Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

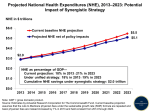

Health Care Chapter 7 Is Health Care a Special Good? 1. Considered fundamental right by many 2. Most health expenditure is covered by third-party payments 3. Lack of competition in the health care sector Health Care as Fundamental Right • Fairness considerations: health care is a right • Economics: Who is going to pay for the “fundamental right” provision? What if a patient can’t afford health care services? Third-Party Payments Definition. A payment made directly to the provider of a good or service by a party other than the buyer is called a third-party payment. If a patient is insured, third-party payments cover most of the health care costs. Growth in third-party payments since 1960s, up to 88% Ambiguous effects of increased insurance coverage. Lack of Competition • Effects of competition in private markets Innovation Reduce production costs Provide better quality • Lack of competition in health care Physician-induced demand Government regulation Physician-Induced Demand Definition. Ineffective health care prescribed by physicians to increase their own wealth is called physician-induced demand. Asymmetric information: the patients are less informed about medicine compared to the doctors. Doctors have incentives to prescribe unnecessary or ineffective care. Government Regulations • 1945: federal McCarran-Ferguson Act prohibiting interstate competition among health insurance firms • Lack of competition results in Higher prices Lower quality Problems with the Health Care Sector 1. Rising share of GDP devoted to health care 2. More uninsured 3. Wasteful spending National Health Expenditure Definition. National health care expenditures adjusted for inflation and population growth are called real National Health Expenditures (NHE) Definition. Gross domestic product adjusted for inflation and population is called real GDP per capita. • Real NHE to grow faster than real GDP per capita • The share of NHE in GDP has been increasing: see graph NHE Expenditures, GDP Share Affordability of Health Care Expenditures • Growing health care share in GDP is impossible to maintain in the long-run • In the short- to medium-run, growing share of NHE in GDP is affordable if expenditure on all other goods does not decline Health care expenditures Non-health care expenditures Future Scenarios • Scenario 1: real NHE per capita grows 1% point faster than real GDP per capitanon-health expenditure grows • Scenario 2: real NHE per capita grows 2% points faster than real GDP per capitanon-health expenditure declines • Historically, the gap has been closer to 2% rather than 1%: see the graph Future Scenarios Projected non-health care expenditures per capita Medicare and Medicaid • Medicare: a federal health insurance program for people 65 and over • Medicaid: a federal and state program that provides health care for low-income and disabled persons. • Medicare and Medicaid expenditures take up increasingly larger share of the government budget: see graph Medicaid, Medicare and Budget Medicare, Medicaid as % projected budget revenues Growing Share of Medical Insurance: Problems • Financing increases in Medicare and Medicaid Increase budget deficit Reduced GDP growth rate Increased inflation rate Increase taxes A tax increase of 35-45% Transfer resources from discretionary government programs Impossible to cover all the increased costs Health Care and Households’ Budget • How households pay for health care Direct payments for expenditures not covered by insurance Health insurance premiums Reductions in take-home pay due to employer-provided health insurance Taxes to finance Medicare, Medicaid, other health programs Growing Ranks of the Uninsured • 15% population uninsured • Share of the uninsured rising • Many insured face risk of losing insurance, e.g. by losing a job Growing Share of Uninsured Health Insurance and Large vs Small Firms • For large firms, cost of health insurance per employee is much smaller than it is for the small firms Administrative costs per employee are much higher for small firms Risk of loss is higher in a small pool of employees NHE and the Uninsured • NHE share in GDP grows • Share of uninsured grows as well • Causality? Just correlation? We don’t know • Employers might drop health insurance plans as fringe benefits to reduce costs associated with health insurance Wasteful Spending • With insurance, more demand is in place than is socially optimal • Technically, some demand for health care occurs when the marginal costs exceed marginal benefits: see graph Health Insurance and Inefficiency • Without insurance, market clears at P1, efficient • With insurance Price Ps is paid by consumers Price P2 is received by producers Consumer expenditure: H2xPs Third party expenditure: (P2-Ps)xH2 Total spending increases by A+B+C+D+E Total costs increase: C+D+E Total benefits increase: D+E Welfare cost: C How Much is the Loss? • Wasteful spending can be measured as A+B+C+D+E: total additional spending C: welfare cost Definition. Spending that provides benefits that are less than costs is called wasteful spending. Price Indices for Health Care and Consumer Goods • Health insurance creates higher prices, which we see comparing price indices for medical care and nonmedical goods • Is this trend going to continue forever? • No insurance may actually be preferable (laser eye surgery prices dropped since 1998, not covered by insurance) Laser Surgery Case • 1998: $2200 per eye • 2004: $1350 per eye • Number of eye surgeries has been growing, too • Laser eye surgery is a sector without health insurance! Economic Inefficiency: General View • Benefits are less than costs • (Allocative inefficiency): benefits per dollar of cost are different across sectors Health Insurance: Inefficiency Reasons 1. Third-party payments 2. Physician-induced demand 3. Defensive medicine 4. Federal tax subsidy of employer-provided health insurance Defensive Medicine Definition. Medical procedures or diagnostic tests performed to reduce the risk of a lawsuit are called defensive medicine. To avoid damage from malpractice lawsuits, doctors buy malpractice insurance. The cost of malpractice insurance has been increasing. To avoid malpractice insurance costs, doctors practice defensive medicine. Third-party payments make the problem worse since doctors are more willing to prescribe useless medicine in case they know patients do not face all the costs. Data on Defensive Medicine • 90% physicians practice defensive medicine • 92.5% surgeons ordered imaging tests to protect themselves from lawsuits • 34% of overall health care costs attributed (by doctors) to defensive medicine • 42% doctors avoid dealing with patients with complex conditions or patients perceived to be litigious Defensive Medicine: Positive Effects • Higher quality care • Reduction in number of high-risk procedures Federal Tax Exemption • Employers pay for up to 80% of health insurance premiums • These costs are shifted to the employees as lower wages • Employees’ compensation is exempted from the federal individual income tax if it is received in the form of health insurance • Estimate: tax exemption for health insurance increases demand for health care by 10% to 20% among under-age-65 Controlling Health Care Expenditures • Current growth rates are unsustainable • Need to control health care expenditures 1. Managed care (more command-and-control) 2. Introducing competition (more market-oriented) Managed Care Definition. Health care that is reviewed by someone other than the patient or provider to determine whether the right services are being provided and whether the cost of provision is minimized. • A price-control scheme with the rates received by doctors negotiated in return for the insurance provider providing patients • Effects of price controls Rationing: not all patients get equal access to health care services Doctors are chosen by the insurance providers, not by the patients More patients get medical care, but: Longer waiting time Age-based discrimination Introducing Competition • More competition seems to be the key to reducing health care costs 1. Health savings accounts 2. Health care vouchers 3. Interstate competition for health insurance Health Savings Accounts • Health insurance induces unnecessary demand, e.g. visit to an expensive emergency room instead of waiting until morning • Health savings accounts Tax-deductible Larger co-paymentsless moral hazard Used for light diseases, for instance Serious illnesses covered by insurance taken out by the employer, which is much cheaper than an all-inclusive insurance Remaining balance on a health savings accounts carries over to the next year Since unnecessary demand is reduced, prices are down, and doctors compete to attract patients by increasing quality of their services Health Care Vouchers Definition. A coupon that can be used to pay for something, such as health care or health insurance is called a health care voucher. Target: poor people who don’t get health insurance through an employer Form: e.g. a government “credit card” with limited balance Competition: a patient can choose his doctor Interstate Competition • Competition is benefited due to the increase in the number of health care providers Eliminating Federal Tax Exemption • Problems with the tax exemption • Excessive health care spending • Unnecessary as a means of increasing availability of low-cost insurance • Value rises with marginal tax ratesubsidy to high income earners • Equivalent to direct expenditures worth $100 billion (2004) • Elimination of the tax exemption is politically challenging