Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

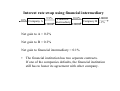

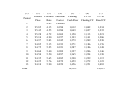

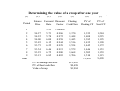

Interest rate swap using financial intermediary 10.0% LIBOR Financial 10% Company A Company B +1% intermediary LIBOR LIBOR 9.9% Net gain to A = 0.2% Net gain to B = 0.2% Net gain to financial intermediary = 0.1% • The financial institution has two separate contracts. If one of the companies defaults, the financial institution still has to honor its agreement with other company. 1 Exploiting comparative advantages • Initial motivation for the interest rate swap market was borrower exploitation of “credit arbitrage” opportunities because of differences between the quality spread between lower- and higher-rated credits in the US and Eurodollar bond markets. Query As with any arbitrage opportunity, the more it is exploited, the smaller it becomes. Explanation The difference in quality spread persists due to differences in regulations and tax treatment in different countries. 2 Valuation of interest rate swap • When a swap is entered into, it typically has zero value. • Valuation involves finding the fixed coupon rate K such that fixed and floating legs have equal value at inception. • Consider a swap with payment dates t1, t2, …, tN set in the terms of the swap. (ti – ti-1) ×K × N … 0 t1 t2 … ti tN 3 Valuation (cont’d) • Fixed payment at ti is (ti – ti-1) × K × N where N is the notional principal, ti – ti-1 is the tenor period. The fixed payments are packages of bonds with par K × N. • To generate the floating rate payments, we invest a floating rate bond of par value $N and use the floating rate interest earned to honor the floating leg payments. At maturity, $N remains but all the intermediate floating rate interests are forgone. “Assume forward rates will be realized” rule 1. Calculate the swap’s net cash flows on the assumption that LIBOR rates in the future equal today’s forward LIBOR rates. 2. Set the value of the swap equal to the present value of the net cash flows using today’s LIBOR zero curve for discounting. 4 Valuation (cont’d) • Let B(0, t) be the discount bond price with maturity t. • Sum of percent value of floating leg payments = N[1 – B(0, tN)]; sum of present value of fixed leg payments = N ( N × K )∑ (ti − ti −1 ) B(0, ti ). i =1 • Hence, the swap rate is given by K= 1 − B(0, t N ) N ∑ (t − t i =1 i i −1 . ) B(0, ti ) 5 Swap rate curves • From traded discount bonds, we may construct the implied forward rates; then the equilibrium swap rates are determined from these forward rates. • Turning around, with the high liquidity of the swap market, and available at so many maturities, it is the swap rates that drive the prices of bonds. That is, the fixed leg of a par swap (having zero value) is determined by the market. • For swap-based interest rate derivatives, swap rates constitute the more natural set of state variables, rather than the forward rates. 6 Numerical Example: Determining the Swap Rate Three-year swap, notional amount $100 thousand Fixed-rate receiver Actual/360 day count basis, quarterly payments Floating-rate receiver 3-month LIBOR, actual/360 day count basis, quarterly payments and reset. Swap rate is the rate that will produce fixed cash flows whose present value will equal the present value of the floating cash flows. 7 (1) Period 1 2 3 4 5 6 7 8 9 10 11 12 13 Total (2) (3) (4) (5) Futures Forward Discount Floating Price Rate Factor Cash Flow 4.05 1.00000 95.85 4.15 0.990 1,012 95.45 4.55 0.980 1,049 95.28 4.72 0.969 1,150 95.10 4.90 0.957 1,193 94.97 5.03 0.945 1,279 94.85 5.15 0.933 1,271 94.75 5.25 0.921 1,287 94.60 5.40 0.909 1,327 94.50 5.50 0.897 1,365 94.35 5.65 0.885 1,390 94.25 5.76 0.872 1,459 94.10 5.90 0.859 1,456 14,053 (6) (7) PV of PV of Floating CF Fixed CF 1,002 1,027 1,113 1,141 1,209 1,186 1,186 1,206 1,224 1,229 1,272 1,251 1,234 1,235 1,221 1,206 1,230 1,176 1,148 1,146 1,130 1,115 1,123 1,083 14,053 8 Column (2): The Eurodollar CD futures price. Column (3): Forward Rate = Futures Rate. The forward rate for LIBOR found from the futures price of the Eurodollar CD futures contract as follows: 100.00 – Futures price Column (4): The discount factor is found as follows: Discount factor in the previous period [1 + (forward rate in previous period × number of days in period/360)] 9 Column (5): The floating cash flow is found by multiplying the forward rate and the notional amount, adjusted for the number of days in the payment period. That is: Forward rate previous period × number of days in period × notional amount 360 Column (7): This column is found by trial and error, based on a guess of the swap rate. In determining the fixed cash flow, the cash flow must be adjusted for the day count as follows: Assumed swap rate × number of days in period × notional amount 360 10 Determining the value of a swap after one year (1) Period 1 2 3 4 5 6 7 8 9 Total (2) (3) (4) (5) Futures Forward Discount Floating Price Rate Factor Cash Flow 94.27 94.22 94.00 93.85 93.75 93.54 93.25 93.15 5.25 5.73 5.78 6.00 6.15 6.25 6.46 6.75 6.85 1.00000 0.986 0.972 0.958 0.944 0.929 0.915 0.900 0.885 PV of floating cash flow PV of fixed cash flow Value of swap 1,370 1,448 1,445 1,516 1,554 1,579 1,668 1,706 (6) (7) PV of PV of Floating CF Fixed CF 1,352 1,408 1,385 1,432 1,445 1,446 1,502 1,510 11,482 1,284 1,225 1,195 1,190 1,172 1,153 1,159 1,115 9,498 $11,482 $9,498 $1,984 11 Credit exposure on derivatives Credit risk fluctuates over time with the variables that determine the value of the underlying contract. Current exposure Replacement cost if the counterparty defaults right now. Potential exposure Estimation of the future replacement cost: expected exposure and maximum exposure. At best, we provide probabilistic assessment. 12