackRock Municipal Bonds Group, points to three timely and perhaps not-so-obvious reasons to consider the asset class today. 4.56 4.0 3.39 3.0 2.58 2.68 Munis Aggregate 3.58 1.98 2.0 1.0 0.0 Treasuries Invest.-grade Muni TEY @ 28% Muni TEY @ 43.4% Sources: BlackRock and Bloomberg; as of March 21, 2017. Yields shown are yield to worst. Treasuries represented by the Bloomberg Barclays Treasury Index, munis by the Bloomberg Barclays Municipal Bond Index, aggregate by the Bloomberg Barclays U.S. Aggregate Bond Index and investment-grade by the Bloomberg Barclays U.S. Aggregate Corporate Index. It is not possible to invest directly in an index. TEY (tax equivalent yield) figures show the tax-adjusted yield offered at current top tax rate of 43.4% and assuming a 28% cap on the benefit of tax-exemption. Positioning your muni allocation While munis may come with more uncertainty and volatility than in recent years prior, that does not make them any less valuable as a core component of a broadly diversified portfolio, in our view. Munis provide the unique advantage of tax-free income (alterable, but not dispensable), high credit quality among fixed income options, and an important ballast to equity and equity-like risk. We’d offer four key ideas for managing your municipal bond allocation in 2017: Favor short to intermediate maturities (7-10 years) for liquidity, flexibility and insulation from interest rate and policy uncertainty. Consider flexible strategies that allow you to be nimble and manage around interest rate and policy risks. Look to the A-rated space, which has outperformed the broader market since 2009. Be choosy and diversify. Not all credits are created equal. We see an advantage in owning a diversified, professionally managed portfolio of munis over single bonds. blackrock.com 20170510-154097-421027 2. Quality and diversification 3. Value With an average rating of AA, the municipal market remains of high quality, particularly relative to the corporate bond market. In addition, municipals have tended to have very low default rates, a dynamic that is unlikely to change. The reason: Municipalities, unlike corporations, have a social and political obligation to continually provide services to tax-paying citizens, making defaults difficult and rare. S&P’s most recent data puts 10-year cumulative default rates at 0.15% for investmentgrade municipals vs. 2.72% for investment-grade corporate bonds. Municipal bonds also have tended to exhibit low volatility. We expect that to tick up this year as the market anticipates Fed rate moves and clarity around tax reform, but it is unlikely to rise to the level of traditional risk assets. In fact, munis show a negative correlation to equities, making them effective portfolio diversifiers. Muni prices fell sharply immediately post-election. The drop reflected interest rate and liquidity concerns, as well as policy uncertainty under a new administration. The policy fears centered on tax reform diluting the benefit of the tax-exemption (and hurting demand) and infrastructure spending inciting a spike in supply. The market has since come to realize that the actual manifestation of these early policy promises isn’t so clear cut. Munis can help offset equity risk One-year correlation to various assets Is the market overpricing tax reform? 1.00 0.80 0.63 0.60 Muni pricing puts tax rate at 25% 0.58 0.40 0.09 0.20 Equities 0.00 -0.20 Treasuries Tax reform could take many forms, extending pros and cons across asset classes, and infrastructure spending could prove a positive depending on how it’s funded. By some measures, the market is priced for tax rates in the area of 25%. This would be an overshoot if you assume a top marginal tax rate at 33% and the benefit of the muni tax deduction capped at 28%. Ultimately, the market has not adjusted back to its pre-election level, and the “price gap” between Election Day and today is where the opportunity may reside. Invest.-grade High yield -0.40 -0.19 Source: Morningstar, as of Feb. 28, 2017. Correlations based on one-year daily total return. Treasuries represented by the Bloomberg Barclays Treasury Index, investmentgrade by the Bloomberg Barclays Investment Grade Corporate Index, high yield by the Bloomberg Barclays U.S. High Yield 2% Issuer-Capped Index, equities by the S&P 500 Index, and munis by the Bloomberg Barclays Municipal Index. Want to know more? 50% 45 40 35 30 25 20 15 Implied tax rate 3/15/16 6/15/16 9/15/16 12/15/16 3/15/17 Sources: BlackRock and Bloomberg Barclays indexes, as of March 15, 2017. Chart shows the market-implied tax benefit by calculating the complement of the ratio of the Bloomberg Barclays Municipal Bond Index to the Bloomberg Barclays U.S. Aggregate Corporate Index. blackrock.com/keepmore Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results. This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of March 2017, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader. ©2017 BlackRock, Inc. All Rights Reserved. BLACKROCK is a registered trademark of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners. Prepared by BlackRock Investments, LLC, member FINRA. Not FDIC Insured • May Lose Value • No Bank Guarantee Lit. No. 3REASONS-0317R 008512A-0317 20170510-154097-421027