Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

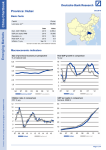

Talking point CIS: A resource-rich region experiencing the longest period of economic expansion since 1991 November 19, 2007 It is common knowledge that Russia possesses an abundance of natural resources such as oil and gas. In the context of rising commodity prices, however, other countries of the Commonwealth of Independent States* (CIS) have also moved into the spotlight. The CIS, which is home to about 280 million people, is blessed with having some of the largest deposits of oil, gas, coal and uranium in the world. Notably, high commodity prices have not only fuelled revenues in the energy-exporting countries like Azerbaijan, Kazakhstan, Russia, Turkmenistan and Uzbekistan but also in Armenia, Georgia, Tajikistan and Ukraine, which export cotton, copper and other metals, for instance. The revenues from commodity exports have meanwhile also spilled over into other parts of the economy and thus contributed to the longest period of economic expansion in the region since the countries became independent in 1991. As a consequence, foreign investors and policy makers have started to take a markedly increased interest in the CIS. The IMF recently highlighted that, apart from high commodity prices, an increase in foreign private capital inflows and productivity gains have boosted economic growth. Rising real income levels as well as better access to credit have also led to a rise in consumption which in turn has become the main driver of economic growth. Of course, rising commodity prices and terms-of-trade gains also pose challenges for the CIS, for instance with regard to the diversification of their economies. In our view, the near-term outlook for the region is quite favourable. Commodity prices are likely to remain high in the near future and new oil and gas fields may become operational and boost output in some countries. Russia obviously plays a key role in the region and affects the other countries’ growth via its import demand and flows of private remittances. Apart from Russia, strong demand from Kazakhstan and further regional economic integration could prove beneficial to smaller countries. In addition, financial sector deepening in the region as envisaged for instance by the Regional Financial Centre initiative in Almaty could also underpin further growth, especially since the gains may be especially large for less developed financial systems. Finally, there is still some potential for further economic growth due to catch-up opportunities as the CIS still exhibits relatively low GDP per capita. Important challenges remain though with regard to diversification of the economy and governance structures. Structural reforms and institutional developments have been improving but are still at a comparatively low level in many countries. Certainly, the wealth created via the commodity price boom could help to further speed up the transition process. Our CIS chartbook allows a visual comparison of economic and social developments in the CIS. See CIS chartbook * The Commonwealth of Independent States is a loose confederation consisting of Armenia, Azerbaijan, Belarus, Georgia, Kazakhstan, Kyrgyzstan, Moldova, Russia, Tajikistan, Ukraine, Uzbekistan and Turkmenistan as an associate member. The CIS has little scope in supranational decisions but it is more than a geographical term, possessing coordinating powers in trade and finance as well as lawmaking and security for these twelve of the fifteen former republics of the Soviet Union. Page 1 of 2 Talking Point Thorsten Nestmann (+49) 69 9103-1894 ...more information on Emerging Markets Talking Point - Archive © Copyright 2007. Deutsche Bank AG, DB Research, D-60262 Frankfurt am Main, Germany. All rights reserved. When quoting please cite “Deutsche Bank Research”. The above information does not constitute the provision of investment, legal or tax advice. Any views expressed reflect the current views of the author, which do not necessarily correspond to the opinions of Deutsche Bank AG or its affiliates. Opinions expressed may change without notice. Opinions expressed may differ from views set out in other documents, including research, published by Deutsche Bank. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. No warranty or representation is made as to the correctness, completeness and accuracy of the information given or the assessments made. In Germany this information is approved and/or communicated by Deutsche Bank AG Frankfurt, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht. In the United Kingdom this information is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange regulated by the Financial Services Authority for the conduct of investment business in the UK. This information is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. and in Singapore by Deutsche Bank AG, Singapore Branch. In Japan this information is approved and/or distributed by Deutsche Securities Limited, Tokyo Branch. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. Page 2 of 2