Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

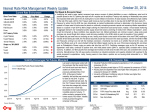

GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND SEPTEMBER 30, 2014 ROBIN GREENWOOD GEORGE GUND PROFESSOR OF FINANCE & BANKING, HARVARD BUSINESS SCHOOL SAMUEL G. HANSON ASSISTANT PROFESSOR, HARVARD BUSINESS SCHOOL JOSHUA S. RUDOLPH MASTER IN PUBLIC POLICY, HARVARD KENNEDY SCHOOL OF GOVERNMENT LAWRENCE H. SUMMERS CHARLES W. ELIOT UNIVERSITY PROFESSOR, HARVARD UNIVERSITY OUR PAPER I. Quantify Fed vs. Treasury conflict in QE era II. Fed vs. Treasury in historical perspective III. A modern framework for debt management IV. Ways to resolve Fed vs. Treasury conflict PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 20% 15% 10% The Fed’s Quantitative Easing (QE) policies have reduced the net supply of long-term securities. 5% 0% Fed QE: Treasuries, Agencies and MBS -5% -10% -15% -20% 2007 QE1 2008 QE2 2009 2010 Twist 2011 QE3 2012 2013 15.6% PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 20% 15% 10% Meanwhile the Treasury was doing the opposite, extending the average maturity of its borrowings. Treasury: Maturity Extension 5% 5.6% 0% Fed QE: Treasuries, Agencies and MBS -5% -10% -15% -20% 2007 QE1 2008 QE2 2009 2010 Twist 2011 QE3 2012 2013 PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 20% 15% Treasury: Maturity Extension 10% 5% 0% Fed QE: Treasuries, Agencies and MBS -5% -10% -15% -20% 2007 QE1 2008 QE2 2009 2010 Twist 2011 QE3 2012 2013 Net Impact: 10.1% PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 30% 24.9% 10-year equivalents, % of GDP 20% Treasury: Rising Debt Stock 10% 5.5% Maturity Extension 0% Fed QE -10% 15.6% -20% 2008 2009 2010 2011 2012 2013 2014 MARKET IMPACT Relying on prior studies, we estimate that the Fed’s QE policies have lowered the yield on 10-year Treasuries by a cumulative 1.37 percentage points. Thus, Treasury’s maturity extension may have offset as much as one-third of QE’s market impact. FED VS. TREASURY HISTORICALLY Before 2008, the Fed’s balance sheet was far smaller. As a result, the Fed had little impact on the maturity structure of the government’s consolidated debts. 100% Treasury % of GDP 75% 50% > 5y 1-5y 25% < 1y 0% 1943 > 5y 1950 1957 1964 1971 1978 1985 1992 1999 2006 1-5y 2013 Fed -25% 1936 < 1y TRADITIONAL DEBT MANAGEMENT Treasury’s traditional approach to determining the appropriate maturity of the debt traded off a desire to achieve low cost financing against the desire to limit fiscal risk. Low cost financing Shorter-term Limit fiscal risk Longer-term TRADITIONAL DEBT MANAGEMENT Issuing short-term is “cheaper” because it allows Treasury to capture the “liquidity premium” on Tbills and to conserve on the “term premium” investors demand to hold long bonds. Liquidity premium on short-term T-bills, Basis points 200 bps 150 100 50 0 2002 2004 2006 2008 2010 2012 2014 Term Premium on 10-Year Zero-Coupon Treasuries (1990 to 2014) -1 .0 QE3 Twist QE2 QE1 3.0 199 0 199 1 199 2 199 3 199 4 199 5 199 6 199 7 199 8 199 9 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 % TRADITIONAL DEBT MANAGEMENT 2.0 1.0 0.0 TRADITIONAL DEBT MANAGEMENT What is fiscal risk? • Refinancing risk • If the government issues short-term, it is exposed to increases in interest rates • If the government issues long-term, it ‘locks in’ the cost of capital • Rollover risk • Failed auction • Self-fulfilling bank run TRADITIONAL DEBT MANAGEMENT The desire to limit fiscal risk looms larger when the overall debt burden rises. Low cost financing Limit fiscal risk Shorter-term Longer-term TRADITIONAL DEBT MANAGEMENT Thus, Treasury has historically tended to extend the average maturity of the debt when debt-toGDP rises. Much like the Treasury is doing today. 120% 100% 80% 60% 40% 20% 0% 1936 1943 1950 1957 1964 1971 Long-term share Treasury 1978 1985 1992 Debt/GDP 1999 2006 2013 QUANTIFYING FISCAL RISK: A COUNTERFACTUAL We argue that the “fiscal risk” generated by issuing short-term debt is less important than traditionally thought.Deficits in Counterfactual Case in which Treasury rolled over 3-mo Bills Actual Path of Deficits TRADITIONAL DEBT MANAGEMENT Low cost financing Shorter-term Limit fiscal risk Longer-term MODERN DEBT MANAGEMENT Modern debt management recognizes that the maturity of government debt may also be a valuable tool for managing aggregate demand and promoting financial stability. Limit fiscal risk Financial stability Aggregate demand Low cost Shorter-term Longer-term DEBT MANAGEMENT CONFLICTS Objectives of modern debt management have been assigned to Treasury and Fed, which exercise different policy weights Limit fiscal risk Treasur Fed Financial y stability FedAggregate demand Treasur Low cost y Shorter-term Longer-term DEBT MANAGEMENT CONFLICTS • Expansionary monetary policy at ZLB • Extend average duration to mitigate fiscal risk (Treasury) • Shorten average duration to bolster aggregate demand (Fed) • Fed and Treasury in direct conflict over objectives • Contractionary monetary policy • Rise in premium on money-like assets • Increases incentive to issue short • In this case, Treasury-led debt management is expansionary SOLVING THE CONFLICTS • Outside of the zero-lower-bound, Fed sterilization of Treasury debt management is imperfect workaround • Fed gets last word using short rate • But sterilization no longer possible at the ZLB • Better solution: Treasury and Fed release annual joint statement on combined public debt management strategy • Forces each agency to internalize other’s objectives • Fed charged with routine tactical adjustments because of its expertise in open-market operations